Follow us

Follow us

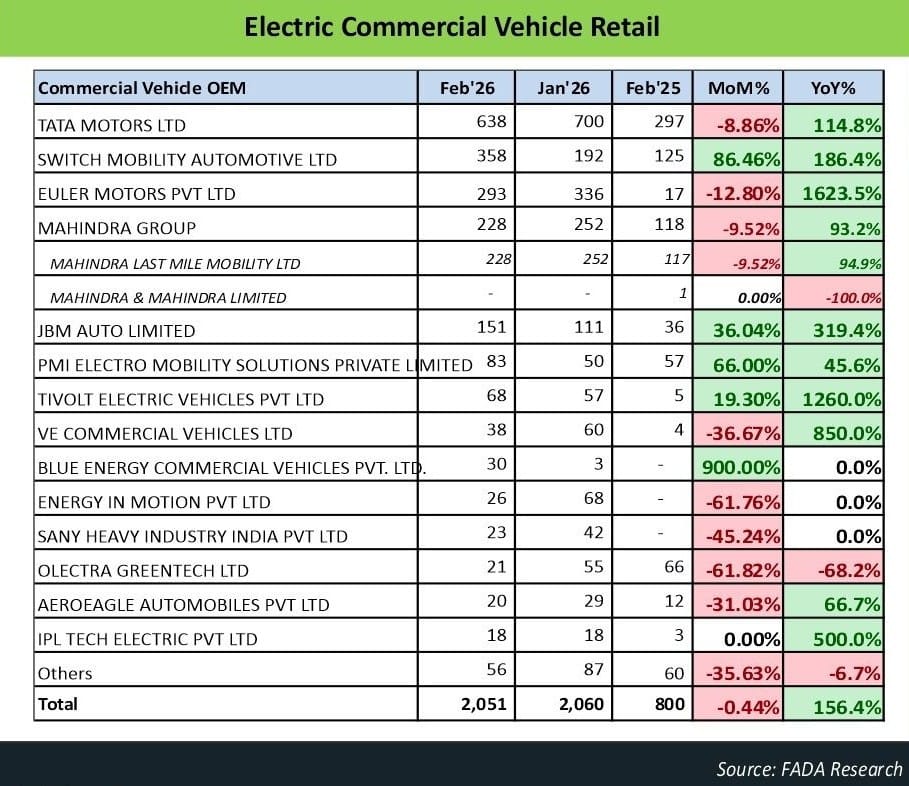

India's Electric Commercial Vehicle Retail Holds Steady in February 2026

Total registrations dipped marginally month-on-month to 2,051 units but more than doubled year-on-year, as market share shifts among top OEMs.

958 Views

958 Views

Electric commercial vehicle (ECV) retail in India stood at 2,051 units in February 2026, a marginal decline of 0.44% from 2,060 units recorded in January 2026, according to data released by the Federation of Automobile Dealers Associations (FADA). Despite the month-on-month softness, the segment posted year-on-year growth of 156.4% from 800 units in February 2025, underscoring the pace at which electric vehicles are penetrating India's commercial vehicle market.

The data covers a range of original equipment manufacturers (OEMs) operating across electric buses, electric trucks, and last-mile delivery vehicles — segments that have emerged as early adopters of electrification within India's broader automotive ecosystem.

Market Leaders

Tata Motors Ltd retained its position as the top-selling ECV manufacturer with 638 units in February 2026, though sales declined 8.86% from 700 units in January. On a year-on-year basis, Tata Motors reported growth of 114.8% from 297 units in February 2025. The company's consistent leadership reflects its established presence across electric bus and last-mile delivery segments, backed by participation in government-tendered fleet contracts.

Tata Motors Ltd retained its position as the top-selling ECV manufacturer with 638 units in February 2026, though sales declined 8.86% from 700 units in January. On a year-on-year basis, Tata Motors reported growth of 114.8% from 297 units in February 2025. The company's consistent leadership reflects its established presence across electric bus and last-mile delivery segments, backed by participation in government-tendered fleet contracts.

Switch Mobility Automotive Ltd emerged as the month's notable performer among larger players, with retail figures rising 86.46% to 358 units from 192 units in January 2026. Year-on-year, the company posted growth of 186.4% from a base of 125 units. Switch Mobility, the electric vehicle subsidiary of the Hinduja Group's Ashok Leyland, has been scaling operations in the electric bus category.

Euler Motors Pvt Ltd ranked third with 293 units, a month-on-month decline of 12.80% from 336 units in January. However, the company's year-on-year figure stood at a growth of 1,623.5%, against a low base of 17 units in February 2025, reflecting the pace of its ramp-up in the electric cargo three-wheeler segment over the past year.

