India Auto Inc is fighting back and how. For an industry, which was hugely impacted by the long-vexing supply chain crisis triggered off by the global decline in supplies of critical semiconductor, the latest first-half FY2023 production statistics are proof that it has more or less put the chip crisis behind it.

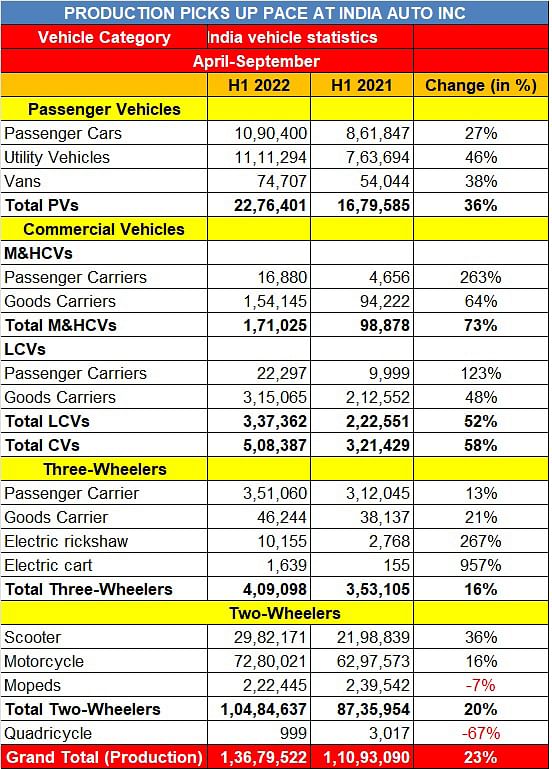

Apex industry body SIAM today released the sales and production data for the April-September 2022 period. The total production volume of 1,36,79,522 units is a strong double-digit 23% year-on-year growth (H1 FY2022: 1,10,93,090 units). Importantly, all four segments – passenger vehicles (36%), commercial vehicles (58%), three-wheelers (16%) and two-wheelers (20%) – have recorded double-digit growth. And, all sub-segments other than mopeds (-7%) and quadricycles (-67%) are in strong positive territory.

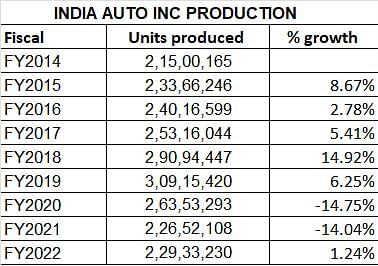

As per SIAM’s production data for the past nine fiscals, India Auto Inc saw a high of 30.91 million units in FY2019 (see data table above). Since then, output has substantially declined due to the slowdown which began in FY2020 and was exacerbated by the Covid-19 pandemic after April 2020. Overall industry output rose in FY2022 after two straight years of decline, with FY2023.

If the momentum of the first-half of FY2023 is maintained over the next six months, industry could potentially reach the 27.50 million-units mark by end-March 2023.

Passenger Vehicles: 22,76,401 units / up 36% YoY

Given the humungous demand in the domestic market, where some PV manufacturers including Maruti Suzuki and Mahindra & Mahindra have a ‘problem’ of plenty with overall pending orders estimated in the region of over 650,000 units, it was only to be expected that this segment would see a good YoY increase in volumes.

The 2.27 million unts produced in H1 FY2023 are a strong 36% YoY increase (H1 FY2022: 16,79,585 units). Given the continued and surging demand for SUVs, it’s no surprise that 49% of total PV output comprises a million UVs – 11,11,294 units (up 46) – while cars at 10,90,400 units (up 27%) are close to the UV contribution at 48%. The balance 3.38% is made up by vans (74,707 units / up 38%).

Given that PV sales in H1 FY2023 have already crossed 1.93 million units and notched robust 40% YoY growth, expect manufacturers to up the ante on the production front. Given the sterling pace of demand and PVs en route to hit their best-ever annual numbers billed to be in excess of 3.6 million units, expect manufacturers to keep the assembly line humming.

Commercial Vehicles: 508,387 units / up 58% YoY

What has brought plenty of smiles to India Auto Inc is the return of demand to the CV industry, whose fortunes are cyclical. After a near-five-year slump, demand is back in the sector, which is known to be the barometer of the economy.

At halfway stage in the fiscal, the CV industry’s production has crossed the half-a-million mark at 508,387 units, up 58% (H1 FY2022: 321,429 units). To cater to strong demand from the mining, steel and cement industries, as well as from passenger-carrying buses for the school and executive transport segments, M&HCV production has jumped 73% YoY to 171,025 units. And heavy goods carriers with 154,145 units account for 90% of that volume.

Light commercial vehicles with 337,362 units account for 66% of total CV production. While a total of 22,297 buses were manufactured (up 123%), huge demand for last-mile transport and the successful hub-and-spoke delivery formula saw OEMs roll out 315,065 small goods carriers including pickups (up 48%).

Given that the economy is on the mend and considerable replacement demand from logistics operators is expected even as OEMs will look to cater to demand from the booming e-commerce sector, CV production in the coming months can be headed only one way – up.

Three-wheelers: 409,098 units / up 16% YoY

Overall production for the three-wheeler segment crossed the 400,000-unit mark in H1 FY2023 with the bulk of the output being 351,060 passenger-carrying models, which account for 86% of the total and a modest 13% YoY increase with 46,244 goods carriers contributing 11.30%. Together these ICE models add up to 397,304 units and 97% of total production, the remaining 11,794 units (2.88% share) belonging to electric rickshaws and goods carriers. But YoY, the share of electric three-wheelers has grown hugely: from 2,923 units (0.82% of total production) to 2.88% of H1 FY2023 output.

Two-wheelers: 1,04,84,637 units / up 20% YoY

When production is of the tune of 10.48 million units or averages nearly 1.75 units a month, there’s ample reason to believe the industry is on to a good thing. Two-wheeler manufacturers rolled out a total of 1,04,84,637 units (up 20% YoY). Motorcycles with 72,80,021 units (up 16%) comprised 69.43% of the total while scooters with 29,82,171 units (36%) accounted for 28.44% of the total. Demand for mopeds is on the decline while is reflected in the seven percent decline in volume to 222,445 units in H1 FY2023.

This segment’s production will grow at a faster pace once demand for entry-level motorcycles from rural India returns. Last month, Manish Raj Singhania, President, FADA said the two-wheeler industry is bearing the brunt of increased prices and expensive loans. “Due to increased input costs, two-wheeler OEMs raised prices by five times in the past year. Apart from this, RBI’s fight with inflation saw rate hikes, which continued to make vehicle loans expensive. While India is showing revival signs, Bharat is yet to perform. Two-wheelers, especially entry level vehicles, are finding extremely few buyers.”

September 2022, which heralded the oncoming of the two-month festive season in India, was a good month for the industry, and saw most OEMs stock their dealerships with popular models. October, which has Diwali in its last week, should accelerate the momentum even more.