Follow us

Follow us

Decoding the Hyundai Motor India DRHP

An analysis of IPO documents reveals that the Korean group’s strategy of sweating its assets has created a highly profitable Indian unit.

7995 Views

7995 Views

Hyundai Motor India’s initial public offering is set to be a landmark event for both the Indian equity market as well as the Indian automobile sector. With this IPO, Hyundai Motor India will become the first car manufacturer in India to become public in over two decades. India’s largest carmaker, Maruti Suzuki India, was the last to be listed on bourses in 2003.

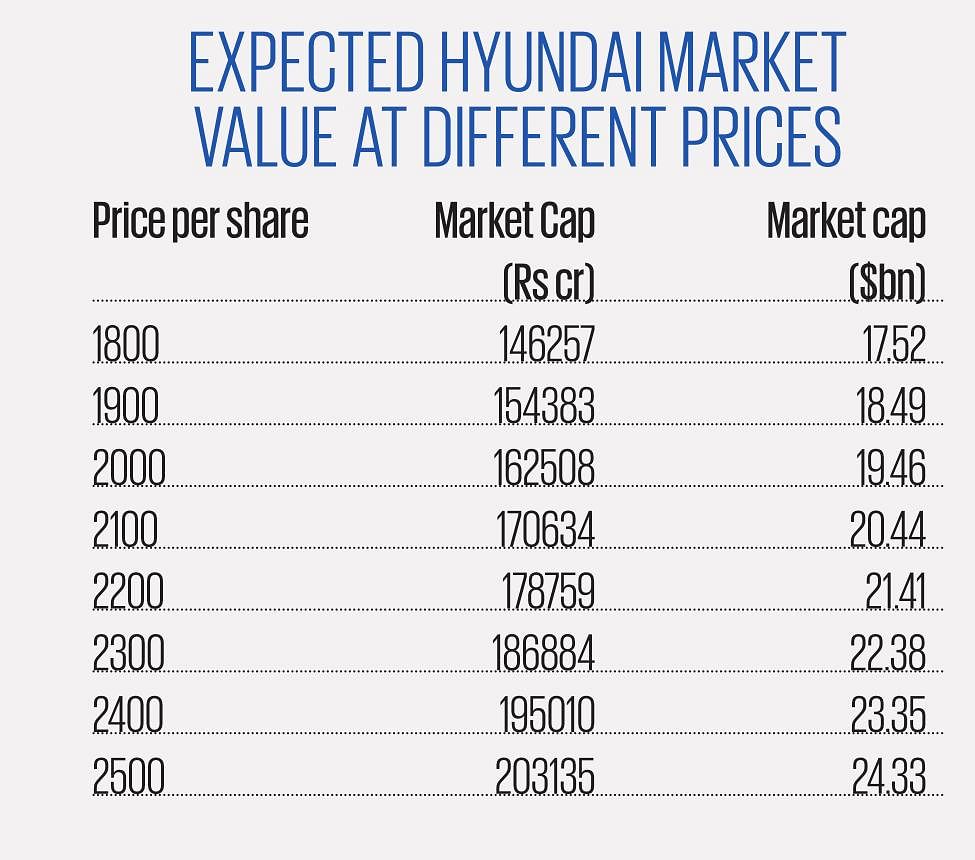

The IPO is expected to be the largest in India. Market participants estimate the Korean parent could raise around Rs 25,000 crore, higher than the Rs 21,000 crore raised by the Life Insurance Corporation in India’s largest IPO in 2022.

The Korean parent could divest up to 17.5% of the Indian unit at an expected valuation of $18 billion to $20 billion. Since there will be no fresh issue of shares in this offering, the money will initially flow to the Korean parent, which is expected to channel it back into the Indian company in the form of equity investments later.

Analysts say the timing of the IPO is perfect, considering the Nifty and the Nifty Auto are trading at all-time highs. This could boost Hyundai Motor Company’s valuation in the home stock market and offset the "Korean discount.”

The Korean discount refers to a tendency for South Korean companies to be valued lower than their global peers on the international stock market, even with similar earnings or book value. This could be attributed to corporate governance concerns and geo-political risks. Analysts often consider South Korea’s stock market undervalued, despite being Asia's fourth largest economy.

