Follow us

Follow us

Mahindra reports net profit of Rs 162 crore for Q2 FY2021, down 88%

The net profit came down significantly as exceptional items on account of impairments have led to a drop for the current quarter as compared to the corresponding quarter in the previous year.

4143 Views

4143 Views

Mumbai-headquartered automotive major Mahindra & Mahindra announced its financial results for the Q2 FY2021. The company reported consolidated revenue of Rs 11,590 crore, a growth of 6 percent YoY (Q2 FY2020: Rs 10,935 crore), profit after tax of Rs 162 crore, (-88% YoY) compared to a profit of Rs 1,355 crore reported for the same period last year. The net profit came down significantly as exceptional items on account of impairments have led to a drop for the current quarter as compared to the corresponding quarter in the previous year.

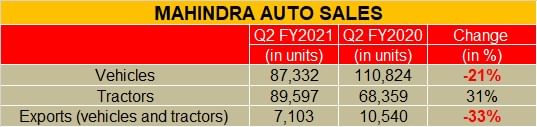

The OEM says in Q2 FY2021 the Indian auto industry including two-wheeler was just 1 percent lower that the comparative quarter in the previous year. It is after six quarters that the industry reported a flat performance with the PV industry growing 17 percent after 8 consecutive quarters of de-growth. Within the PV segment the SUV segment grew by 21.2 percent.

The growth was driven by good demand especially in semi-urban and rural parts of the country, pent-up demand, preference for personal mobility, new launches and availability of affordable finance. As a result of positive outlook in the rural and agri sectors, the Pick-Up segment (2-3.5-tonne GVW) after six quarters of reduction saw positive momentum, with a growth of 6.2 percent over previous year with volumes almost at the pre-Covid levels of FY2020.

Mahindra says with the overall economy yet to gain momentum and with excess capacity in the transportation ecosystem, the M&HCV goods industry volumes stand at just 23,936 units, which is a de-growth of 40.5 percent over previous year. With partial reopening up of the economy in the months of May and June, and then subsequent relaxations allowed in the reopening phases, the economy at large is adapting to operating and living in a post-Covid era. The auto industry ecosystem including suppliers and dealers were quick to bounce back and operations now are near normal despite some isolated pockets of supply side constraints that still remain.

In Q2 FY2021, the Indian tractor industry reported a growth of 41.4 percent, which is the highest ever Q2 quarter growth for the tractor industry. Timely relaxation of the Covid lockdown restrictions for the agricultural sector supported by healthy reservoir levels, good increase in MSP for Kharif crops and important reforms in the agri sector announced by the government focused on improving the state of agriculture in India in the mid- to long-term have helped tractor demand to bounce back after April 2020. On the back of these positive factors, the OEM expects that tractor demand will remain robust during the upcoming festive season.

On August 15, Mahindra unveiled the all-new Thar and launched it on October 2, 2020, which has witnessed robust demand from the customers leading to bookings crossing the 20,000 mark.

The company says on the back of its strong performance in tractors combined with its ruthless focus on cost has achieved a very high OPM and the PAT (before EI) in Q2 FY2021 , which is just 3 percent lower than Q2 FY2020, despite a substantial fall in other income in the current quarter as compared to the previous year quarter.

Urban demand may continue to lag

Mahindra says the real GDP growth in FY2021 is expected to be negative at 9.5 percent, as per RBI’s latest estimates with risks tilted to the downside. However, economic activity, seen through the prism of high frequency indicators, seems to be stabilising after the unprecedented shock in Q1 wherein the GDP shrank 23.9 percent YoY. With government spending and rural demand anchoring economic activity, manufacturing and some categories of services have gradually recovered in Q2.

Proactive steps from the RBI have kept domestic financial conditions easy and system liquidity in surplus. Kharif sowing and the recent agricultural reforms portend well for the rural economy. However, the turnaround in urban demand may continue to lag especially the contact-intensive services sectors. Manufacturing capacity utilisation is expected to recover in Q3 and activity to gain some traction from Q4 onwards. However, capex and exports are likely to remain subdued.

Importantly, the IMF estimate for global GDP growth for 2020 has been revised upwards slightly to -4.4% from -5.2% (June 2020); and expected to be around +5.2% in 2021. As economies reopened and released constraints on spending, overall activity normalised faster than anticipated. GDP outruns for the second quarter surprised on the upside in China, US and Eurozone (economies contracted at a historic pace but less severely than projected). However, several countries are seeing a second wave and have re-imposed local lockdowns which may hurt economic activity.

RELATED ARTICLES

Cosmo First diversifies into paint protection film and ceramic coatings

Autocar Professional Bureau

Autocar Professional Bureau

17 Jul 2025

17 Jul 2025

The Aurangabad, Maharashtra-based packaging materials supplier is leveraging its competencies in plastic films and speci...

JSW MG Motor India confident of selling 1,000 M9 electric MPVs in first year

Autocar Professional Bureau

11 Jul 2025

The 5.2-metre-long, seven-seater luxury electric MPV, which will be locally assembled at the Halol plant in Gujarat, wil...

Modern Automotives targets 25% CAGR in forged components by FY2031, diversifies into e-3Ws

Autocar Professional Bureau

05 Jul 2025

The Tier-1 component supplier of forged components such as connecting rods, crankshafts, tie-rods, and fork bridges to l...