Follow us

Follow us

India auto retails soar 48% in festive October, all vehicle segments register double-digit growth

At nearly 2.1 million units and all segments recording double-digit growth, October 2022 numbers indicate steady return to pre-Covid sales; ICE three-wheelers sole sub-segment to see decline vs October 2019.

07 Nov 2022

07 Nov 2022

13741 Views

Share -

13741 Views

Share -

The retail sales numbers, which portray the real-world story of automobile sales on ground, are out for the month of October 2022. At nearly 2.1 million units (20,94,378 units) for five vehicle segments – two- and three-wheelers, passenger vehicles, passenger vehicles, tractors and commercial vehicles – the year-on-year growth is a robust 47.63 percent. Importantly, what indicates the sales revival at India Auto Inc is that October 2022’s numbers are an 8.32% growth of pre-Covid October 2019’s 19,33,484 units.

What also helped charge retail numbers last month was that all of October was part of the 42-day festive period in India, which saw Navrati and Diwali in it. Commenting on the industry’s performance, FADA President, Manish Raj Singhania said, “Auto retail for October 2022 saw an overall growth of 48%. With most of the month under festive period, the sentiments were extremely positive across all categories of dealership outlets.”

He added, “Even when compared to the pre-Covid month of 2019, overall retails for the first time closed in the green by growing 8 percent. Except for three-wheelers, which saw a marginal dip of 0.6%, all the other categories like two-wheelers, PVS, tractors and CVs grew by 6%, 18%, 47% and 13% respectively.”

Electric three-wheelers rule, two-wheeler volumes rev up

Demand for three-wheelers rose 66% to 66,763 units (October 2021: 40,251) – it remains the sole vehicle category to be below pre-Covid October 2019 sales (67,160 units), albeit marginally at 0.59 percent. Given the momentum of growth, that deficit should be crossed soon.

The marked shift to electric mobility is clearly seen in the three-wheeler segment. Of the total 66,763 units sold, 49% or 32,468 units are electric three-wheelers comprising 30,519 passenger-carrying variants (up 91%) and 1,949 goods transporters (63%). Not only that, sales of electric passenger three-wheelers were higher than their ICE siblings (27,337 units) by 3,182 units, depicting the trend in the segment. A close look at the overall FADA sales table reveals that the three IC-engined three-wheeler sub-segment are the only ones in the red and negative territory when compared to October 2019 retails. Clearly, ICE is no longer the favourite in the three-wheeler segment. According to FADA, three-wheeler numbers would have been higher last month had it not been for permit issues in some regions that impacted sales.

In what marks a welcome return of demand for two-wheelers, the segment saw retails of 15,71,165 units, up 51% over October 2021’s 10,39,845 units, 41% over October 2020’s 11,11,785 units and 5.79% over October 2019’s 14,85,240 units. While this could be put down to a rush of festive season buying, what’s vital for the sector is that the demand pattern sustains in the months to come.

Average dealer inventory for the two-wheeler segment was between 40 to 45 days at the end of October.

PVs and CVs shine

The passenger vehicle segment, which has been leading the India auto growth story saw total retails of 328,645 units, up 41% YoY and translates into 10,601 units being sold every day in October 2022. What’s more, last month’s PV sales are 25% better than October 2020’s 262,274 units and 18% better than October 2019’s 278,867 units. FY2023 is set to be a record-setting fiscal for this segment.

At the end of October 2022, the average dealer inventory for the PV segment was between 35 to 40 days.

According to Singhania, “The PV segment showed a growth of 41% YoY and 18% when compared to 2019. PV segment continues to see extremely high demand especially in SUV and Compact SUV segments including higher variants in most of the product categories. With better vehicle availability coupled with new launches, the segment also witnessed the best festive period in a decade by surpassing 2020 festival sale by 2%.”

The CV sector, for whom growth comes in a cyclical pattern of four-odd years, is back on track. October retails were 74,443 units up 25% (October 2021: 59,363 units), on the back of demand from multiple sectors. Singhania said: “Festivities ignited better fleet sales. With mining and infrastructure projects increasing in various regions, demand has been keeping well and is also coming back on track.”

Festive month is best in four years

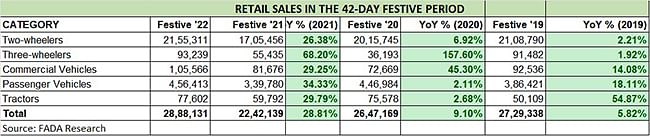

The retail sales data, for five vehicle segments, in the 42-day festive period in 2022 (from September 26 through to November 6) reveals that it is the best in the past four years.

At 28,88,131 units, the YoY growth is 29% with all five categories recording strong double-digit growth. Three-wheelers with 93,239 units recorded 68% growth while two-wheelers (21,55,311 units) are up 26% YoY. The commercial vehicle segment, so critical for the economy, is back in action with 105,566 units, up 29%, while tractors with 77,602 units is up 30 percent. The passenger vehicle sector, which has been firing on all cylinders and riding the wave of demand for SUVs, recorded retails of 456,413 units, up 34 percent.

Dealerships saw double the regular footfalls in the festive month. According to Singhania, “Sentiments have also started improving at the rural level but the same needs to sustain for at least next 3-4 months. Apart from this, new launches and good customer schemes also played a pivotal role in helping revival in demand.”

Near-term outlook: Cautiously optimistic

With festive October 2022 over and out, industry and retails typically witness softening of demand compared to the previous month. FADA remains cautiously optimistic about its near-term growth outlook. Singhania says, “While farmers will start receiving their crop realisations, the overall sentiment continues to show some headwinds especially in the two-wheeler rural segment. For auto retails to show strength, the two-wheeler segment will have to grow for at least 3-4 months over pre-Covid months to come out of the woods.”

“The CV segment is anticipated to see continued demand due to rising infra projects and government spending. While the PV segment continues to outperform, demand in entry level segment continues to show some softness.”

Singhania points out that “most of the OEMs will now start migrating towards manufacturing OBD-2 norm vehicles. This will definitely see a steep price increase across all categories of vehicles as and when they hit the market. Also, with year-end coming close, many customers wait for vehicles manufactured in the new year.”

RELATED ARTICLES

Maruti Brezza Crosses 1.5 Million Sales Ahead of New Model Launch Today

Ajit Dalvi

24 Jul 2026

Ajit Dalvi

24 Jul 2026

Maruti Suzuki’s game-changing Brezza, which spawned the compact SUV segment a decade ago and is the category’s best-sell...

Electric Car and SUV Sales Jump 79% in H1, Set to Cross 300,000 Units in CY2026

Ajit Dalvi

09 Jul 2026

Led by Tata Motors, Mahindra and JSW MG Motor, demand for electric passenger vehicles soared to 148,023 units in the fir...

Electric 2W Sales Race Past a Million Units in First 6 Months and 6 Days of CY2026

Ajit Dalvi

07 Jul 2026

Between January 1 and July 6, electric 2W OEMs have sold 10,05,279 scooters and motorcycles, which is 75% of CY2025’s re...