Follow us

Follow us

India Auto Components Inc registers 12.6% growth in H1 FY24, clocks revenues of Rs 2.98 lakh crore

Riding on the strong demand for vehicles across categories, the domestic sale of components to OEMs contributed more than 85 percent of the industry’s total revenue. A depreciating rupee, and geopolitical tensions, however, continue to remain key headwinds for the industry, says ACMA.

20 Dec 2023

20 Dec 2023

6143 Views

Share -

6143 Views

Share -

The Indian Auto Components Inc clocked cumulative revenue of Rs 298,487 crore or $36.1 billion in H1 FY24 – April to September 2023 – to register a 12.6 percent year-on-year growth (H1 FY23: Rs 265,099 crore). The sector has been growing at a CAGR of 4.1 percent between FY19 and FY23, with robust domestic vehicle sales, a strong aftermarket, and rising exports from India contributing to the industry’s strong performance.

While the sale of components to domestic vehicle OEMs formed the chunk (85%) of the industry’s revenues at Rs 254,885 crore, registering a 13.9 percent YoY growth, exports in the first half of the ongoing fiscal grew by 8.7 percent to clock Rs 85,870 crore ($10.4 billion) in revenues (H1 FY23: Rs 79,033 crore). With healthy growth in the used vehicle parc, as well as the continuous formalisation of the repair and maintenance market, aftermarket turnover registered a 7.5 percent YoY growth to close at Rs 45,158 crore (H1 FY23: Rs 42,007 crore).

While the sale of components to domestic vehicle OEMs formed the chunk (85%) of the industry’s revenues at Rs 254,885 crore, registering a 13.9 percent YoY growth, exports in the first half of the ongoing fiscal grew by 8.7 percent to clock Rs 85,870 crore ($10.4 billion) in revenues (H1 FY23: Rs 79,033 crore). With healthy growth in the used vehicle parc, as well as the continuous formalisation of the repair and maintenance market, aftermarket turnover registered a 7.5 percent YoY growth to close at Rs 45,158 crore (H1 FY23: Rs 42,007 crore).