Raghunandhan NL from Nuvama Wealth believes Hyundai might have chosen the IPO route for a better valuation. This could also provide valuation support for the global entity, which trades at around $50-55 billion. Hyundai Motor Company trades at low P/E ratios of 4.1-4.6 times, compared to Japanese and US automakers' average P/E ratios of 7.3 and 5.4, respectively.

A potential $18-20 billion valuation for Hyundai India would imply that the value of the Indian unit is about half the value of the company’s operations outside India ($35-37 billion).

According to the company’s DRHP, Hyundai Motor has invested around Rs 29,741 crore in India as of December end in tangible fixed assets and capital work in progress since inception, helping it set up the first and secondlargest manufacturing and supply chain ecosystem within the group outside Korea.

The DRHP sheds light on the company’s operations and infrastructure. According to it, Hyundai Motor India has two integrated manufacturing plants in Sriperumbudur — on the outskirts of Chennai, with a combined annual production capacity of 8,24,000 units. The company has a portfolio of 13 passenger vehicles based on seven platforms, including a range of SUVs and multiple fuel options across petrol, diesel, compressed natural gas (CNG) and electric.

In addition to a stronghold in the domestic market, with a share of around 15%, India serves as an export hub for Hyundai Motor Company’s emerging markets in South Asia, Latin America, Africa, and the Middle East, with the potential to export to other global markets as well.

Hyundai India has been India’s largest exporter of passenger vehicles from the financial year 2005 to the first 11 months of FY24, the company said. Exports account for around 23% of Hyundai India’s annual revenue from operations and total volumes. Verna, Creta, Alcazar, Grand i10 and Venue are among the top export models.

“The company has a track record of manufacturing and selling PVs, which are reliable, feature-rich, innovative, and backed by the latest technology. Key strengths include— (1) strong brand positioning, (2) ability to leverage new technologies and expand into new businesses and (3) endeavor to exceed customer expectations,” Kotak Institutional Equities said in its note to investors.

High Profits

A closer look at the company’s numbers in the DRHP reveals that the company has been highly profitable for the Korean parent.

