Follow us

Follow us

Trading places: UV share of PVs jumps to 65%, car share plunges to 31% in April-Dec

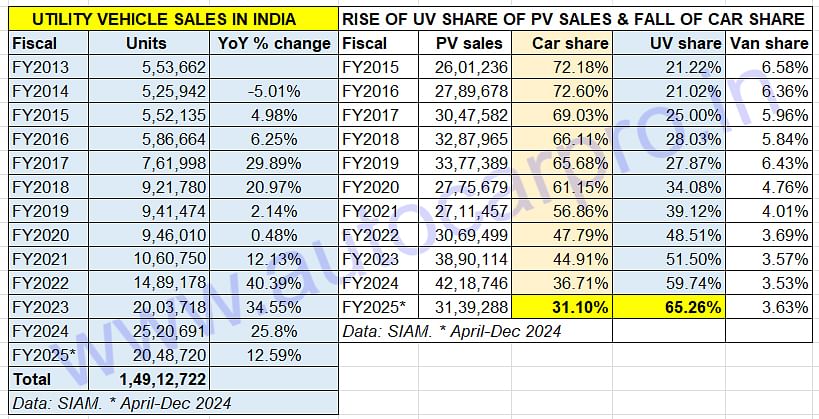

The SUV-MPV and passenger car segments have traded places in the past decade. While utility vehicles’ share of passenger vehicle sales has jumped three-fold to 65% from 21% in FY2015, hatchbacks and sedans, which commanded a 72% share in FY2015, has nosedived to a record low of 31% in the current fiscal year.

26 Jan 2025

26 Jan 2025

10643 Views

Share -

10643 Views

Share -

India’s passenger vehicle market, with 31,39,288 units or 3.13 million units in the April-December 2024 period, is well set to surpass the 4-million-units mark for the second fiscal year in a row. In FY2024, India PV Inc had registered record wholesales of 4.21 million cars, SUVs, MPVs and vans, an increase of 8% over FY2023’s 3.89 million units. What is enabling the segment to achieve the big number is the consistently growing contribution of the utility vehicle (UV) sub-segment.