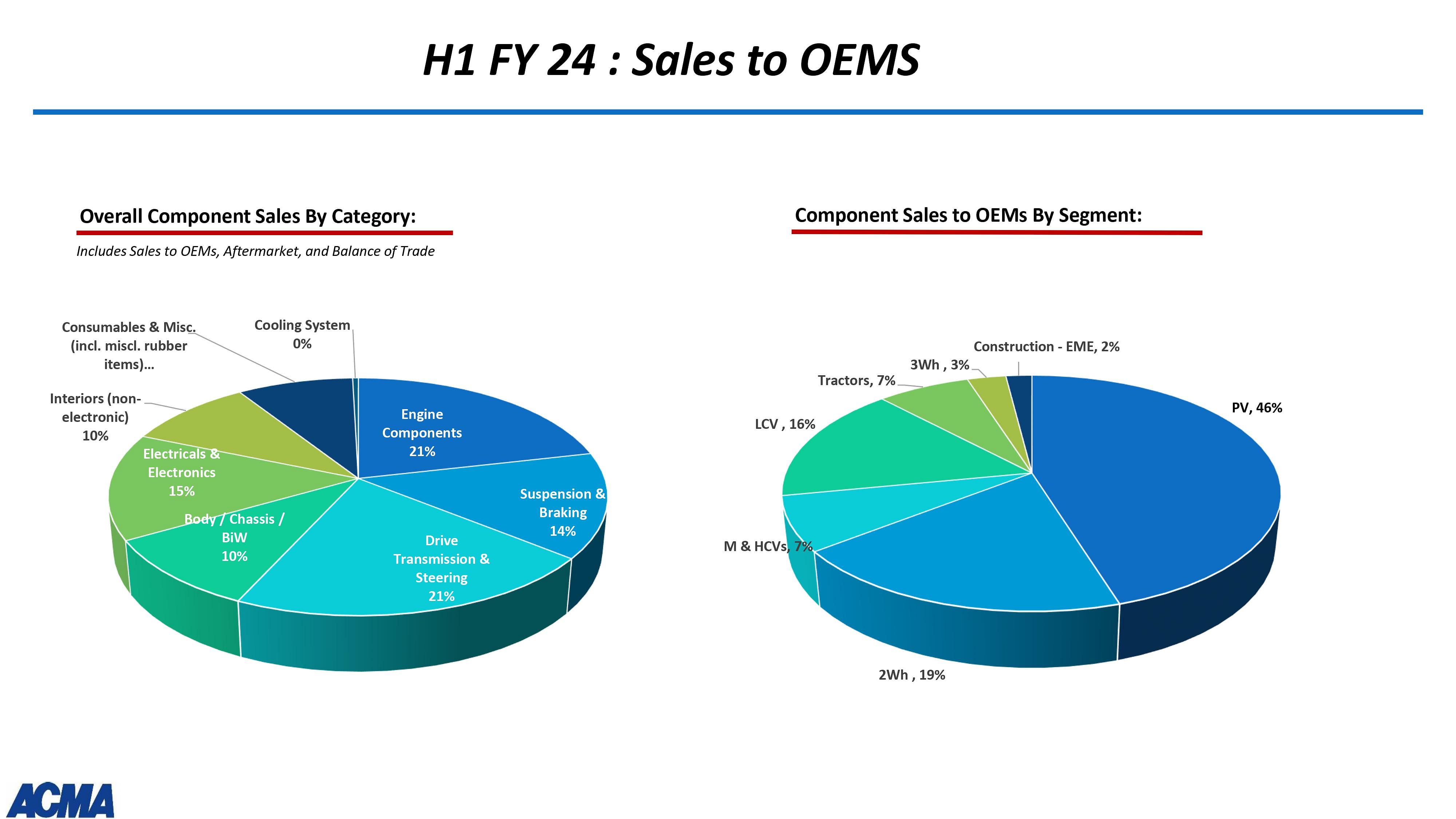

In the domestic market, passenger vehicle (PV) OEMs contributed to over 46 percent of the component industry’s revenues, while two-wheeler manufacturers at 19%, and M&HCV (7%) and LCV (16%) players followed behind. Despite electric vehicle sales growing by 50 percent in H1 FY24, engine components at 21 percent, along with drive transmission and steering components at 21 percent, formed the two major parts categories to be procured by vehicle manufacturers, as well as the aftermarket.

Electricals and electronics (15%), suspension and braking components (14%), as well as body and chassis systems (10%) were the other major categories of parts that were supplied by the Indian automotive component manufacturers in H1 FY24 in the domestic market. According to the Automotive Component Manufacturers Association of India (ACMA), there has been a perceptible shift in consumer preferences, with larger / more powerful vehicles registering higher growth across segments.

Utility vehicles, including SUVs, reported a 57 percent share of the PV segment in H1 FY24, growing 8 percentage points from the 49 percent share in H1 FY23. Similarly, there was around 70 percent increase in the sales of motorcycles with a 200-250cc engine capacity, while M&HCVs maintained a 35 percent share amongst all commercial vehicles in the first half of the ongoing fiscal.

According to Vinnie Mehta, Director General, ACMA, “With vehicle sales and exports displaying a steady performance, the automotive component industry demonstrated a strong 12.6 percent growth, scaling to a turnover of Rs. 2.98 lakh crore (USD 36.1 billion), in H1 FY24. Component supplies to all segments of the industry remained steadfast.”

Shradha Suri Marwah, President, ACMA, added and said, “With vehicle sales across all segments reaching pre-pandemic levels and with the mitigation of supply-side challenges such as the availability of semiconductors, high input raw-material costs as well as non-availability of containers, particularly witnessed during the pandemic, the auto components sector witnessed a steady growth in both domestic and the international markets in the first half of FY24.”

