Follow us

Follow us

Electric Three-Wheeler Retail Sales Fall 12% Month-on-Month in February 2026

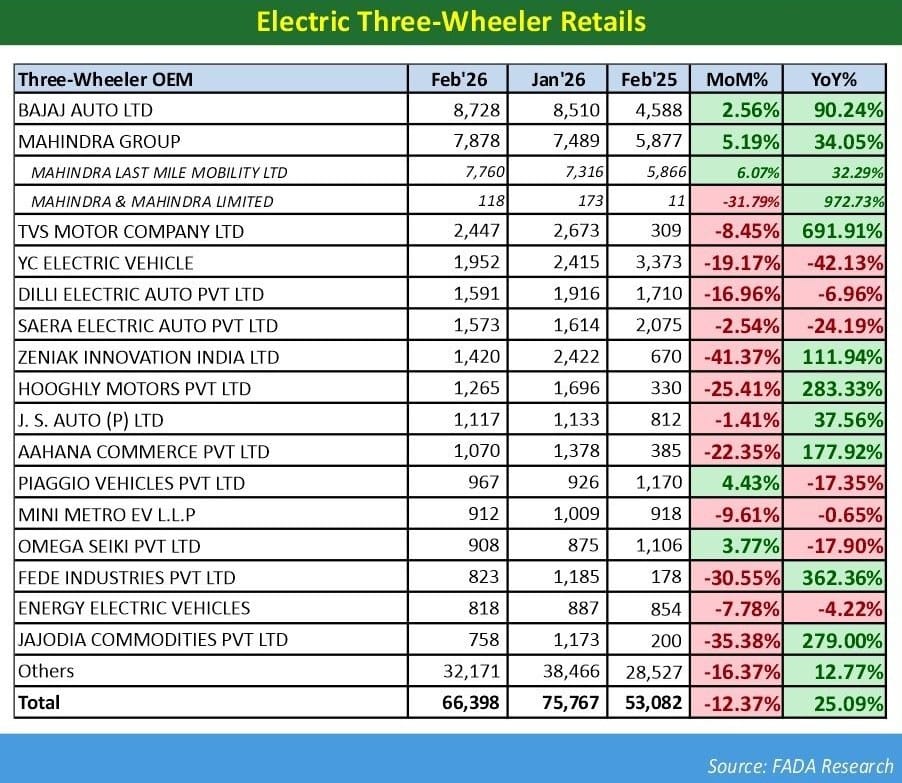

India's electric three-wheeler segment recorded 66,398 units in retail sales last month, down from January's 75,767 units, even as year-on-year growth remained strong at 25%, with market share holding above 56%.

1057 Views

1057 Views

India's electric three-wheeler (E3W) retail sales declined 12.37% in February 2026 compared to January, according to data released by the Federation of Automobile Dealers Associations (FADA). A total of 66,398 units were retailed during the month, against 75,767 units in January 2026. Despite the monthly contraction, the segment posted a 25.09% increase on a year-on-year basis, compared to the 53,082 units sold in February 2025 — underscoring the segment's sustained growth trajectory over the past twelve months.

The E3W segment's share of the overall three-wheeler market stood at 56.7% in February 2026, slightly above the 56.4% recorded in February 2025, though below the 59.6% seen in January 2026. The narrowing of market share from January to February is consistent with seasonal retail patterns seen in prior years. The data was collated as of March 2, 2026, in collaboration with the Ministry of Road Transport and Highways (MoRTH), Government of India, and covers 1,459 out of 1,464 Regional Transport Offices (RTOs). Figures from Telangana (TS) are not included in the dataset.

Market Leaders Hold Ground

Bajaj Auto Ltd retained its position as the top-selling E3W original equipment manufacturer (OEM) with 8,728 units sold in February 2026. This represented a month-on-month (MoM) increase of 2.56% over January's 8,510 units, and a year-on-year (YoY) jump of 90.24% from the 4,588 units it sold in February 2025. Bajaj's consistent performance reflects its established distribution network and strong demand for its electric cargo and passenger three-wheelers across major cities.

Bajaj Auto Ltd retained its position as the top-selling E3W original equipment manufacturer (OEM) with 8,728 units sold in February 2026. This represented a month-on-month (MoM) increase of 2.56% over January's 8,510 units, and a year-on-year (YoY) jump of 90.24% from the 4,588 units it sold in February 2025. Bajaj's consistent performance reflects its established distribution network and strong demand for its electric cargo and passenger three-wheelers across major cities.

Mahindra Group ranked second with 7,878 units, posting a MoM rise of 5.19% and a YoY gain of 34.05% over the 5,877 units sold in February 2025. The group's performance was led by its subsidiary Mahindra Last Mile Mobility Ltd, which accounted for 7,760 units — up 6.07% MoM and 32.29% YoY. Mahindra & Mahindra Limited, the parent entity's direct contribution, stood at 118 units, down 31.79% MoM but recording a significant YoY increase of 972.73% from a low base of just 11 units in February 2025.

TVS Motor Company Ltd secured the third position with 2,447 units in February 2026. While its sales fell 8.45% compared to January's 2,673 units, the company recorded one of the highest YoY growth rates among listed manufacturers at 691.91%, up from 309 units in February 2025. TVS has been scaling up its electric three-wheeler presence over the past year, making it among the fastest-growing players in the segment in volume terms.

Mid-Tier Players Show Mixed Trends

Among mid-tier manufacturers, performance was varied. YC Electric Vehicle, which had been among the top-five sellers in recent months, saw its sales fall to 1,952 units in February — a 19.17% MoM decline from 2,415 units in January — and a sharper 42.13% YoY drop from 3,373 units in February 2025. The decline places YC Electric Vehicle among the few listed OEMs to have contracted on both a monthly and annual basis.