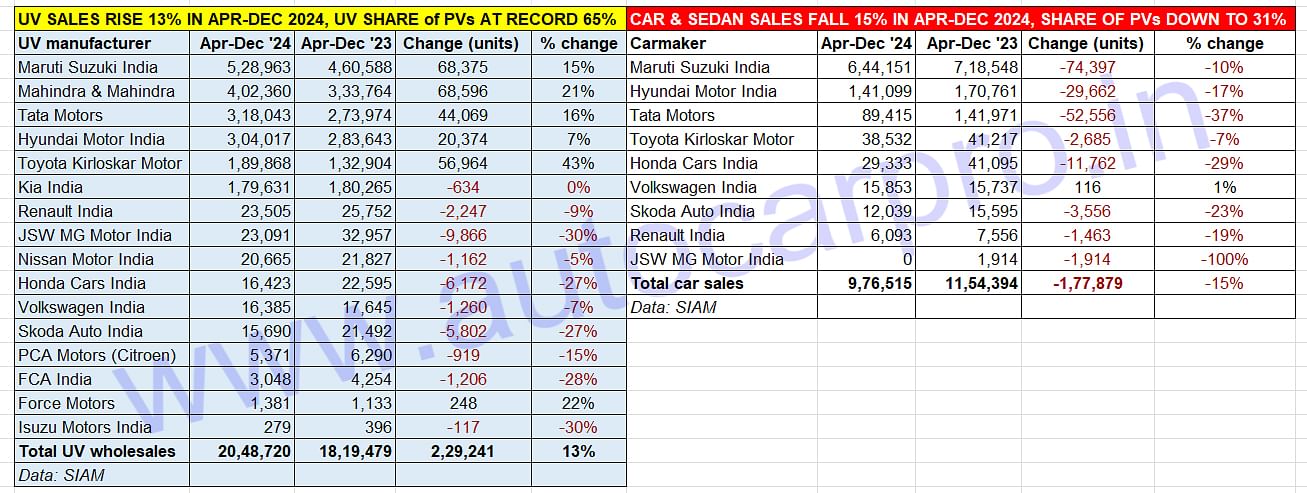

At the top is UV market leader Maruti Suzuki India with 528,963 units, up 15% YoY, and a 26% share of the UV market (see data table below). Mahindra & Mahindra, which has a 10-model-strong portfolio, is the No. 2 with 402,360 units, up 21% YoY and a 20% UV market share. Tata Motors is currently ranked third with 318,043 units, up 16% YoY and a 15.52% market share.

Exactly 14,000 UVs behind Tata is Hyundai Motor India with 304,017 units, up 7% YoY, and a market share of 15 percent. Toyota Kirloskar Motor, which is having a fine run, sold 189,868 units, up 43% YoY, has a 9% market share and is followed by Kia India which dispatched 179,631 units but saw flat (0% YoY) sales for an 8.76% market share.

While SUV and MPV wholesales at 2.04 million units have risen 13% YoY in April-December 2024, demand for hatchbacks and sedans continues to drop -- the 976,515 units are a 15% YoY. decline

While SUV and MPV wholesales at 2.04 million units have risen 13% YoY in April-December 2024, demand for hatchbacks and sedans continues to drop -- the 976,515 units are a 15% YoY. decline

Of this lot, Mahindra & Mahindra has sold the highest additional number of UV in the past nine months – 68,596 units compared to Maruti Suzuki (68,375 units), Toyota Kirloskar Motor (56,964 units), Tata Motors (44,069 units) or Hyundai Motor India (20,374 units).

With three months still left in this fiscal year, all these six OEMs with SUV-heavy portfolios are well set to register record UV sales on FY2025. While Maruti Suzuki needs to sell 113,333 UVs more (FY2024: 642,296 units), Mahindra & Mahindra just 54,504 units more (FY2024: 459,864 units), which it will achieve either in January 2025 or early February. Tata Motors, which had clocked sales of 388,418 UVs in FY2024, is currently 70,375 units away from that figure. Hyundai, ranked third in FY2024 (388,725 units, 15.42% UV share) is currently 84,708 UVs shy of that number. Toyota Kirloskar Motor will have already surpassed its FY2024 score (191,065 units, 7.57% UV share) in the first few days of January 2025. Kia India, with sales of 179,631 UVs in April-December 2024, is the farthest at this from its FY2024 total of 2,45,634 UVs – the difference is 66,003 units.

Trading places: 10 years ago, in FY2015, the hatchback and sedan market commanded a 72% share of overall passenger vehicle sales. That has now nosedived to a record low of 31% in April-December 2024 while the SUV-MPV share has jumped to 65% from 21% in FY2015.

Trading places: 10 years ago, in FY2015, the hatchback and sedan market commanded a 72% share of overall passenger vehicle sales. That has now nosedived to a record low of 31% in April-December 2024 while the SUV-MPV share has jumped to 65% from 21% in FY2015.

UV SHARE CATAPULTS TO 65% FROM 21% IN FY2015, CARS' SHARE NOSEDIVES TO 31% FROM 72%

A close look at decadal wholesales data reveals just how much the PV market and consumer buying preferences have changed. Hatchback and sedan sales in FY2015, at 18,77,706 units of 2.6 million PVs, accounted for three out of every four PV sales. A decade and a little more down the line, in April-December 2024, demand for this vehicle category has nearly halved to 31% – 976,515 units of the 3.13 million PVs sold in the first nine months of the current fiscal.

Along with the accelerated shift to SUVs, other factors like hatchback and sedan prices rising by over 50% over the past few years due to increased cost inputs and regulatory upgrades as also the much-slackened demand for entry-level hatchbacks as a result of stagnating income in that buyer segment, have played spoilsport.

