Follow us

Follow us

FADA study shows Kia, Toyota, Hero, Bajaj and VECV meet expectations in post-Covid support

Survey probed dealers across vehicle segments in receiving financial assistance and business continuity support in a post-Covid scenario.

24 Sep 2020

24 Sep 2020

25637 Views

Share -

25637 Views

Share -

Kia and Toyota emerge as front runners in the passenger vehicle segment, meeting their dealer partner expectations in tackling post-Covid challenges better than peers. Hero, Bajaj and VECV too shine in their respective segments in the, ‘Dealer Support Satisfaction Study’ conducted by the Federation of Automobile Dealers Association (FADA) in conjunction with advisory firm PremonAsia.

The survey set out to understand expectations and satisfaction levels of dealers with respect to the support received from their respective OEMs on different aspects of business operations to mitigate the challenges posed by the Covid-19 pandemic. It covered dealers from all segments of the market including passenger cars and utility vehicles, luxury passenger vehicles, two-wheelers, three-wheelers, and M&HCVs and LCVs.

According to Vinkesh Gulati, president, FADA, “Auto dealers were already facing financial stress due to transition from BS IV to BS VI norms and those with high inventories were the worst hit by Covid-19, which almost broke the backbone as dealerships were reeling under high stress with no sales and fixed operational costs.”

“Various OEMs came forward to support their channel partners in this hour of crisis, but the support received varied across segments and manufacturers. The FADA-PremonAsia survey aims to find out whether the support lent by OEMs was enough in bailing out their first customers,” Gulati added.

The study conducted in an online fashion probed dealer owners and CEOs from across India on six major factors:

- OEM support received on financial matters

- Support regarding customer communications

- Support on dealer manpower matters

- Support on lockdown related matters

- Support on restart of business

- Support on future business evolution

While dealer expectations range from hygiene and delight factors to hygiene expectations including support on online manpower engagement training, redefining manpower productivity norms and providing freedom to dealer owners, support on handling customers in terms of delays in new vehicle delivery as well as information on transition to BS VI norms and support in creation of active dealer council to effectively communicate and manage common issues.

Dealer delight expectations included financial collaboration such as support by negotiating with banks to provide better working capital rates and assistance on expediting collection of receivables, rationalisation of inventory better dealer-OEM coordination and last but not least, support in terms of comprehensive and bespoke support packages emerged as being an ask of absolute delight for most dealer owners.

The segment-wise findings of the study are as follows:

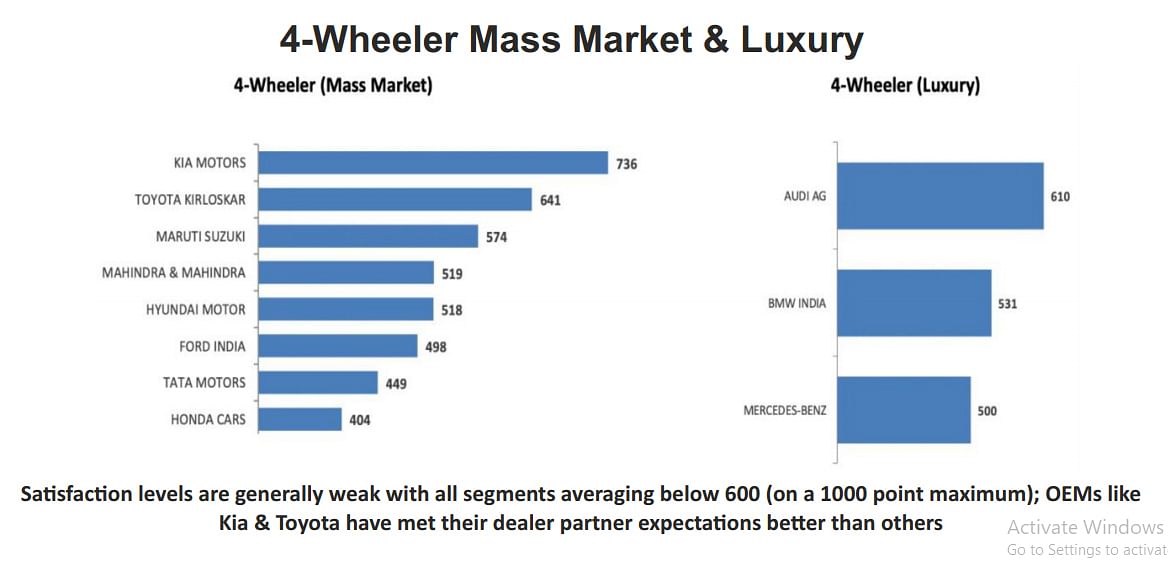

Passenger vehicles: Kia emerged at the top; Toyota a close second

While dealer satisfaction levels were generally weak across the PV segment with most OEMs averaging below 600 (on a 1,000-point scale), OEMs including Kia Motors India and Toyota Kirloskar Motor (TKM) have met their dealer partner expectations better than others.

What worked in favour of Kia was that the OEM was able to record stronger level of satisfaction on areas of communication and dealer manpower-related matters. Senior management of Kia maintained regular and close communication with dealer owners and offered adequate information on communication with customers waiting for their vehicles. Dealer principals were also content with the fact that Kia offered online engagement to motivate and enhance knowledge of sales ands service staff at the dealerships.

On the other hand, TKM too exceled on the fronts of expediting settlement of all claims including warranty, marketing, sales incentives, and payments among others. The carmaker also assisted its dealer partners financially on their vehicle inventory - both at the dealerships and those in transit. Toyota also was sensitive and supportive of dealer-specific business issues and deployed personalised solutions.

