Follow us

Follow us

Mahindra, Bajaj and TVS power electric 3W sales past 800,000 for the first time in FY2026

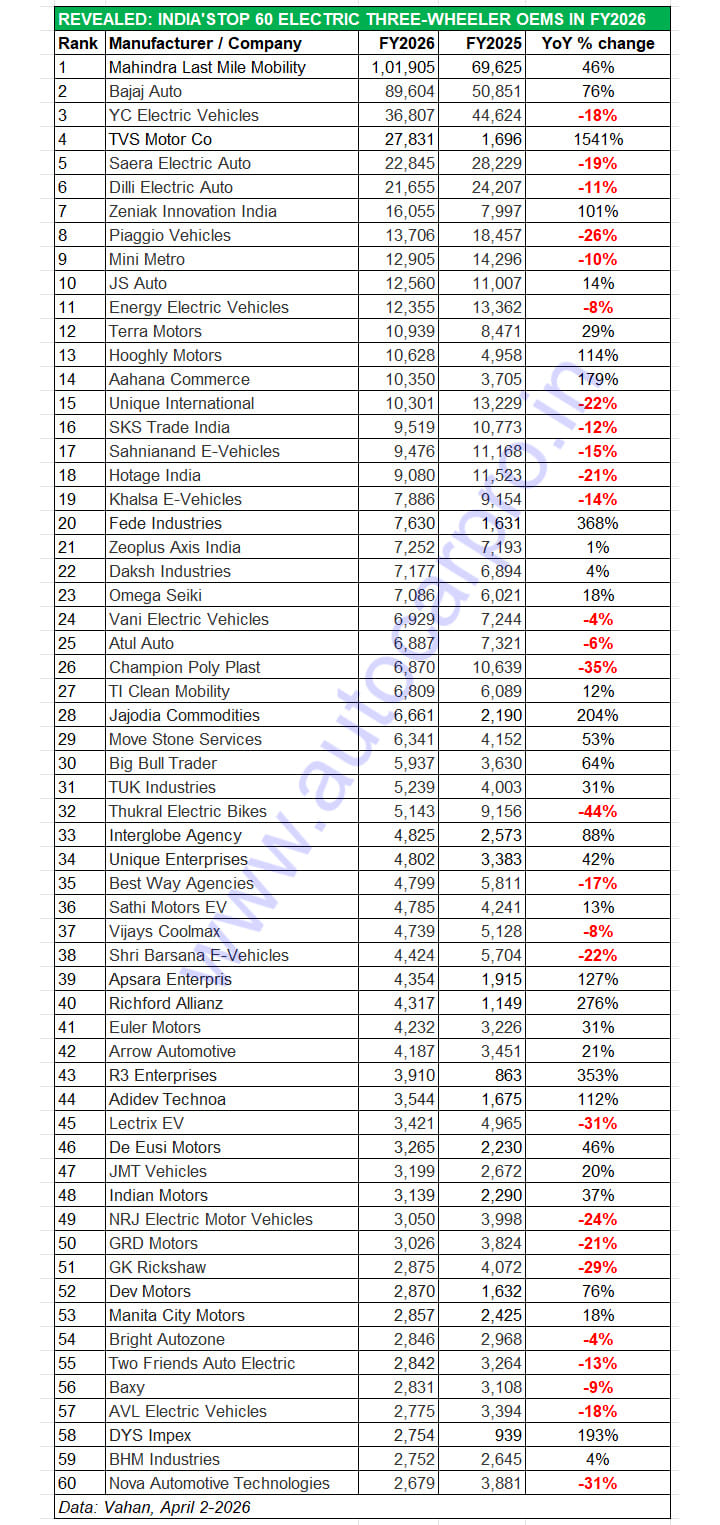

Demand for electric 3-wheelers rose 19% to a record 830,819 units in FY2026. While market leader Mahindra Last Mile Mobility sold 101,905 units, Bajaj Auto and TVS Motor also secured their highest sales as legacy OEMs stamped their authority. We reveal India’s Top 60 e-3W OEMs.