In sharp contrast to the sales slide of the hatchback and sedan market, the sales graph of the UV segment has soared and how. From the 552,135 UVs sold in FY2015 through to the record 25,20,691 units sold in FY2024, and the 2.04 million units sold in April-December 2024, the dynamic growth of the SUV and MPV market has been stellar.

Utility vehicle sales surpassed the million-units mark for the first time in FY2021 and since then the numbers have only accelerated.

Utility vehicle sales surpassed the million-units mark for the first time in FY2021 and since then the numbers have only accelerated.

The fastest vehicle category to put the pandemic blues behind them, SUV and MPV sales surpassed the million units mark for the first time in FY2021 (10,60,750 units, up 12%), and then have for the next three fiscals delivered high double-digit growth. While FY2022 saw 1.48 million-unit sales and sterling 40% growth, the two-million-milestone was achieved in FY2023 at an equally robust 34% YoY growth rate. And the UV segment has wrapped up FY2024 with 26% growth at 2.52 million units. Ample reason and more why every OEM worth its wheel wants to have a slice of the SUV market.

The consumer in this segment, particularly for SUVs, is truly spoilt – including the 16 SIAM member companies and 14 luxury OEMs there are all of 32 OEMs with an estimated 128 UV models and a mind-boggling 1,001-odd variants! Just like its commanding market share, the UV segment also rules the roost in terms of models and accounts for 62% of the estimated 204 passenger vehicle models on sale and 73% of the 1,370-odd variants as of December 2024.

Of the mainstream players, Mahindra, Maruti Suzuki and Toyota are the ones with the highest number of models – 8 each. While M&M’s SUV portfolio covers 103 variants, Maruti has 65 and Toyota 51 variants. However, Tata Motors, with six SUVs (including the Nexon EV and Punch EV), has the highest number of variants – 154! And the luxury pack comprises 16 carmakers encompassing 60-odd models and 150-plus variants.

Since FY2023, when it crossed two million units (20,03,718 UVs, up 34%) for the first time in a fiscal, the UV segment has been the mover and shaker of the overall PV category, helping buffer the marked decline in demand for passenger cars and sedans.

Of the total 4.21 million PVs sold in FY2024, UVs accounted for 25,20,691 units (up 26% YoY) and 59.74% of entire PV sales. Not only was this a big jump over the 51.50% share that UVs had in FY2023 but it was also the first time that UV dispatches surpassed the 2.5-million-units mark. What’s more, UV sales helped buffer the sharp 11% decline in passenger car and sedan sales – from 1.74 million units to 1.54 million units in FY2024. That’s just the reason why all the vehicle manufacturers with SUV-laden portfolios registered handsome gains in FY2024.

There’s a repeat of the same scenario in the first nine months of FY2025. Between April-December 2024, a total of 20,48,720 UVs were dispatched by 16 manufacturers to showrooms across India, which is a 13% increase over the year-ago sales (April-December 2023: 18,19,479 UVs). Driving the charge are six manufacturers, each with UV-heavy portfolios and each with six-figure sales. Given the current momentum and a host of new SUVs launched in the first couple of months this year, expect the UV segment to register record wholesales of around 2.65 million units or more.

RELATED ARTICLES

Maruti Brezza Crosses 1.5 Million Sales Ahead of New Model Launch

Ajit Dalvi

24 Jul 2026

Ajit Dalvi

24 Jul 2026

Maruti Suzuki’s game-changing Brezza, which spawned the compact SUV segment a decade ago and is the category’s best-sell...

Electric Car and SUV Sales Jump 79% in H1, Set to Cross 300,000 Units in CY2026

Ajit Dalvi

09 Jul 2026

Led by Tata Motors, Mahindra and JSW MG Motor, demand for electric passenger vehicles soared to 148,023 units in the fir...

Electric 2W Sales Race Past a Million Units in First 6 Months and 6 Days of CY2026

Ajit Dalvi

07 Jul 2026

Between January 1 and July 6, electric 2W OEMs have sold 10,05,279 scooters and motorcycles, which is 75% of CY2025’s re...