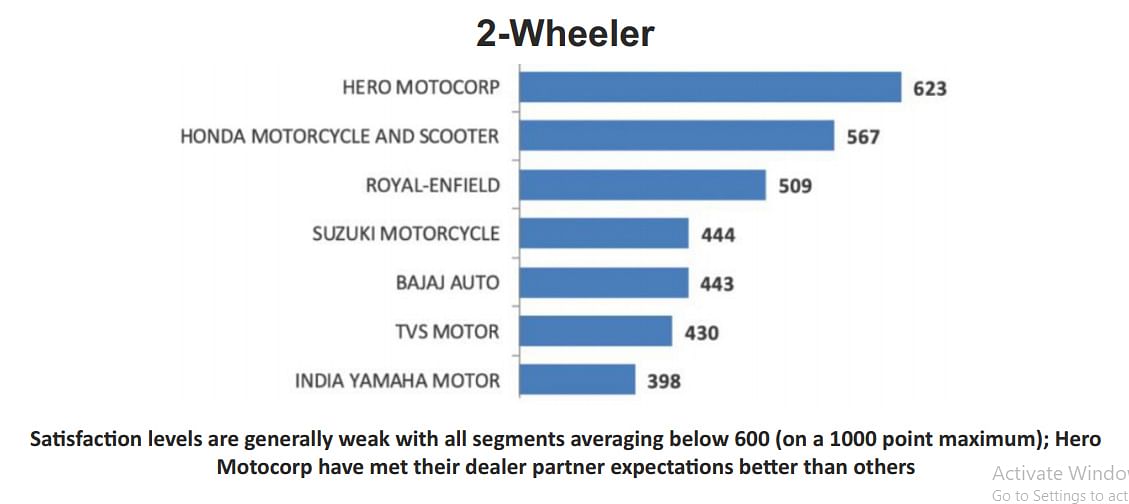

Two-wheelers: Similarly, in the two-wheeler space, while overall satisfaction levels remained below an average of 600, country’s largest two-wheeler maker, Hero MotoCorp was able to meet the dealers’ expectations better than others.

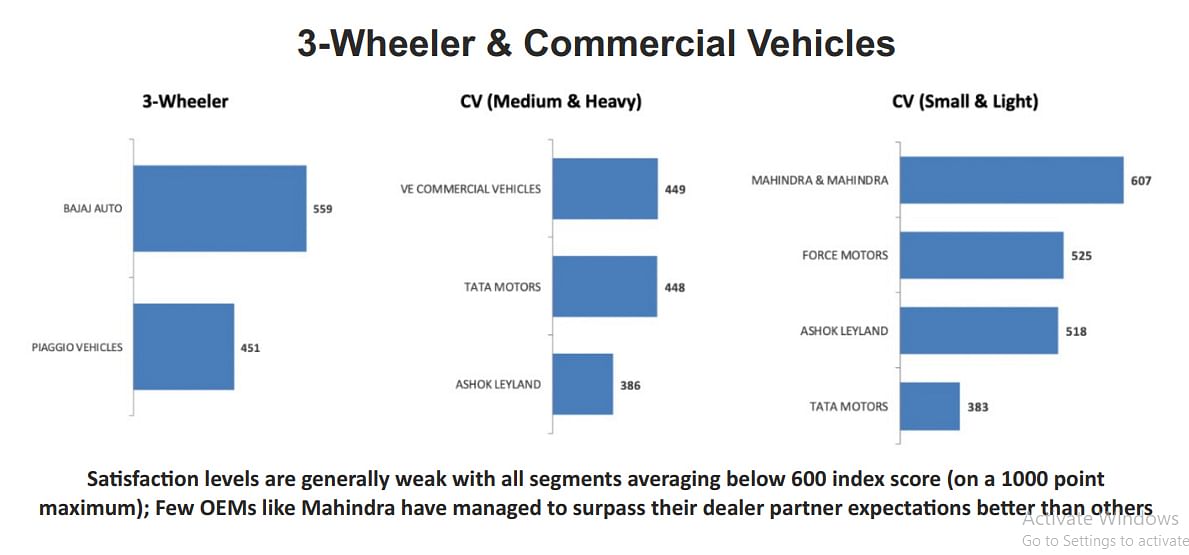

Three-wheelers and CVs: In the three-wheeler segment, it was Bajaj Auto and Piaggio Vehicles that bettered the industry average while VECV and Mahindra & Mahindra topped the charts in M&HCV and LCV segment, respectively.

Future roadmap

Future roadmap

With Covid-19 pandemic taking a toll on profitability and casting shadows even on business sustenance in low-volume, high-cost dealer operations, the report also outlined the way forward for automobile dealers to ensure survival in the tough situation.

While dealers would need to cut costs and exercise greater financial discipline to survive, there is also going to be a big role to be played by data analytics as well as digital marketing and technology in ensuring growth, sustenance and profitability.

With an increased focus on digital and contactless retail, 50 percent of the respondents in the survey believe that the need for physical dealership infrastructure will reduce over time.

RELATED ARTICLES

Cosmo First diversifies into paint protection film and ceramic coatings

Autocar Professional Bureau

17 Jul 2025

Autocar Professional Bureau

17 Jul 2025

The Aurangabad, Maharashtra-based packaging materials supplier is leveraging its competencies in plastic films and speci...

JSW MG Motor India confident of selling 1,000 M9 electric MPVs in first year

Autocar Professional Bureau

11 Jul 2025

The 5.2-metre-long, seven-seater luxury electric MPV, which will be locally assembled at the Halol plant in Gujarat, wil...

Modern Automotives targets 25% CAGR in forged components by FY2031, diversifies into e-3Ws

Autocar Professional Bureau

05 Jul 2025

The Tier-1 component supplier of forged components such as connecting rods, crankshafts, tie-rods, and fork bridges to l...