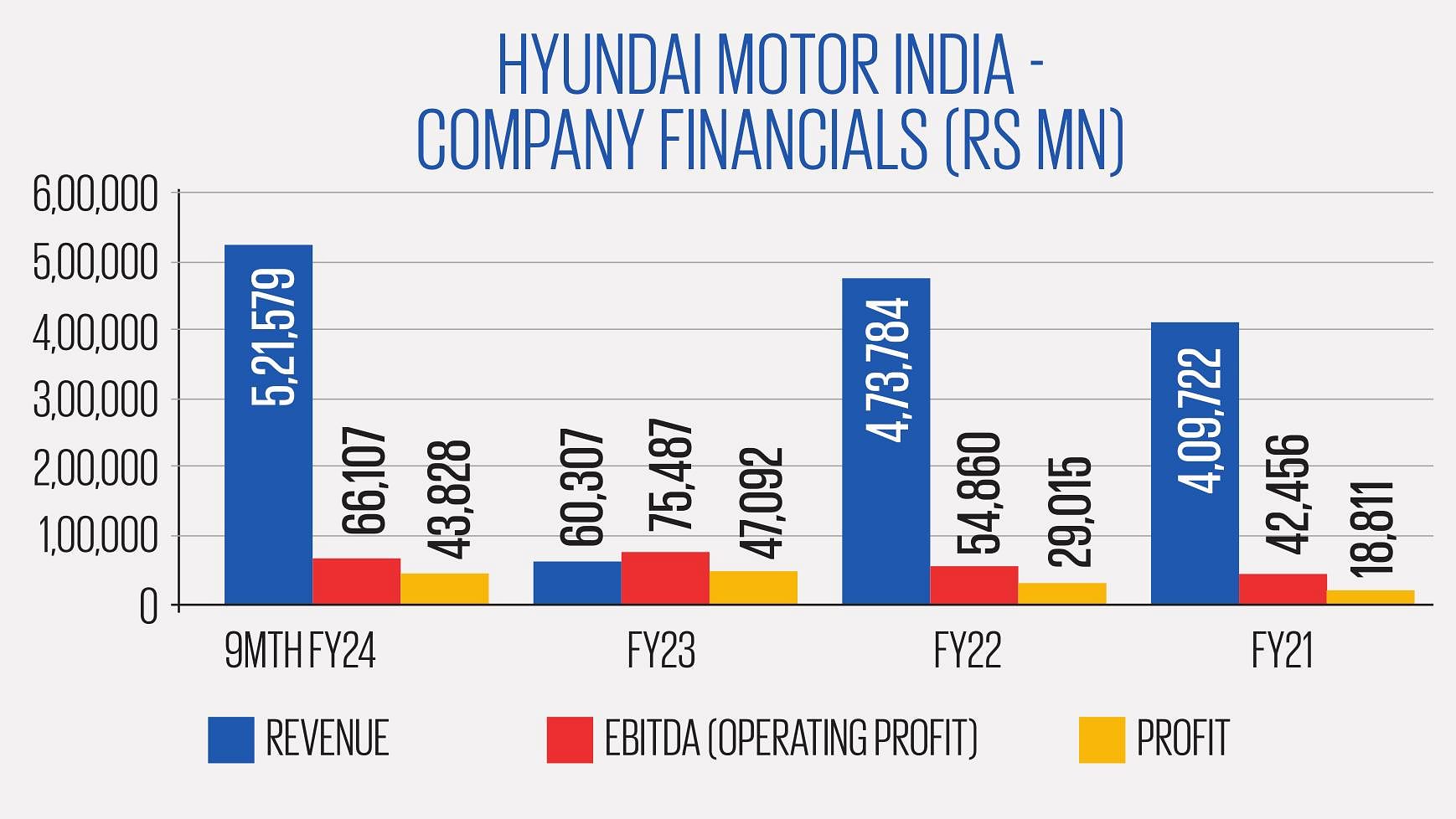

For the financial year 2023, the automaker clocked a net profit of Rs 4,692.01 crore, up 62% year on year. Hyundai India did not disclose its numbers for the full financial year 2024. But going by the net profit of Rs 4,382.87 crore disclosed for the nine months that ended Dec 31, FY24 is likely to have been an even more profitable year for the company.

The company’s revenue from operations for FY23 rose around 27% to Rs 60,307.58 crore, driven by double-digit volume growth. For the first nine months of FY24, revenue from operations was at Rs 52,157.91 crore.

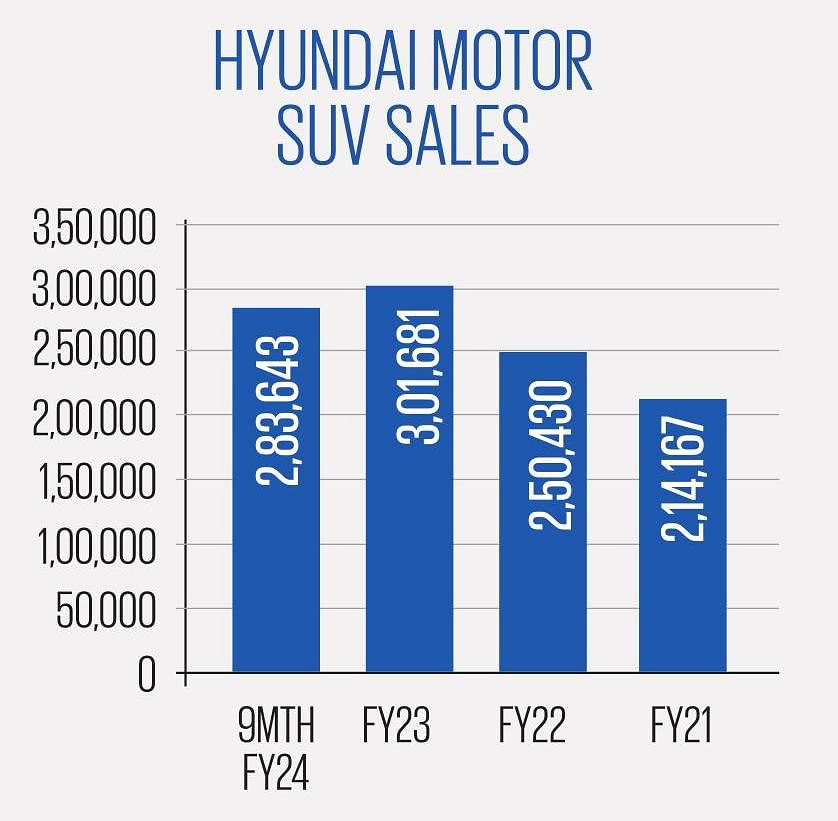

Growth during FY23 was driven by strong demand. Hyundai India sold 720,565 vehicles during the financial year, up around 18% from the year-ago period. The carmaker generates more than half of its domestic volume from SUVs, 53.2% in FY23 and 52% in FY22, which partly explains its high profitability.

