Follow us

Follow us

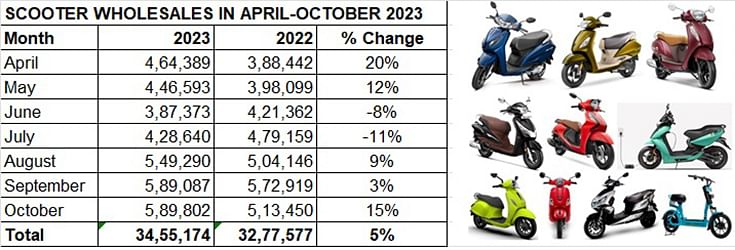

Scooter sales hit 589,802 units in October, best in first 7 months of FY2024

Demand is back in the scooter market and the festive season acts as a catalyst. While the ACtiva-powered Honda remains the unassailable market leader, TVS, Suzuki, Yamaha, Ather and Bajaj Auto increase their share in April-October 2023.

12 Nov 2023

12 Nov 2023

10244 Views

Share -

10244 Views

Share -

The festive season and Diwali are a bright light on the Indian automobile industry. So much so, that all segments have recorded strong year-on-year growth. As per the wholesales numbers released by SIAM for the passenger vehicle, two- and three-wheeler segments, cumulative sales at 2.36 million units are a strong 20% YoY growth (October 2022: 19,68,938 units). Importantly, all three segments have registered strong double-digit growth. And demand is finally back in the two-wheeler segment which comprises scooters, motorcycles and mopeds.

The two-wheeler segment registered total wholesales of 1.89 million units, up 20% YoY (October 2022: 15,78,383 units) and 8.34% on September 2023’s 17,49,794 units. Motorcycles, with 1.25 million units, were up 23% YoY and saw 12% MoM growth, and accounted for 66% of total segment sales.

In tandem with the motorcycle market, demand has also come the way of the scooter segment, which has a 47% share of the overall two-wheeler market. At 589,802 units, October 2023 numbers were up 15% (October 2022: 513,450 units) and are the best monthly numbers in the fiscal year to date (see data table below).

Scooter market leader Honda, with its Activa brand, continues to maintain its unassailable position with 251,241 units, up 4.85% YoY (October 2022: 2,39,598) and a market share of 42.64%. However, this also indicates that HMSI’s share has declined from 46.66% in October 2022.

TVS Motor Co, which continues to witness sustained demand for its Jupiter and NTorq 125 scooters, dispatched 153,831 units last month – this constitutes 22% growth over October 2022’s 125,896 units gives the company a scooter market share of 26%, up from the 24% it had a year ago. What is helping TVS is the growing contribution of its e-scooter, the iQube. At 20,121 units, the iQube accounted for 13% of TVS’ sales last month, up from the 6% it had a year ago (October 2022: 8,103 iQubes / 125,896 scooters).

Interestingly, Bajaj Auto dispatched all of 12,137 Chetaks, its best monthly performance yet since the company began selling the electric scooter in January 2020, the same month when the TVS iQube rolled out.

TVS, Suzuki, Yamaha, Ather and Bajaj increase scooter market share in April-October 2023

Cumulative scooter wholesales of 34,55,174 units in the first 7 months of FY2024 are 66.57% of FY2023’s 51,90,018 units and 84% of FY2021’s 41,12,672 units, which indicates growth is back in this segment.

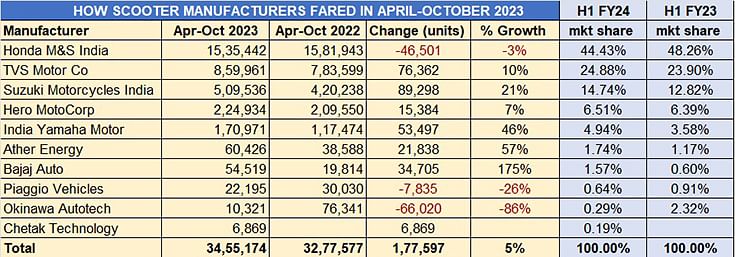

The top five OEMs among the SIAM 10 scooter members account for 33,00,844 units or an overwhelming 95% of total scooter sales April-October 2023. Of them, the top three players – Honda Motorcycle & Scooter India, TVS Motor Co and Suzuki – cumulatively have 29,04,939 units or 84% of the industry numbers. In terms of volume increase amongst these 10 OEMs, five OEMs –TVS, Suzuki, Yamaha, Ather and Bajaj Auto – stand out.