3102 Views

3102 Views

Having missed the 800,000 retail sales milestone by a whisker in CY2025, India’s electric 3-wheeler industry has charged past that big number for the first time in FY2026. As per the e-3W sales registration data on the Vahan portal, 830,819 units were delivered to customers in FY2026, which marks strong 19% YoY growth (FY2025: 698,914 units).

Like the electric 2-wheeler (1.40 million units, up 22%) and passenger vehicle (199,333 units, up 83%) segments, which have registered their highest-ever fiscal year sales, demand for zero-emission passenger and cargo e-3Ws also rose to a new high. As is known, the e-3W segment continues to witness the fastest transition to electric mobility, mainly driven by legacy ICE OEMs which have diversified into zero-emission vehicles. In FY2026, the share of e-3Ws in overall 3W sales rose to 61% compared to 57% in FY2025. And the record 830,819 units gave the segment a 34% share of India EV Inc’s record 2.45 million units, the second highest after the e-2W segment’s 57% share.

Retail sales in FY2026 saw a sharp spike in November (83,663 units, up 32%) and December 2025 (88,276 units, up 49%) with the year-ending month turning out to be the highest monthly sales yet for the e-3W industry. This was because December 31, 2025 was the closure of the subsidy for the L5 e-3W category under the PM E-Drive Scheme as the target (288,000 units) was achieved ahead of time and the incentivization under the scheme closed after December 26. The L5 category includes both passenger and cargo e-3Ws, powered by motors rated above 0.25 kW and with a top speed of over 25kph.

December 2025 (88,276 units, up 49%) saw the segment achieve its highest monthly sales to date. In FY2026, e-3Ws had a 34% share of India EV Inc’s record sales of 2.45 million zero-emission vehicles.

December 2025 (88,276 units, up 49%) saw the segment achieve its highest monthly sales to date. In FY2026, e-3Ws had a 34% share of India EV Inc’s record sales of 2.45 million zero-emission vehicles.

India e-3W Inc’s robust performance was driven by three legacy OEMs – Mahindra & Mahindra, Bajaj Auto and TVS Motor Co – along with a few other companies from amongst the 680-player market. Let’s take a closer look at the top six best-selling e-3W OEMs who accounted for 36% (300,647 units) of the retail sales in FY2026.

No. 1 – MAHINDRA LAST MILE MOBILITY

FY2026: 101,905 units, up 46%. Market share: 12%

FY2025: 69,625 units, up 15%. Market share: 10%

FY2024: 60,619 units. Market share: 9.57%

Mahindra Last Mile Mobility (MLMM), the e-3W arm of the SUV major Mahindra & Mahindra, maintains its leadership with its best-ever retail sales of 101,905 units, up 46% YoY (FY2025: 69,625 units). This stellar performance, which translates into an additional 32,280 units YoY, makes MLMM the first OEM to surpass 100,000 sales in a single fiscal year.

In terms of market share, MLMM has hit a new high of 12% in FY2026, up from the 10% in FY2025 and 9.57% in FY2024. As the first legacy OEM to plug into e-mobility nearly a decade ago, MLMM has the largest e-3W portfolio including the Treo, Treo Plus, Treo Zor, Treo Yaari, Zor Grand, e-Alfa Plus, e-Alfa Cargo and more recently the UDO. As per the company, it commands a strong presence in the L5 category, with a market share of 39.7 percent.

MLMM clocked five-figure monthly sales for the first time in October (11,861 units) and followed it up with 10,783 units in November 2025. In FY2026, sales rose quarter on quarter in Q1 (19,557 units), Q2 (26,887 units) Q3 (30,759 units) but dropped in Q4 (24,702 units) for a total of 101,905 units. This gave MLMM a decisive advantage of 12,301 units over its arch rival Bajaj Auto which it outsold in 10 of the past 12 months.

