Follow us

Follow us

Renault Says It Is Ready to Compete With Chinese Rivals Today

As Chinese manufacturers take a growing share of the European car market on price, speed and technology, Renault's new chief executive says his company is already equipped to respond — and is not waiting for the rest of the industry to catch up.

1185 Views

1185 Views

François Provost is not hedging. While most of Europe's car industry is still mapping a path to competing with Chinese manufacturers, Renault's new chief executive says the race is already underway. "The timeframe is step by step, but it is already starting today," he told analysts at the group's futuREady strategy presentation on March 10. His evidence was a car already in showrooms. "You take the Twingo. This car is below €20,000. Full EV, you have Google inside, great features. I am quite comfortable with this."

The Twingo was built at Renault's Advanced China Development Centre, known internally as ACDC, in 22 months, a record for the group, and is now the standard Provost has set for every programme that follows. The group delivered 32 models in five years under its previous Renaulution plan and sold 2.337 million vehicles in 2025. It holds contract manufacturing agreements with Nissan, Mitsubishi Motors, Volvo Group (through Renault Trucks) and Ford, with a target of producing more than 300,000 vehicles a year for these partners by 2030 across three continents.

François Provost, CEO of Renault Group

François Provost, CEO of Renault Group

It has also spent decades building a downstream revenue model covering used car resale, leasing roll-overs, aftersales, software updates and energy services, a base of commercial relationships that Chinese competitors have not yet had time to establish in Europe. "Downstream, I deeply think that we can bring higher value," Provost said.