Mahindra Group, consolidating figures from its subsidiary Mahindra Last Mile Mobility Ltd, sold 228 units in February 2026 — a 9.52% decline from 252 units in January. Year-on-year, the group recorded growth of 93.2% from 118 units. Mahindra Last Mile Mobility, which focuses on electric three-wheelers for last-mile delivery, accounted for the entirety of the group's sales, while the parent entity Mahindra & Mahindra Limited — which had reported one unit in February 2025 — recorded no sales in the current period.

Mid-Tier and Emerging Players

JBM Auto Limited, primarily a manufacturer of electric buses, recorded 151 units in February 2026, a 36.04% increase from 111 units in January and a year-on-year rise of 319.4% from 36 units. PMI Electro Mobility Solutions Private Limited posted 83 units, up 66% month-on-month from 50 units, with a year-on-year increase of 45.6%.

Tivolt Electric Vehicles Pvt Ltd sold 68 units, a 19.30% month-on-month gain, while recording a year-on-year growth of 1,260% from a base of five units in February 2025. VE Commercial Vehicles Ltd, a joint venture between the Volvo Group and Eicher Motors, reported 38 units — a month-on-month decline of 36.67%, though the company's year-on-year figure showed a growth of 850% from four units a year ago.

Blue Energy Commercial Vehicles Pvt Ltd posted 30 units in February 2026, compared to three units in January — a month-on-month increase of 900%. The company had no recorded sales in February 2025, resulting in a year-on-year growth figure of 0% by convention. Energy in Motion Pvt Ltd and Sany Heavy Industry India Pvt Ltd, both of which had no sales in February 2025, reported 26 and 23 units respectively in February 2026, each reflecting month-on-month declines of 61.76% and 45.24%.

Declines and Laggards

Olectra Greentech Ltd, one of the established names in the electric bus segment, saw retail figures fall to 21 units in February 2026 from 55 units in January — a decline of 61.82% — and a year-on-year drop of 68.2% from 66 units. Aeroeagle Automobiles Pvt Ltd sold 20 units, down 31.03% month-on-month, while IPL Tech Electric Pvt Ltd held steady at 18 units, flat from January, recording year-on-year growth of 500% from three units. The "Others" category, aggregating smaller OEMs, contributed 56 units, down 35.63% from 87 units in January and 6.7% lower year-on-year.

Market Concentration and Competitive Dynamics

The top four OEMs — Tata Motors, Switch Mobility, Euler Motors, and Mahindra Group — accounted for approximately 72% of total February 2026 retail volumes at 1,517 units. This concentration has narrowed somewhat compared to the same period last year, as mid-tier and newer entrants increase their share. The data also points to volatility at the lower end of the market, where month-on-month swings of 60% or more are common, reflecting the lumpy nature of fleet orders and the early-stage dynamics of the segment.

The contrast between year-on-year growth rates is notable. While established players such as Tata Motors and Mahindra Group show growth in the range of 93–115%, newer entrants like Euler Motors, Tivolt, and VE Commercial Vehicles are working off low bases and recording triple- or quadruple-digit percentage increases. As volumes normalise and bases rise, such outsized year-on-year growth figures are likely to moderate.

India's electric commercial vehicle segment has seen an acceleration in adoption over the past two years, driven by a combination of policy support, total cost of ownership advantages, and increasing model availability. The government's PM e-Bus Sewa scheme, under which electric buses are deployed on city routes through long-term contracts, has provided a demand anchor for bus-focused manufacturers. Meanwhile, the last-mile delivery segment has attracted investment from startups and established players alike, supported by the growth of e-commerce logistics and increasing fuel costs that have made electric alternatives more economically viable for fleet operators.

Despite year-on-year growth, the overall volume of approximately 2,000 units per month remains a small fraction of India's total commercial vehicle retail, which typically runs in the range of 80,000 to 90,000 units per month. Electrification of commercial vehicles, while directionally positive, continues to face constraints including charging infrastructure gaps, higher upfront vehicle costs relative to diesel counterparts, and range limitations for long-haul applications.

Industry observers note that the near-term trajectory of the segment will depend on the pace of government procurement under fleet electrification schemes, the availability of financing for fleet operators transitioning from conventional vehicles, and the ability of manufacturers to build out after-sales and service networks at scale.

RELATED ARTICLES

Aston Martin Cuts Price Across India Line-Up by up to Rs 4 Crore Following India-UK FTA

Autocar Professional Bureau

Autocar Professional Bureau

05 Aug 2026

05 Aug 2026

The British luxury carmaker has revised prices across its entire India portfolio, becoming the latest brand to pass on i...

Cummins India Q1 Revenue Rises 18%, Profit at ₹543 Crore

Arunima Pal

05 Aug 2026

Arunima Pal

05 Aug 2026

Strong domestic demand drove revenue growth, while higher commodity costs and inflationary pressures weighed on margins....

ASK Automotive Q1 Profit Rises 29% to ₹85 Crore, Rrevenue up 52%

Arunima Pal

05 Aug 2026

Broad-based growth across braking systems, aluminium components and cables helped ASK Automotive post a strong first qua...