Follow us

Follow us

India's Passenger Vehicle Retail Hits Record High in February 2026

Passenger vehicle sales rose 26% year-on-year to nearly 3.95 lakh units, with rural markets outpacing urban demand and inventory levels continuing to improve toward recommended benchmarks.

720 Views

720 Views

Passenger vehicle (PV) retail in India reached 3,94,768 units in February 2026, marking the highest-ever February sales volume for the segment, according to data released by the Federation of Automobile Dealers Associations (FADA) on March 5, 2026. The result surpassed the previous February record set in 2024 and came despite February being a shorter month in terms of trading days.

The year-on-year growth of 26.12% was broad-based across both urban and rural geographies, reflecting sustained consumer demand following policy changes earlier in the year. On a month-on-month basis, retail declined 23.12% from January 2026's figure of 5,13,475 units. FADA noted this sequential dip is consistent with typical seasonal patterns, as January tends to see elevated purchases ahead of potential price revisions at the start of a new calendar year.

Rural Demand Leads Growth

A notable feature of February's performance was the divergence between rural and urban growth rates. Rural markets recorded a year-on-year increase of 34.21%, significantly outpacing urban markets, which grew 21.12% over the same period. This marks a continuation of a trend seen over recent months, where rural India has been a stronger contributor to overall PV demand than urban centres.

FADA noted that the strength in rural markets is translating into renewed interest in the small car segment, a category that had been under pressure for much of the past two years as consumer preference shifted toward SUVs and utility vehicles. The rural recovery appears to be broadening the demand base, even as larger vehicles continue to drive volumes at the aggregate level. Improved agricultural incomes following a good crop season, along with better affordability stemming from GST rationalisation, were cited as key factors behind rural demand.

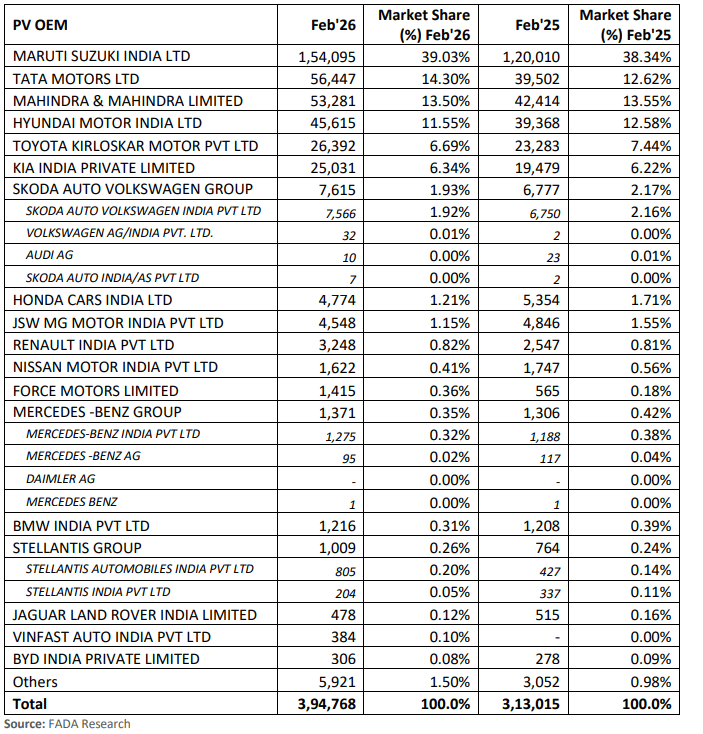

OEM Market Share

Maruti Suzuki India retained its position as the dominant player in the PV segment, retailing 1,54,095 units in February 2026 and holding a 39.03% market share, up slightly from 38.34% in February 2025. The company's performance was supported by its wide product portfolio across multiple price points, spanning entry-level hatchbacks to SUVs, giving it exposure to both the urban and rural recovery.

Tata Motors ranked second with 56,447 units and a market share of 14.30%, a gain from 12.62% in the same month last year. Mahindra & Mahindra came in third with 53,281 units and a 13.50% share, broadly stable year-on-year. Hyundai Motor India held fourth position with 45,615 units and an 11.55% share, while Toyota Kirloskar Motor and Kia India rounded out the top six with shares of 6.69% and 6.34% respectively.