Honda Motorcycle & Scooter India (HMSI) with its Activa brand remains unassailable – the company dispatched 1.53 million units (15,35,442 units), 46,501 units fewer than a year ago and down 3% YoY. This sees HMSI’s scooter market share reduce to 44.43%, from the 48.26% it had a year ago.

TVS Motor Co remains the well-entrenched No. 2 player – at 859,961 units, sales are up 10% up YoY, which helps increase its market share marginally to 24.88% from 23.90% a year ago. While the Jupiter continues to be its best-seller, followed by the NTorq 125, the iQube electric scooter has contributed 116,192 units – this is a massive 257% YoY increase on year-ago 32,472 units and accounts for 13.51% to TVS’ total scooter sales.

Suzuki Motorcycle India has sold over half-a-million scooters – 509,536 units. In volume terms, it is 89,298 units more than a year ago and up 22%. This sees Suzuki’s market share rise smartly to 14.74% from 12.82% a year ago.

In fourth position is Hero MotoCorp with 224,934 units, up 7% and a market share of 6.51%. India Yamaha Motor with 170,971 units, sees sales grow 46% YoY, a strong performance that enables its scooter share rise to nearly 5%, up from 3.58% a year ago.

Two electric vehicle OEMs – Ather Energy and Bajaj Auto – have witnessed strong sales in April-October 2023. While Ather has sold 40,426 e-scooters in the form of the 450S and 450X, 21,838 units more than it did a year ago to achieve a market share to 1.74%, Bajaj Auto has dispatched 54,519 Chetaks, 34,705 more than in April-October 2022 for a market share of 1.57%, up on the 0.60% it had 12 months ago.

The electric two-wheeler market leader though is Ola Electric which clocked its highest monthly sales in October (22,565 units) and has increased its already-commanding share to 31 percent in April-October 2023. However, with the company not being a member of SIAM, Ola is not represented in this wholesales analysis of scooter manufacturers, which is specific to SIAM members only.

WILL DEMAND GROW FASTER?

In FY2023, 5.19 million scooters were sold, up 26% on FY2022’s 41,12,672 units. However, this was well below the pre-Covid FY2020 total of 5.5 million units (55,66,036 units) and way below the record 6.71 million units (67,19,811 units) of FY2018 and 6.70 million units of FY2019.

While there is no doubt that the domestic market scenario is much improved since a year ago, the scooter market in tandem with motorcycles is yet to see fulsome demand come its way. The cost of two-wheeler ownership has increased over the past year and the demand in the critical entry-level segment continues to be impacted. However, the green shoots of recovery in rural India are welcome news for India Auto Inc.

Scooter wholesales have surpassed the 500,000-unit mark for three srtaight months in August, September and October, also beecause OEMs would have ramped up production of popular and new models, ensuring their showrooms across the country are well stocked to cater to customer demand in the festive season. A gaggle of festive-season offers have also delivered the goods. While two-wheeler retail sales in October were down by 12% to 15,07,756 units, this can be put down to the tepid first fortnight. Expect fireworks in the November 2023 numbers.

ALSO READ:

Festive October powers strong double-digit growth for PV, two- and three-wheeler wholesales

Car and SUV makers capture festive demand, October sales soar to record 391,000 units

EV sales soar to 139,000 units in October and 1.23 million in first 10 months of 2023

RELATED ARTICLES

Electric Car and SUV Sales Jump 79% in H1, Set to Cross 300,000 Units in CY2026

Ajit Dalvi

09 Jul 2026

Ajit Dalvi

09 Jul 2026

Led by Tata Motors, Mahindra and JSW MG Motor, demand for electric passenger vehicles soared to 148,023 units in the fir...

Electric 2W Sales Race Past a Million Units in First 6 Months and 6 Days of CY2026

Ajit Dalvi

07 Jul 2026

Between January 1 and July 6, electric 2W OEMs have sold 10,05,279 scooters and motorcycles, which is 75% of CY2025’s re...

Bajaj Auto's Three-Wheeler Lead Narrows As Electric Rivals Mahindra And TVS Gain Ground

Autocar Professional Bureau

06 Jul 2026

Autocar Professional Bureau

06 Jul 2026

Despite retaining its position atop India's three-wheeler sales charts through FY26, Bajaj Auto's market share has stead...