Dilli Electric Auto Pvt Ltd sold 1,591 units, down 16.96% MoM and 6.96% YoY, while Saera Electric Auto Pvt Ltd retailed 1,573 units, recording a 2.54% MoM decline and a 24.19% fall compared to February 2025. Piaggio Vehicles Pvt Ltd, one of the older players in the three-wheeler market, bucked the broader monthly trend with a 4.43% MoM increase to 967 units, though it remained down 17.35% on a YoY basis.

Omega Seiki Pvt Ltd similarly posted a modest MoM gain of 3.77% to 908 units, although it remained 17.90% below its February 2025 levels. Mini Metro EV L.L.P sold 912 units — a 9.61% MoM drop but a near-flat 0.65% YoY decline — making it one of the more stable performers in the segment over the annual period. J.S. Auto (P) Ltd was similarly resilient, dipping just 1.41% MoM to 1,117 units while posting a 37.56% YoY gain.

Notable Monthly Declines

Several manufacturers recorded sharp month-on-month contractions. Zeniak Innovation India Ltd fell 41.37% MoM to 1,420 units, despite posting a 111.94% YoY gain that reflects a strong recovery from the 670 units sold in February 2025. Jajodia Commodities Pvt Ltd recorded the steepest MoM fall among listed players, declining 35.38% to 758 units, though it remained 279% above year-ago levels.

Fede Industries Pvt Ltd dropped 30.55% MoM to 823 units, while Hooghly Motors Pvt Ltd declined 25.41% MoM to 1,265 units. Aahana Commerce Pvt Ltd fell 22.35% MoM to 1,070 units. Energy Electric Vehicles posted a 7.78% MoM decline to 818 units, and also slipped 4.22% on a YoY basis to record one of the smaller absolute contractions in the mid-range.

The sharp monthly declines across several players suggest that January's retail numbers may have been elevated by pre-festival stocking or end-of-quarter push by some dealers, with February seeing a natural correction.

Strong Year-on-Year Performers

Despite the broader monthly pullback, the YoY data points to a segment in structural growth. Fede Industries Pvt Ltd led annual growth among listed OEMs with a 362.36% YoY increase to 823 units from 178 units a year earlier. Hooghly Motors Pvt Ltd rose 283.33% YoY to 1,265 units, while Jajodia Commodities Pvt Ltd climbed 279% YoY to 758 units. Aahana Commerce Pvt Ltd recorded a 177.92% YoY increase to 1,070 units from 385 units in February 2025.

These figures suggest that a number of smaller and emerging manufacturers have significantly expanded their production and distribution capacity over the past year, even if monthly volumes remain modest in absolute terms. The contrast between their YoY growth rates and MoM declines indicates that base effects continue to flatter annual comparisons for newer entrants.

The "Others" category — comprising the many manufacturers outside the top listed OEMs — accounted for 32,171 units in February 2026, down 16.37% MoM from 38,466 units in January, but up 12.77% YoY from 28,527 units in February 2025. This category continues to represent the single largest share of total E3W retail volumes, reflecting the fragmented nature of the market beyond the top-tier players. The size of the Others segment also points to the large number of regional and smaller-scale manufacturers that have entered the electric three-wheeler space in recent years.

The electric three-wheeler segment in India has expanded at a pace faster than most other vehicle categories, driven by demand for last-mile passenger and cargo mobility in urban, peri-urban, and rural markets. The lower cost of ownership relative to internal combustion engine (ICE) three-wheelers — aided by falling battery prices and government incentives — has accelerated fleet electrification among auto-rickshaw operators and goods carriers.

Government policy has played a role in shaping demand. The PM E-DRIVE scheme, along with FAME II subsidies during their operational phase, provided direct purchase incentives for electric three-wheelers. State-level EV policies in markets such as Delhi, Maharashtra, and Uttar Pradesh have further supported adoption through road tax exemptions and registration fee waivers. Several state transport undertakings have also placed bulk orders for electric three-wheelers for intra-city and feeder route operations.

The month-on-month decline in February is not unusual within the context of Indian automotive retail. Sales activity typically moderates in February relative to January, partly due to the shorter calendar duration of the month and inventory normalization at the dealer level following the post-harvest and year-opening demand cycle. The YoY comparison, which strips out these seasonal effects, presents a more consistent picture of the underlying demand trend — and by that measure, the segment continues to grow at a rate well above the broader three-wheeler market.

FADA collects vehicle retail registration data from RTOs nationwide and publishes monthly segment-wise reports in collaboration with MoRTH. The E3W retail data captures units registered at dealerships, as distinct from wholesale dispatches from manufacturers to dealers, making it a more accurate representation of end-consumer demand.

RELATED ARTICLES

Schaeffler India Reports 17.5 Percent Revenue Growth in CYQ2

Autocar Professional Bureau

Autocar Professional Bureau

22 Jul 2026

22 Jul 2026

The company, which operates on a calendar year accounting cycle, reports a 17.5 per cent revenue increase for the April ...

N.A.N. MagneTech to Build ₹1,250 Crore Magnet Facility in Andhra Pradesh

Autocar Professional Bureau

22 Jul 2026

The N.A.N. GreenMet platform secures land in Naidupeta for a rare earth magnet plant aiming to start commercial producti...

Sona Comstar and DENSO Form Joint Ventures for Electric Powertrains

Dev Vadchhedia

22 Jul 2026

Dev Vadchhedia

22 Jul 2026

The Indian auto component manufacturer and the Japanese technology supplier partner to produce electric and hybrid syste...