The company’s earnings before interest, taxes, depreciation, and amortisation (EBITDA), or operating profit, increased by 38% during FY23 to Rs 7,548.78 crore, boosting the operating profit margin 90 basis points to 12.5%. For the first nine months of FY24, EBITDA came in at Rs 6,610.77 crore.

Royalty payments to Hyundai Motor Company totaled Rs 1,435.82 crore in FY23 and Rs 808.88 core of the nine months of FY24.

In terms of profitability, Hyundai Motor India leads among the country's top three listed passenger car makers. The automaker has consistently achieved a doubledigit operating profit margin over the past few years, surpassing Maruti Suzuki and Tata Motors (passenger vehicle business).

Thanks to its focus on premium cars, a higher share of sports utility vehicles in the sales basket, cost structure, and capacity utilisation, Hyundai India has been a champion in maintaining profitability in the Indian passenger vehicle market.

Hyundai India’s EBITDA margin of 12.7% is higher than Maruti Suzuki’s 11.4% and Tata Motors’ PV business’ margin of 6.1%. Besides, Hyundai India's EBITDA margin has grown consistently from FY21 to FY23 – from 10.4% in FTY21 to 11.6% in FY22 to 12.5% in FY23. For comparison, Maruti Suzuki’s consolidated margins were 7.6% in FY21, 6.5% in FY22 and 11% in FY23. For FY24, the company’s margin was at 13%. Tata Motors’ margin was 5.3% in FY22 and 6.4% in FY23. In FY24, it improved further to 6.5%.

Meanwhile, Mahindra & Mahindra reported a standalone operating margin of 7.8% for FY23 and 10.6% for FY24. However, the company's standalone figures include the automotive (PVs and CVs) and farm equipment businesses.

Part of the reason for the high margins has been the company’s ability to sweat its assets. Hyundai India’s facilities in Chennai have been operating at over 94% capacity since last financial year as the market bounced back from the pandemic. The company also benefited from robust volume growth, and price hikes that offset the impact of inflation in raw material prices and improved margins over the period.

Another significant tailwind has been the improving mix of high-margin products, particularly sports utility vehicles. Hyundai India has generated more than half of its domestic volume from SUVs in the last few years. In the first nine months of FY24, SUVs accounted for 62.4% of the company’s domestic sales.

There has been a significant shift in consumer preference towards SUVs with the launch of compact and mid-size models. Feature-rich SUVs are witnessing more traction with increased spending from the upper middle class and aspirations after the pandemic.

The share of PVs priced above Rs 10 lakh has increased from 32.37% in fiscal 2021 to 48.71% in fiscal 2023 and 49.23% in the nine months ended December 31, 2024, the company noted. In comparison, market leader Maruti Suzuki gets only around 25% of its volumes from SUVs.

This feature was first published in Autocar Professional's July 1, 2024 issue.

RELATED ARTICLES

E20 Contamination Claims Don't Hold up to Testing, Oil Marketers Say

Autocar Professional Bureau

Autocar Professional Bureau

07 Aug 2026

07 Aug 2026

Chloride readings at pumps run 0–3 ppm against alleged several hundred; two outlets briefly suspended.

Apollo Tyres Completes Netherlands Shutdown in Strategic Pivot Toward Indian and Hungarian Plants

Shahkar Abidi

07 Aug 2026

Shahkar Abidi

07 Aug 2026

By shifting TBR production to India and expanding PCR throughput in Hungary, Apollo aims to build a lower-cost manufactu...

Tornel Trouble: How West Asia's War Reached JK Tyre's Mexican Factory Floor

Shahkar Abidi

07 Aug 2026

Supply chain disruption and worker unrest combine to deliver JK Tyre's worst quarter in its Latin American operations.