Follow us

Follow us

India’s scooter market bounces back after four years with strong Q1 FY2023 numbers

After four years of a sales slowdown, things are finally looking up for the scooter market as Q1 numbers reveal. While Honda reigns supreme, TVS Motor Co makes strong market share gains.

19 Jul 2022

19 Jul 2022

17137 Views

Share -

17137 Views

Share -

With wholesale numbers for India Auto Inc across segments – passenger vehicles, two- and three-wheelers and commercial vehicles – returning strong year-on-year growth in the first three months of FY2023, the mood in the industry is cautiously optimistic. Admittedly, the Q1 numbers are on a low year-ago total but the fact of the matter is that sales are nearing pre-Covid levels.

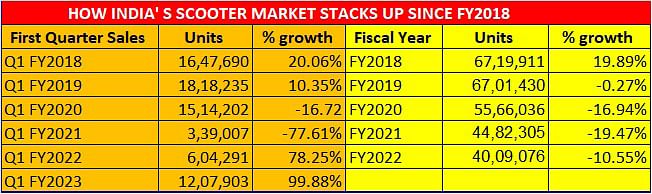

In what is an indicator that the revival is for real is that demand for two-wheelers, the most affordable form of motorised transport, is back after nearly four years for the beleaguered scooter industry. FY2018 with 6.7 million units sold in the domestic market was the last fiscal in which scooter OEMs had recorded growth (see 5-year sales table above). From FY2019, this segment has seen demand drop to a tad over 4 million units in FY2022. While the slowdown had set in FY2019, the Covid pandemic and the resultant lockdowns only exacerbated the situation. The motorcycle sector too was adversely impacted but not to the scale as scooters, more so because scooters still largely continue to be an urban mobility affair.

Now, the Q1 numbers, as released by industry body SIAM, augur well for FY2023. Total two-wheeler industry sales of 3,724,533 units in the April-June 2022 period are a 54% YoY growth (Q1 FY2022: 2,413,608 units). Of this, motorcycles accounted for 64% with 2,405,228 units (38% / Q1 FY2022: 1,740,308), scooters 32% with 1,207,903 units (100% / Q1 FY2022: 604,291), and mopeds 3% with 111,402 units (61% / Q1 FY2022: 69,009).

TVS Motor: the biggest market share gainer in Q1

A close look at the scooter market wholesales in Q1 FY2023, cumulatively as well as company-wise, reveals the numbers have doubled year on year. Of the nine OEMs in SIAM’s list, three have ceded market share – Hero MotoCorp, Suzuki and Piaggio – while TVS Motor Co is the one which has made the maximum market share gains: nearly 5 percentage points to 24.91% from 20.64% in Q1 FY2022. In FY2022, when it clocked cumulative sales of 866,851 scooters, TVS had a 21.62% market share. TVS’ best fiscal for scooters for FY2019 when it had sold over 1.2 million units – 12,41,327 units.

TVS’ total of 300,980 units in Q1 FY2023 marks robust 141% YoY growth with demand coming for all its four IC engine scooters – flagship Jupiter, NTorq, Wego and Pep+ – and also its electric iQube, which has seen demand grow 00% to 8,724 units from 946 a year ago. While the Jupiter, NTorq and Wego have contributed 272,790 units (up 00% / 110,662), the Pep+ accounted for 19,466 units, up 00% / 13,120.

Scooter market leader Honda, of course, is miles ahead of the competition with 562,050 units, which accounts for 00% of total sales in Q1. HMSI recorded 110% growth in its Q1 performance and increased its market share to 46% from 44% a year ago.

Suzuki, which has been among the movers and shakers of the scooter industry, with its Access in the past few years seems to be slowing down. The company’s Q1 sales of 162,927 units comprising the Access, Avenis and the Burgman Street, are up 44% on year-ago numbers.

Growth outlook: Promising

With schools and colleges opening and a good portion of office goers working in hybrid mode, which calls for a two to three days in the office, demand is picking up for scooters, which are typically seen as urban mobility solutions for different members of the family.

The shift to BS VI emission norms, necessitating a technology upgrade to more expensive electronic fuel injection, has made two-wheelers costlier than they were two years ago, which has affected the bottom of the pyramid on the consumer front. This is the reason why the past two years, which were impacted by the pandemic as well as job losses, saw demand sliding for entry-level scooters and commuter motorcycles. In comparison, the executive and premium segment products were not only unaffected but also saw decent growth.

Two-wheeler consumers are inherently cost sensitive, more so when it comes to vehicle servicing. In India, the aftermarket is a vital support when it comes to aftersales of two-wheelers and the lack of diagnostics equipment for BS VI vehicles, as well as the requisite know-how, is deterring some level of buyers from making a new purchase. High petrol prices as well as the lure of electric mobility, albeit at a higher initial cost, is also drawing buyers to electric scooters. Proof of this market trend is the electric two-wheelers accounting for 3.6% of retail sales in Q1 FY2023.

All in all, the upswing in scooter demand is welcome news for OEMs, who will be keeping their fingers firmly crossed that the need to scoot on a two-wheeler grows stronger in the coming months and quarters.

RELATED ARTICLES

TVS Sells 300,000 E-Scooters in Just 7 Months, Races Towards 550,000 in CY2026

Ajit Dalvi

03 Aug 2026

Ajit Dalvi

03 Aug 2026

TVS Motor Co is the fastest e-2W OEM to achieve 300,000 retail sales in a single year, beating Ola which took 8 months f...

Hero Vida Sells 100,000 E-scooters in 5 Months, Crosses 300,000 Milestone

Ajit Dalvi

03 Aug 2026

Hero MotoCorp’s Vida electric 2W brand, which logged its highest monthly sales in July, becomes the latest Indian OEM t...

TVS Sells Record 52,000 E-Scooters in July, E-2W Demand Jumps 77% to 192,000 Units

Ajit Dalvi

01 Aug 2026

Customer deliveries of electric 2Ws crossed 190,000 units for the second month in a row in July. Market leader TVS Motor...