No. 2 – BAJAJ AUTO

FY2026: 89,604 units, up 76%. Market share: 11%

FY2025: 50,851 units, up 366%. Market share: 7%

FY2024: 10,897 units. Market share: 2%

In less than three years since it diversified into the e-3W market, India’s No. 1 three-wheeler manufacturer and exporter has achieved a strong foothold in this segment of the EV industry. The Pune-based Bajaj Auto’s advance has been rapid as seen in the 89,604 units (up 76% YoY), sold in FY2026 and an increase of 38,753 units compared to FY2025 (50,851 units).

This strong performance in a competitive market scenario sees Bajaj Auto maintain its No. 2 OEM podium position, behind Mahindra. Interestingly, Bajaj sold more e-3Ws than MLMM in January (8,509 units vs 7,491 units) as well as in February 2026 (8,731 units vs 7,882 units). However, March saw Mahindra (9,328 units) go ahead of Bajaj Auto (9,050 unit) by 278 units.

Bajaj Auto posted consistent quarter-on-quarter growth throughout the fiscal: Q1 FY2026 (18,280 units), Q2 (20,708 units), Q3 (24,326 units) and Q4 (26,290 units). The company, which has the GoGo brand of passenger and cargo e-3Ws, forayed into the 40,000-units-per-month volume e-rickshaw passenger and cargo sub-segment with its Riki model in November 2025 and, more recently, expanded its passenger model portfolio with the Wego P9018 claimed to be India’s longest range (296km) e-3W. These strategic moves have provided additional volumes each month and Bajaj Auto’s growth trajectory is reflected in its rising market share: from 2% in FY2024 to 7% in FY2025 and now to 11% in FY2026.

No. 3 – YC ELECTRIC

FY2026: 36,807 units, down 18%. Market share: 4%

FY2025: 44,624 units, down 4%. Market share: 6%

FY2024: 42,749 units. Market share: 7%

The Delhi-based YC Electric Vehicles continues to feel the heat of the much-increased competition in the market, particularly from legacy OEMs. This longstanding player, which has five models – Yatri Super, Yatri Deluxe, and Yatri for passenger transport, and E-Loader and Yatri Cart for cargo operations – sold 36,807 units in FY2026, down 18% YoY (FY2025: 44,624 units). This, resultantly, sees the company’s e-3W market share fall to 4% from 6% in FY2025 and 7% in FY2024.

No. 4 – TVS MOTOR CO

FY2026: 27,831 units, up 1541%. Market share: 3%

FY2025: 1,696 units. Market share: 0.24%

TVS Motor Co, the latest legacy ICE three-wheeler OEM to enter the electric three-wheeler market, has already made a mark for itself. As per Vahan retail statistics, the Chennai-based auto major delivered 27,831 units to its customers in FY2026, up 1541% YoY on a low year-ago base (FY2025: 1,696 units). This gives TVS a market share of 3% from 0.24% a year ago and fourth rank amongst nearly 700 players.

The company has seen a good customer response to its King EV Max passenger and King Kargo HD EV models in a competitive market. It opened FY2026 with 1,207 units in April 2025 and closed the fiscal with 2,885 units in March 2026, with monthly retails crossing the 2,200-unit mark nine times in the past fiscal year.

No. 5 – SAERA AUTO

FY2026: 22,845 units, down 19%. Market share: 3%

FY2025: 28,229 units, down 6%. Market share: 4%

FY2024: 30,127 units. Market share: 5%

Rajasthan-based Saera Electric Auto, which manufactures the nine-model Mayuri brand of electric rickshaws, is ranked fifth on the e-3W ladder-board. The company sold 22,845 units in FY2026, down by 19% YoY (FY2025: 28,229 units). This total is down by 5,384 units on year-ago sales and by 7,282 units in FY2024. Like YC Electric and several other e-rickshaw makers, a sub-segment which is the largest monthly volume provider, Saera Auto too has been impacted by the growing presence of legacy OEMs and has seen its e-3W market share reduce to 3% from 5% in FY2024.

