Follow us

Follow us

India Auto Inc drives towards strong FY2023, Q1 wholesales soar 55 percent

All vehicle segments across categories are in the black, with SUVs powering the passenger vehicle segment and M&HCVs finally seeing strong demand come their way.

14 Jul 2022

14 Jul 2022

8784 Views

Share -

8784 Views

Share -

There is a growing feel-good mood and optimism among automakers in India. June 2022 wholesales for India Auto Inc at 1,611,300 units are a strong 24% year-on-year increase (June 2021: 1,301,602) with all vehicle segments in the black. The first quarter (April-June 2022) FY2023 numbers better that growth.

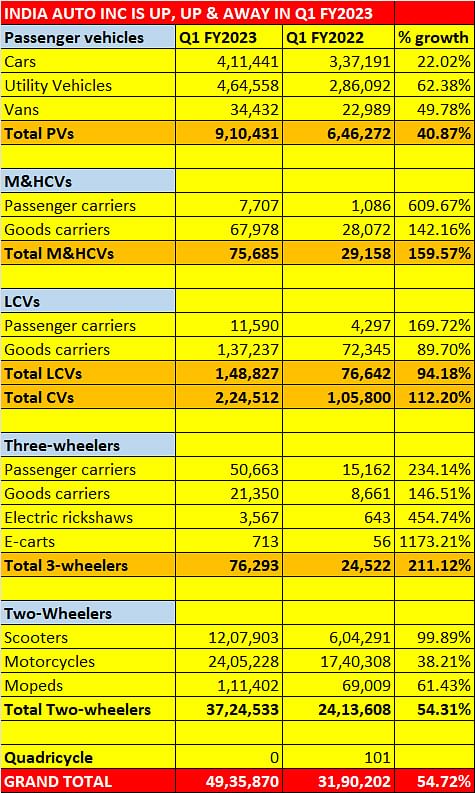

With overall wholesales of 4,935,870 units, India Auto Inc registered a strong 54.72 percent year-on-year (YoY) uptick in the April-June period, over Q1 FY2022's cumulative 3,190,202 units.

The strong demand revival iin Q1 augurs well for a robust FY2023. All vehicle segments hAve registered marked YoY growth with SUVs particularly holding the passenger vehicle segment strong and M&HCVs, considered the barometer of the economy, being back in action.

The passenger vehicle (PV) segment recorded volumes of 910,431 units, registering a 41 percent YoY growth (Q1 FY22: 646,272). SUVs continue to lead the charge for PVs with a total of 464,558 units getting despatched by OEMs to dealers, registering substantial 63 percent growth (Q1 FY22: 286,092). UVs in Q1 account for 51% of total PV sales, which means one out of two cars sold in India is a utility vehicle, a trend which first kicked in FY2022.

For Hyundai Motor India, which has an order backlog of 130,000 units, the Creta and Venue SUVs command the highest share. As per company dealers, wait time for the Creta ranges between six to eight months, depending upon model, variant and city. "Thankfully with improvement in the semiconductor supplies, we should be able to produce more cars in the coming months," said Tarun Garg, director, Sales, Marketing and Service, HMI.

Maruti Suzuki India's (MSIL's) executive director for Marketing and Sales Shashank Srivastava is also confident about the PV segment being poised for strong uptick in the ongoing fiscal, given the successive growth achieved in the last two quarters.

"The industry recorded volumes of over 910,000 units in Q1 and Q4 FY22 was at 921,000 units. We have seen two consecutive quarters breaching the 900,000-unit mark for the first time in the history of the Indian automobile industry. This clearly indicates that the demand parameters are stable."

However, both Garg and Srivastava have raised red flags, with the list-topping concern being the semiconductor supply, "which is still not back to 100 percent", as per the MSIL top executive. Fears of the economy being impacted by inflation as well as that of issuing further price hikes due to rise in commodity prices, are the other major concerns worrying the industry leaders in the PV segment.

High fuel prices across all fuel types don't send a positive signal either, while the possibility of Covid wreaking havoc in another resurgent wave, with examples seen in China, are worrisome too, but the silver lining is that the "chances of disruption in India are much lower", said Srivastava.

"There are geopolitical challenges too, and interest rates are high. But, we are entering the festive season, and I think the PV segment demand should hold up," Garg added.

Two-wheeler demand gradually picking up

The two-wheeler segment is finally seeing some action coming its way. The segment has registered 54.31 percent YoY growth in Q1 with cumulative volumes of 3,724,533 units, albeit on a low year-ago base of 2,413,608 units in Q1 FY2022. While volumes of scooters doubled from 604,291 to 1,207,903 units in the corresponding quarter, motorcycles too reported a noticeable 38.21 percent growth with Q1 volumes closing at 2,405,228 units (1,740,308).

High fuel prices, high prices of petrol-powered BS VI two-wheelers, as well as inflationary pressures continue to be the top concerns for the segment, despite registering an uptick, especially with a resumption in schools, colleges and offices after a hiatus of possibly the longest time.

CVs, three-wheelers see much-needed traction

Within the 94.18 percent YoY growth registered by the commercial vehicle (CV) segment that clocked 224,512 units in Q1 FY2023 (Q1 FY2022: 105,800), M&HCVs drove in the fast lane and clocked sales of 75,685 units to register a significant 160 percent growth (29,158). A marked increase in infrastructure projects with the government aggressively constructing new roads, the segment was the star performer for the industry.

The three-wheeler segment saw sales growing more than three times from 24,522 units in Q1 FY2022 to 76,293 units in Q1 FY23. While passenger carriers and goods carriers witnessed smart upticks, it was the e-three-wheeler category that saw volumes growing six times from a mere 643 units last year to 3,567 units in the first quarter of the ongoing financial year.

Growth outlook: better days and quarters beckon

While the demand certainly seems to have bounced back and is strong, there are still some areas that concern the industry, which is closely monitoring these macro parameters. The rising fears of inflation, driven by the prolonged war between Ukraine and Russia that has sent the global supply chain into a disorder, as well as the constant threat of Covid resurgence are just some of the watchful factors. However, FY2023 might just be the year that the Indian automobile industry has been longing for in the last four years.

RELATED ARTICLES

TVS Sells 300,000 E-Scooters in Just 7 Months, Races Towards 550,000 in CY2026

Ajit Dalvi

03 Aug 2026

Ajit Dalvi

03 Aug 2026

TVS Motor Co is the fastest e-2W OEM to achieve 300,000 retail sales in a single year, beating Ola which took 8 months f...

Hero Vida Sells 100,000 E-scooters in 5 Months, Crosses 300,000 Milestone

Ajit Dalvi

03 Aug 2026

Hero MotoCorp’s Vida electric 2W brand, which logged its highest monthly sales in July, becomes the latest Indian OEM t...

TVS Sells Record 52,000 E-Scooters in July, E-2W Demand Jumps 77% to 192,000 Units

Ajit Dalvi

01 Aug 2026

Customer deliveries of electric 2Ws crossed 190,000 units for the second month in a row in July. Market leader TVS Motor...