“Considering the strong industry performance during the festive season, which witnessed robust sales across most segments of the vehicle industry, I am optimistic that we will witness good performance from the auto components sector in FY24. The components industry continues to make investments for the purposes of higher value-addition, technological upgradation, and localisation, to stay relevant to both domestic and international customers,” Marwah added.

Export-import H1 performance

While automotive component exports from India grew by 8.7 percent in H1 FY24 to Rs 85,870 crore, imports registered a 9.5 percent uptick to Rs 87,425 crore. According to ACMA, the global trade underperformed due to the economic slowdown in European markets, higher inflation rates, and an appreciation in the value of the dollar, which went up by 5.7 percent in the first six months of FY24, compared to the same period in the previous financial year.

While automotive component exports from India grew by 8.7 percent in H1 FY24 to Rs 85,870 crore, imports registered a 9.5 percent uptick to Rs 87,425 crore. According to ACMA, the global trade underperformed due to the economic slowdown in European markets, higher inflation rates, and an appreciation in the value of the dollar, which went up by 5.7 percent in the first six months of FY24, compared to the same period in the previous financial year.

The decreasing value of the Indian rupee compared to the dollar led to a surge in the automotive components trade deficit, which remained almost similar at US$ 200 million as that in H1 FY23. However, with a higher exports CAGR of 5.7 percent between FY19 and FY23, compared to that of 2.7 percent for component exports during the same period, “we are confident that exports will overtake imports over a period of time,” said Mehta.