No. 6 – DILLI ELECTRIC AUTO

FY2026: 21,655 units, down 11%. Market share: 3%

FY2025: 24,207 units, down 7.51%. Market share: 3.5%

FY2024: 26,175 units. Market share: 4%

The Haryana-based Dilli Electric Auto sold 21,655 units in FY2026, down 11% YoY. This company manufactures electric rickshaws (CityLife brand), a category which is now under pressure as legacy players like MLMM, Bajaj Auto, TVS and TI Mobility target sales with better-built, safer products. The impact of increasing competition in the volume e-rickshaw market can be seen in Dilli Electric Auto’s reducing market share which at 2.60% in FY2026 is down from the 4% it had two years ago.

MAHINDRA AND BAJAJ TO CONTINUE BATTLE IN FY2027, TVS COULD BE THE NEW NO. 3 OEM

Competition always makes for exciting industry dynamics and FY2027 should see the exciting battle for market leadership continue at the top of the rankings. Mahindra Last Mile Mobility, the market leader for the past four years, will be looking to ensure it stays the market leader in this EV category which continues to witness the fastest and highest transition to e-mobility in India.

Clearly, the battle between MLMM and Bajaj Auto is underway in full earnest. The growing rivalry between these two OEMs has further increased in new product launches in the same month (February 2026) which had both Bajaj Auto and Mahindra Last Mile Mobility launch their latest e-3Ws – Bajaj P9018 and Mahindra UDO – in the passenger transport category.

Meanwhile, TVS Motor Co has in its first full year of sales, moved into the No. 4 position, behind YC Electric. Given its sustained growth compared to YC Electric’s continuing sales decline, it can be surmised that TVS Motor Co could move up one rank to be the new No. 3 e-3W OEM in FY2027.

A close look at the Top 60 e-3W OEMs in FY2026 (see data table below) reveals that 27 of them have seen a YoY sales decline. This is also reflective of the fact that e-3W buyers of passenger transport and cargo models across the individual as well as fleet operator categories are displaying a preference for models from well-established players which offer well-built, safer products as also the ease of ample service facilities across the country.

Will the strong growth witnessed in FY2026 continue in the new fiscal year? Given the sharpened focus on electric mobility, particularly after the Iran oil crisis, as well as the recent move by the government to extend the PM e-Drive Scheme for the e-3W segment (e-rickshaws and e-carts) to March 31, 2028, albeit with reduced incentives, one can be cautiously optimistic. Even a 10% YoY increase on FY2026’s large base will take the segment to beyond 900,000 units in FY2027.

ALSO READ: Record 1.4 million electric 2Ws sold in FY2026, command 57% share of India EV market

Luxury electric car and SUV sales jump 61% to a new high of 5,404 EVs in FY2026

RELATED ARTICLES

Bajaj Auto Races Past 800,000 EV Sales; Chetak on Track for 400,000 Units This Year

Ajit Dalvi

Ajit Dalvi

28 Jun 2026

28 Jun 2026

Bajaj Auto marks new retail milestone for its Chetak e-scooter, which has witnessed remarkable acceleration in recent mo...

IPO-bound Greaves E-Mobility Crosses 300,000 Sales, Registers 58% Growth This Year

Ajit Dalvi

18 Jun 2026

GEM’s new retail sales milestone for its Ampere e-scooters comes on the back of demand for the Nexus, Magnus Neo and G-M...

Hyundai Venue Joins Select Band of Compact SUVs With 800,000 Sales

Ajit Dalvi

09 Jun 2026

Hyundai Motor India’s first-ever compact SUV launched in May 2019 and followed by the second-gen model in November 2025 ...