Follow us

Follow us

Money talks in the EV race

New mobility solutions, especially electric vehicle start-ups, are attracting a huge chunk of the environmental, social and governance (ESG) investments. But what’s the longer term outlook and will these sustain the momentum?

23 Aug 2021

23 Aug 2021

11201 Views

Share -

11201 Views

Share -

funding future technologies and a large chunk of capital is now earmarked for ESG investment.")

The recent investment flurry in Ola is reflective of the rising SPACs (Special Purpose Acquisition Company)funding future technologies and a large chunk of capital is now earmarked for ESG investment.

Covid-19 no doubt put the brakes on travel near and far but it surely accelerated the move towards next-gen mobility or green mobility. One of the most striking examples of this trend is the much-hyped launch of Ola e-scooters on August 15 at a disruptive Rs 99,999. With state subsidies are factored in, not only does the pricing undercut its closest competitors like the TVS iQube (Rs 101,000), Bajaj Chetak (Rs 142,000) and the Ather 450, but it is also a telling comment on the expected demand outlook.

While the jury is still out on the long-term sustainability of the Ola model, many believe Given the scale and projection, it seems that Ola is almost mirroring the strategy adopted by Tesla.

Can Ola become a Tesla of two-wheelers?

Private investor Ajay Bagga draws up the points of similarities between the two. “Ola Electric Mobility has just reached its first launch stage, so a comparison with industry pioneer Tesla would look premature and stretched. However, the strategies underlying Ola Electric are similar to those of Tesla:

- Scale: Like Tesla’s Gigafactories, Ola Electric’s Future Factory is a massive 500- acre plant with capability to produce 10 million two-wheeler EVs per annum.

- Marketing savvy: Like Tesla’s $100 booking amount for Cybertruck, Ola opened a Rs 499 booking window for its e-Scooter, garnering 100,000 bookings in 24 hours.

- Celebrity CEO: Ola’s CEO Bhavish Aggarwal has been using his social media account to create a buzz. Elon Musk at Tesla has long used his social media to promote his company.

- Breakthrough products: Ola is claiming product superiority with a lot of indigenous content and affordability. Tesla followed the product superiority plank and also launched a more affordable EV to capture that segment.

In short, the two companies, though at different stages in their platform lifecycles, present very similar strategies.”

The obvious question that comes to mind is: Do the valuations support the claims? Can Ola become what Tesla managed? Deven R Choksey, MD, KR Choksey Investment Managers believes, “I think this company would probably not get the valuation of an automobile company but they will get a valuation of a start-up company, which is basically disrupting the entire transportation. Going forward, it is possible in bigger cities people may not be buying the vehicles for themselves but use the vehicle for commuting for a short distance. This is where I think a company like Ola is going to be make it big.”

What’s driving investment in EVs?

Demand for EVs is surely picking up and companies across the gamut of the EV ecosystem are betting that the consumer mindset has evolved during the lockdown. Global sales are expected to approach five-and-a-half million units this calendar year – roughly the size of the total global EV fleet just three years ago.

Ajay Bagga, private investor and director, says: “This has been a combination of a lot of liquidity chasing disruptive and exponential potential auto businesses that can be the next Tesla. The most crucial ingredient in that recipe is blank-check companies or SPACs (Special Purpose Acquisition Company) focused on buying electric-vehicle makers ESG (environmental, social and governance) goals, climate change commitments, disruptive products and new business models based on software driving automobiles are driving this interest.”

Deven R Choksey, MD, KR Choksey Investment Managers, adds: “Most of these start-ups are driven by the disruptive approach. I think when a Zomato kind of a company would come into play, they may not be able to quantify as to what disruption they will create but in the process, they will be in a position to create a large amount of customer database, which they did. Now, this is something which is also similarly happening for most of the EV companies, the kind of disruption that they would create for getting many folds.”

Kishor Ostwal, CMD CNI Research points out that, “Start-ups have a major role in reducing the cost of EVs and make it necessity like a petrol car. In short, the EV segment is a space where start-ups can play a vital role. Expect to see a lot of PEs investing in such start up.”

What’s the limiting factor for major OEMs?