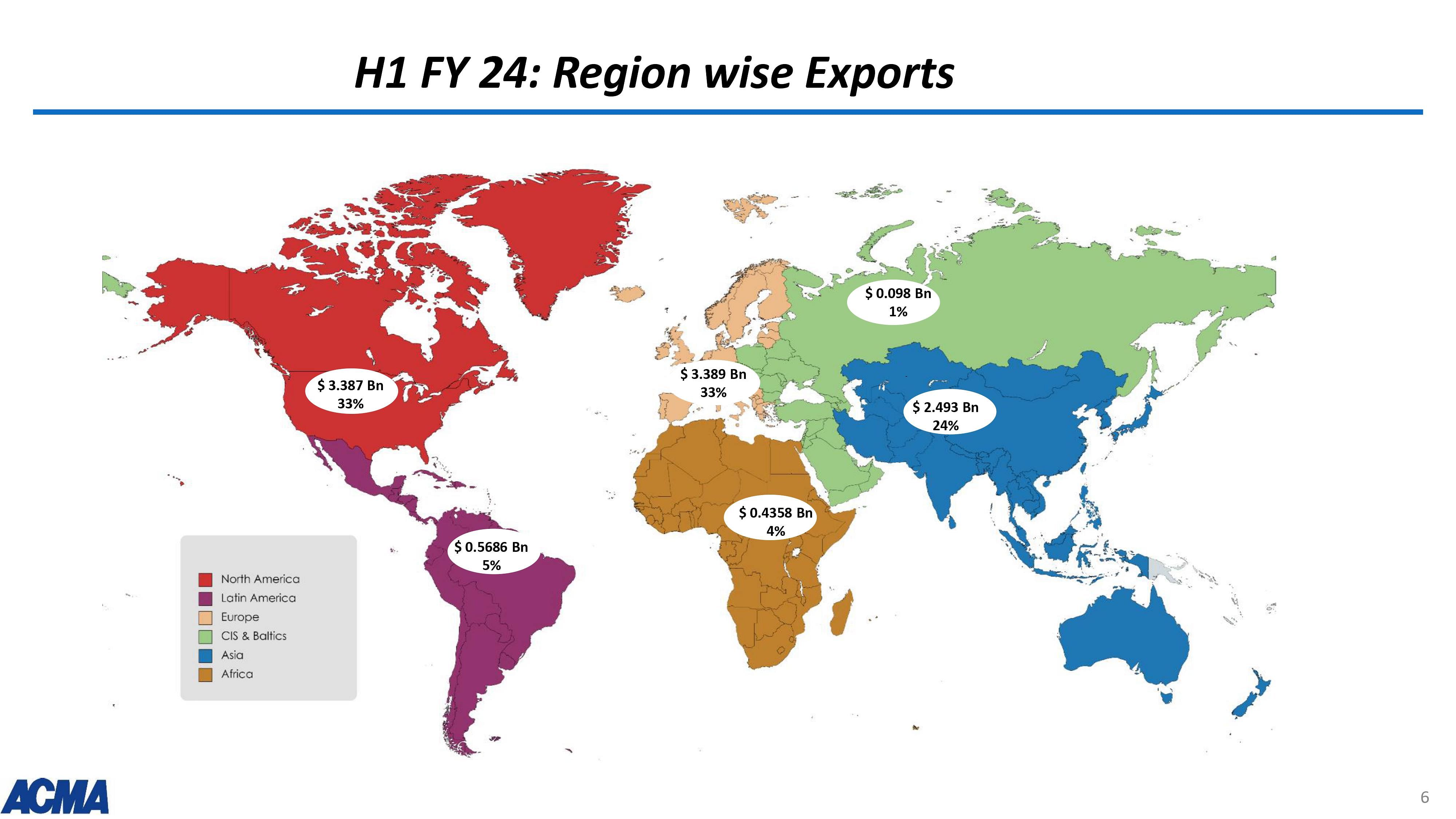

North America and Europe continued to remain the largest export markets for Indian component manufacturers with a 33 percent share each of the total component exports from the country. Asia followed behind at a distant 24 percent, while Latin America (5%) and Africa (4%) were the other key markets. Furthermore, exports of made-in-India automotive components to South Asian markets like Bangladesh, Nepal, and Sri Lanka declined owing to muted economic activity in the region.

The USA emerged as the largest export destination for India Components Inc with a 28 percent share of the total pie, while Germany (8%), Turkey and the UK contributed 4 percent each. At 34 percent, drive transmission and steering components, followed by engine components (20%), electrical and electronics (11%) were the major categories of parts to be exported from India in H1 FY24.