Among other manufacturers, Force Motors saw one of the more notable year-on-year gains in absolute terms, moving from 565 units in February 2025 to 1,415 units in February 2026. VinFast Auto India, which had no recorded retail in February 2025, registered 384 units in February 2026 as it continues to build its presence in the Indian market.

Fuel Mix Trends

Fuel Mix Trends

Petrol and ethanol variants remained the most common fuel type among PV buyers, accounting for 46.08% of retail in February 2026, a decline from 48.30% a year earlier. CNG and LPG vehicles continued to gain ground, rising to 23.45% from 20.38% in February 2025, reflecting consumer interest in lower running costs amid elevated fuel prices.

Diesel's share stood at 18.80%, down from 19.65% a year ago, continuing a gradual decline in its share of the PV mix. Hybrid vehicles accounted for 8.19% of sales, broadly in line with February 2025's 8.64%, while electric vehicles made up 3.48% of PV retail, a modest increase from 3.04% in the same period last year.

Inventory Levels Improve

PV dealer inventory declined by approximately five days compared to the previous month, with stock levels now standing at 27 to 29 days. FADA's recommended benchmark for healthy retail operations is 21 days of inventory. While dealers have not yet reached that target, the consistent reduction over recent months has been noted positively by FADA, which acknowledged PV original equipment manufacturers for improving supply discipline and aligning wholesale dispatches more closely with actual retail offtake.

Elevated inventory had been a concern for FADA through much of FY25, when dealer stock levels had stretched significantly beyond recommended levels, creating financial strain for dealerships. The current trajectory suggests that the sector is moving toward a more balanced supply position.

Demand Drivers and Outlook

FADA attributed February's strong performance to several converging factors. The GST rationalisation announced earlier in FY26, commonly referred to as GST 2.0, improved affordability and boosted consumer confidence across vehicle segments. The ongoing marriage season added incremental demand, while a pipeline of new model launches sustained showroom footfall and enquiries.

Dealers also pointed to customers advancing purchases ahead of anticipated price revisions by manufacturers, a pattern that typically plays out toward the end of the financial year.

Looking ahead to March 2026, the outlook for PV retail remains positive. Year-end depreciation benefits are expected to drive purchases among corporate and fleet buyers, while festival demand tied to Navratri, Gudi Padwa, Ugadi, and Eid is likely to support footfall at dealerships. New product excitement and relatively lean dealer stock levels may further encourage buying decisions.

For the April to May 2026 period, however, FADA's dealer survey signals more measured expectations. The post-festive seasonal lull, combined with summer months that traditionally see softer consumer demand, may lead to a normalisation in sales volumes after what has been a strong run through the first quarter of calendar year 2026. Across FADA's broader survey, 67.35% of dealers expect growth over the March to May period, down from 79.70% who had projected growth in the previous survey covering February to April.

Overall, the industry appears to be transitioning from a phase of sharp post-GST rebound growth to one of more steady, calibrated expansion, with the PV segment well positioned to maintain its momentum through the remainder of the financial year.

RELATED ARTICLES

Aston Martin Cuts Price Across India Line-Up by up to Rs 4 Crore Following India-UK FTA

Autocar Professional Bureau

Autocar Professional Bureau

05 Aug 2026

05 Aug 2026

The British luxury carmaker has revised prices across its entire India portfolio, becoming the latest brand to pass on i...

Cummins India Q1 Revenue Rises 18%, Profit at ₹543 Crore

Arunima Pal

05 Aug 2026

Arunima Pal

05 Aug 2026

Strong domestic demand drove revenue growth, while higher commodity costs and inflationary pressures weighed on margins....

ASK Automotive Q1 Profit Rises 29% to ₹85 Crore, Rrevenue up 52%

Arunima Pal

05 Aug 2026

Broad-based growth across braking systems, aluminium components and cables helped ASK Automotive post a strong first qua...