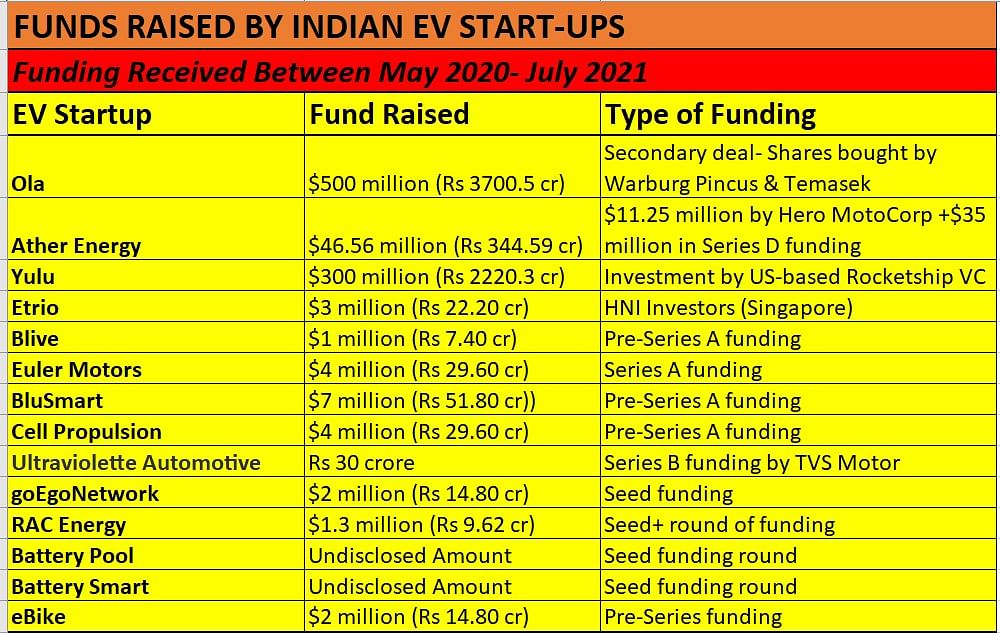

While on the one hand, Indian start-ups have attracted upward of $700-800 million in investment in the past year or so, why are established OEMs not much in the running. If anything, you are seeing even major OEMs putting their money power behind many of the start-ups…. Hero is backing Ather Energy, TVS invested in Ultraviolette while Yulu plans to expand its fleet by deploying Bajaj-built electric scooters by end-2021.

Choksey explains this is primarily because “the bigger companies have their priorities lined up elsewhere. Obviously, they will not concentrate on smaller parts. Rather, they would be interested in creating the ecosystem in which the vendors will be prepared for the purpose of supply to the company eventually. I guess that is why you are going to see the valuation remaining on the higher side.”

Bagga says while the newbies may have some initial advantage, it is only a matter of time before the conventional industry leaders pose stiff competition, “Established players are innovating and planning to launch their EV variants. However, the new players have the benefits of deep-pocketed investors, no legacy costs, no legacy systems or production lines and no legacy labour to be reskilled. Eventually, legacy players will recalibrate their product and service offerings to compete with the EV entrants.”

The affordability argument

In fact lesser travel cost, smaller budgets and lesser maintenance costs all point to another key characteristic of EVs – affordability. It is true that the initial cost of most EVs, be it two- or four-wheelers, is high at the moment but Ostwal believes, with volume and scale, we will see “reduction in the cost of components and EV utility.”

Choksey points out that the difference in operation costs will be the ultimate deal clincher, “Currently, I think a commercial vehicle which runs on a conventional IC engine, may end up paying about 40 rupees per kilometre. If you use an electric CV, you may end up paying Rs 8 a kilometre for the same distance. So, you are operating the entire business at one-fifth of the cost. EVs are going to disrupt the conventional IC-engine vehicles largely on the operating cost parameter.”

No doubt, the EV segment is seeing massive investment interest for now but the ultimate test is in managing mass adoption which remains elusive globally. Advancement in battery technology and infrastructure development supporting the entire EV ecosystem are critical factors to achieve full potential. As most analysts agree, ICE vehicles are not going away in a hurry and as a result, the valuation debate also continues as companies jostle to balance volume and scale along with development in technology to reduce costs.

RELATED ARTICLES

Cosmo First diversifies into paint protection film and ceramic coatings

Autocar Professional Bureau

17 Jul 2025

Autocar Professional Bureau

17 Jul 2025

The Aurangabad, Maharashtra-based packaging materials supplier is leveraging its competencies in plastic films and speci...

JSW MG Motor India confident of selling 1,000 M9 electric MPVs in first year

Autocar Professional Bureau

11 Jul 2025

The 5.2-metre-long, seven-seater luxury electric MPV, which will be locally assembled at the Halol plant in Gujarat, wil...

Modern Automotives targets 25% CAGR in forged components by FY2031, diversifies into e-3Ws

Autocar Professional Bureau

05 Jul 2025

The Tier-1 component supplier of forged components such as connecting rods, crankshafts, tie-rods, and fork bridges to l...