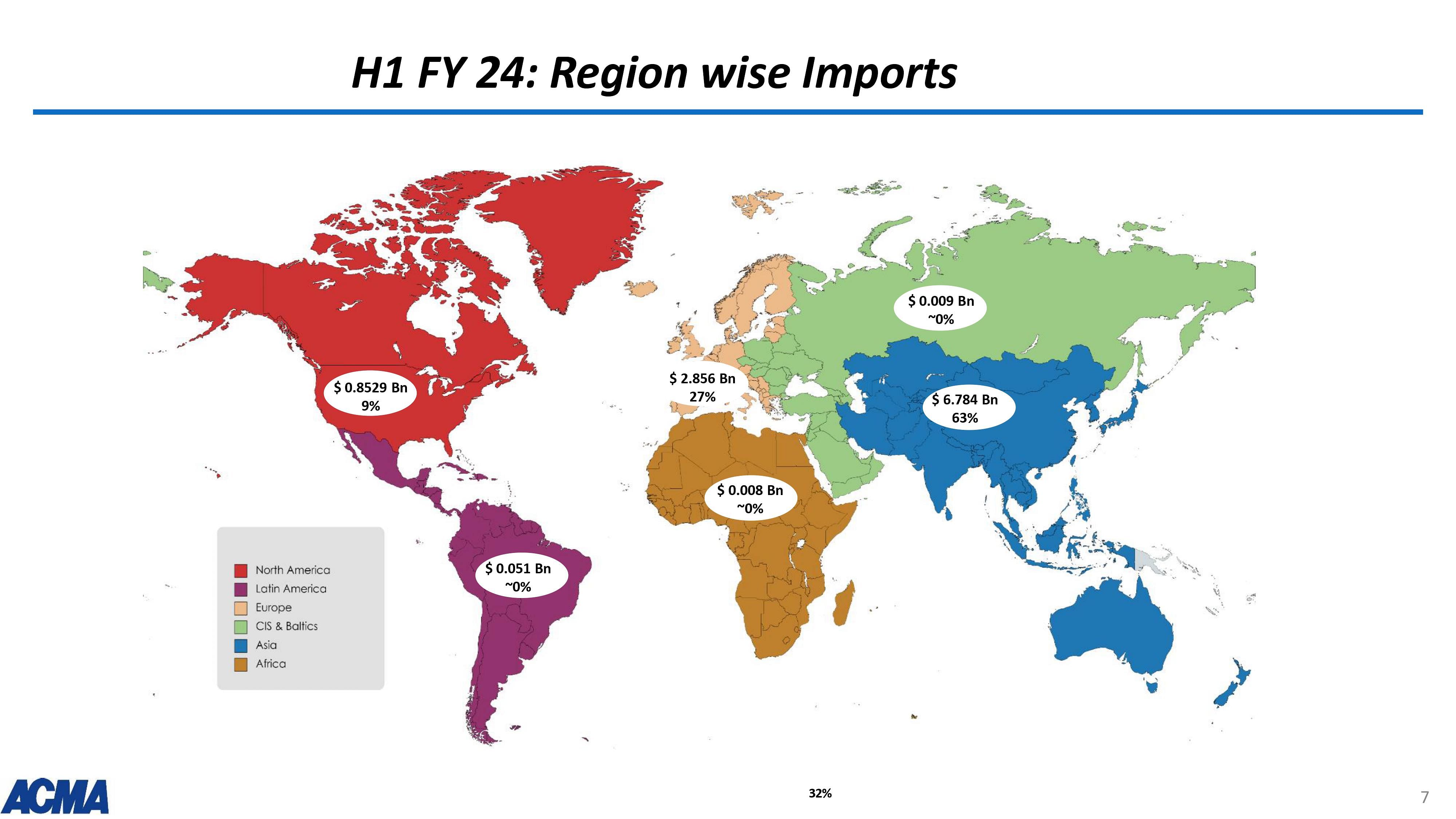

In terms of imports, China emerged as the largest base for automotive components coming into India with a 28 percent global share, followed by Germany (12%), South Korea (10%), Japan (9%), USA (7%), and Thailand at 6 percent, among other nations. Engine components (12%), body and chassis systems (18%), suspension and braking (14%), and electrical and electronics (7%) were the key categories of components that were imported between April and September 2023.

FY24 component sector outlook

With a high estimated GDP growth projection of 6.5 percent for FY24 and FY25, along with the government’s continued push on infrastructure development, and clean technology, as well as the robust demand for vehicles in the domestic market, ACMA is hopeful of a sustained positive industry growth in the short- to mid-term future. However, geopolitical uncertainties, recessionary trends in Europe and the US, as well as the high GST rate on automotive components continue to remain the key headwinds ahead of the industry as it steps into the new calendar.

“Considering that the macro-economic factors are good, we expect the industry to close FY24 at a 10-15 percent growth rate. While we do not expect any major headwinds, other than the slight worry on the geo-political front that could affect exports, things at the domestic front look steady,” said Mehta.

RELATED ARTICLES

Honda Cars India Announces Price, Begins Deliveries of ZR-V e:HEV

Shruti Shiraguppi

25 Jul 2026

Shruti Shiraguppi

25 Jul 2026

The hybrid SUV is priced at Rs 47,99,000 (ex-showroom, Delhi) and is imported as a completely built unit from Japan.

Maruti Suzuki Launches New Brezza Turbo Boosterjet at ₹7.39 Lakh

Shruti Shiraguppi

25 Jul 2026

The SUV is offered with a new 997cc turbo-petrol engine, the existing K15C petrol engine and an S-CNG variant.

US OEMs Trend Towards Hybrids, Chinese Towards BEVs: Sona Comstar CFO

Mukul Yudhveer Singh

25 Jul 2026

Mukul Yudhveer Singh

25 Jul 2026

North America, Sona Comstar’s largest overseas market, contributed 26% of its Q1 FY27 revenue, while the company secured...