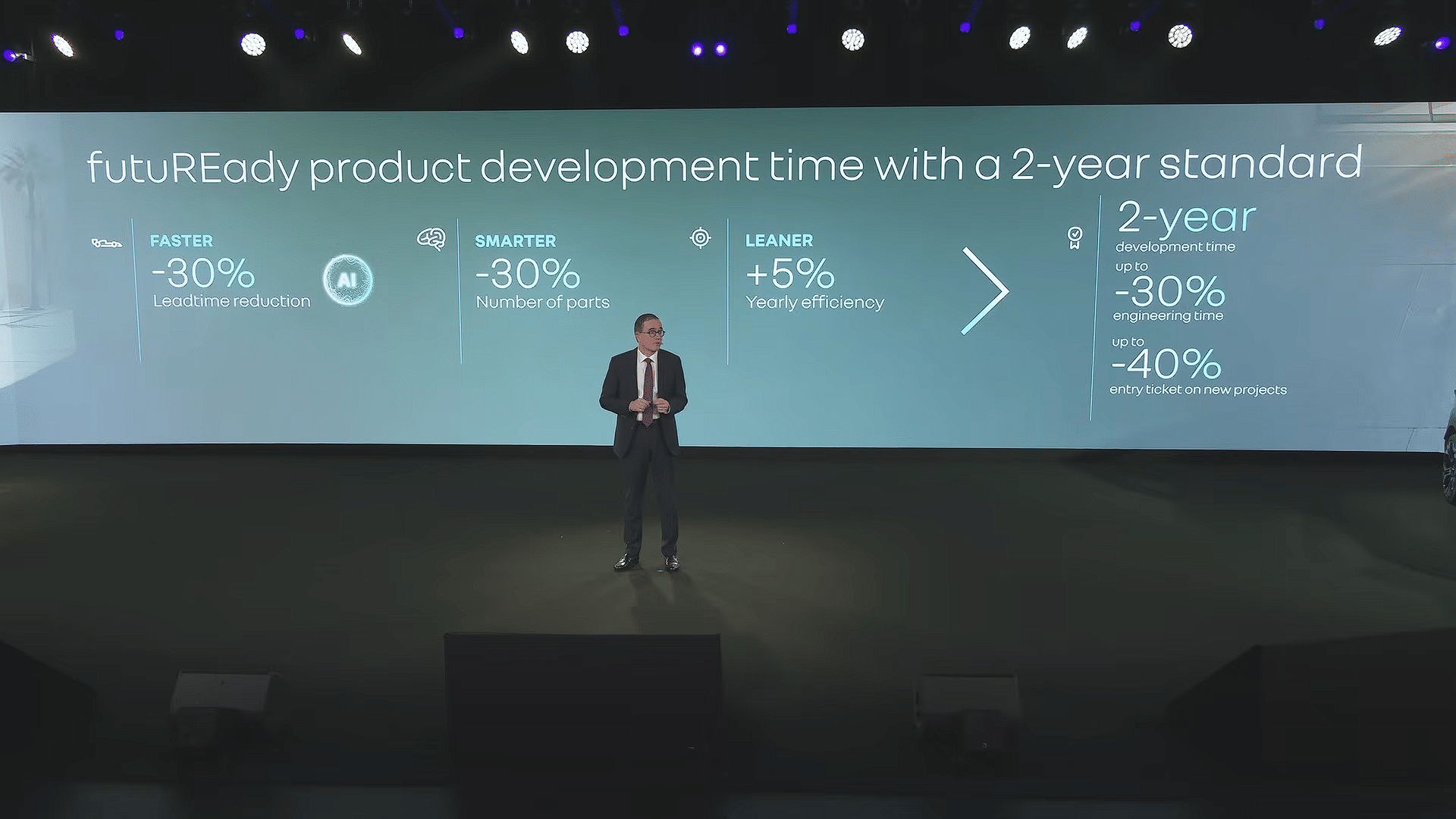

The futuREady plan is Renault's structured response to a competitive shift that has fundamentally altered the European market. It is built around three fronts: closing the technology and cost gap upstream, capitalising on the downstream advantage through the vehicle lifecycle, and anchoring global growth in markets where the company has industrial depth, principally India. The ambition is 36 new model launches by 2030, a shift in the share of sales outside Europe from 38% to 50%, and reductions of up to 40% in entry ticket costs, meaning the development and tooling investment required to bring a new model to market.

The scale of the Chinese challenge puts that ambition in sharp relief. Chinese automakers doubled their overall share of car sales in Europe to 6% in 2025, according to data from automotive consultancy Inovev, up from around 3% in 2020. Their advance has been uneven but striking in key markets. In Britain, Chinese brands accounted for around 11% of all new car sales in 2025. In Spain and Italy, the figure reached around 9%, roughly doubling respective market shares from 2024. Norway, where the market is almost entirely electric, saw Chinese brands take nearly 14%. Companies including BYD, Geely and Chery have expanded quickly, attracting cost-conscious buyers with cars that in some cases cost €10,000 less than equivalent European models. The European Union has imposed tariffs of up to 35% on Chinese-made EVs, but the measures have not halted the advance. Chinese brands have made less headway in car-manufacturing countries such as Germany and France, where analysts cited a share of around 10% of new car sales in the final quarter of 2025, but the trajectory is clear.

That trajectory is also shaping the regulatory environment. On March 4, the European Commission formally proposed the Industrial Accelerator Act, a framework designed to strengthen European manufacturing in strategic sectors, including batteries and electric vehicles. For the automotive sector, the IAA defines criteria for vehicles to qualify as made in the EU for CO₂ emission performance standards and corporate vehicle support schemes. On foreign investment, it requires regulatory approval for large third-country investments in sectors where a single country holds dominant global manufacturing capacity, a provision with direct implications for Chinese automotive investment in Europe.

Renault's exposure to any localisation requirements is limited by decisions already taken. Battery supply is being secured through a dedicated AESC gigafactory within the Douai plant, and Chinese suppliers account for around 5% of the group's global purchasing footprint. Provost called the proposal "a good sign that Europe is starting to move," while acknowledging its complexity. He framed his position in terms of reciprocity. "If you say to China and our Chinese competitors that Europe should not be closed — and this is a Renault recommendation — but the rules applied in Europe are the same that China did so successfully 20 years ago: you are welcome, but you have to invest in Europe, produce in Europe, use the supplier ecosystem, create jobs, put R&D. It will work," he said. On whether the IAA's legislative timeline would give Chinese manufacturers time to entrench before the rules changed, Provost said the group was positioned for any outcome. "We have two legs: all the technology and the legitimacy for electric cars, and a top technology for full hybrid. Those are the two legs. We are ready for any possible scenario."

Development Speed Drives the Cost Case

The competitive logic begins with development speed. Chief Technology Officer Philippe Brunet credited ACDC with demonstrating the viability of a two-year development cycle. The group's new One Engineering organisation, launched by Provost shortly after his appointment last July, scales that approach across three principles: faster development, using a full virtual digital twin with AI support across design and software coding; fewer parts per vehicle, with a 30% reduction through platform standardisation; and a leaner organisation with lower cost per engineering hour and a simplified R&D footprint. The combined effect is projected to reduce entry ticket costs by up to 40% compared with the previous generation and cut the cost of goods per vehicle by between 10% and 30%.

Philippe Brunet, Chief Technology Officer

ACDC remains a permanent fixture in the competitive architecture. Brunet outlined three roles for the centre: developing vehicles on the Geely-shared ANGE platform for overseas markets, sourcing components from the Chinese ecosystem towards the group's target of €400 in cost reduction per vehicle per year, and running what he called "a kind of market intelligence — a north star for us" on technology trends and best practices. Chinese suppliers account for around 5% of Renault's global purchasing footprint, a share the group expects to hold steady.

Provost was unambiguous on the boundaries of the relationship when Chinese media raised the question directly. "We do not plan to come back to the Chinese market as an OEM, just to be super clear," he said. China is a source of speed, cost benchmarking and engineering intelligence. It is not a market Renault intends to contest commercially.

The Technology Bets Behind the Numbers

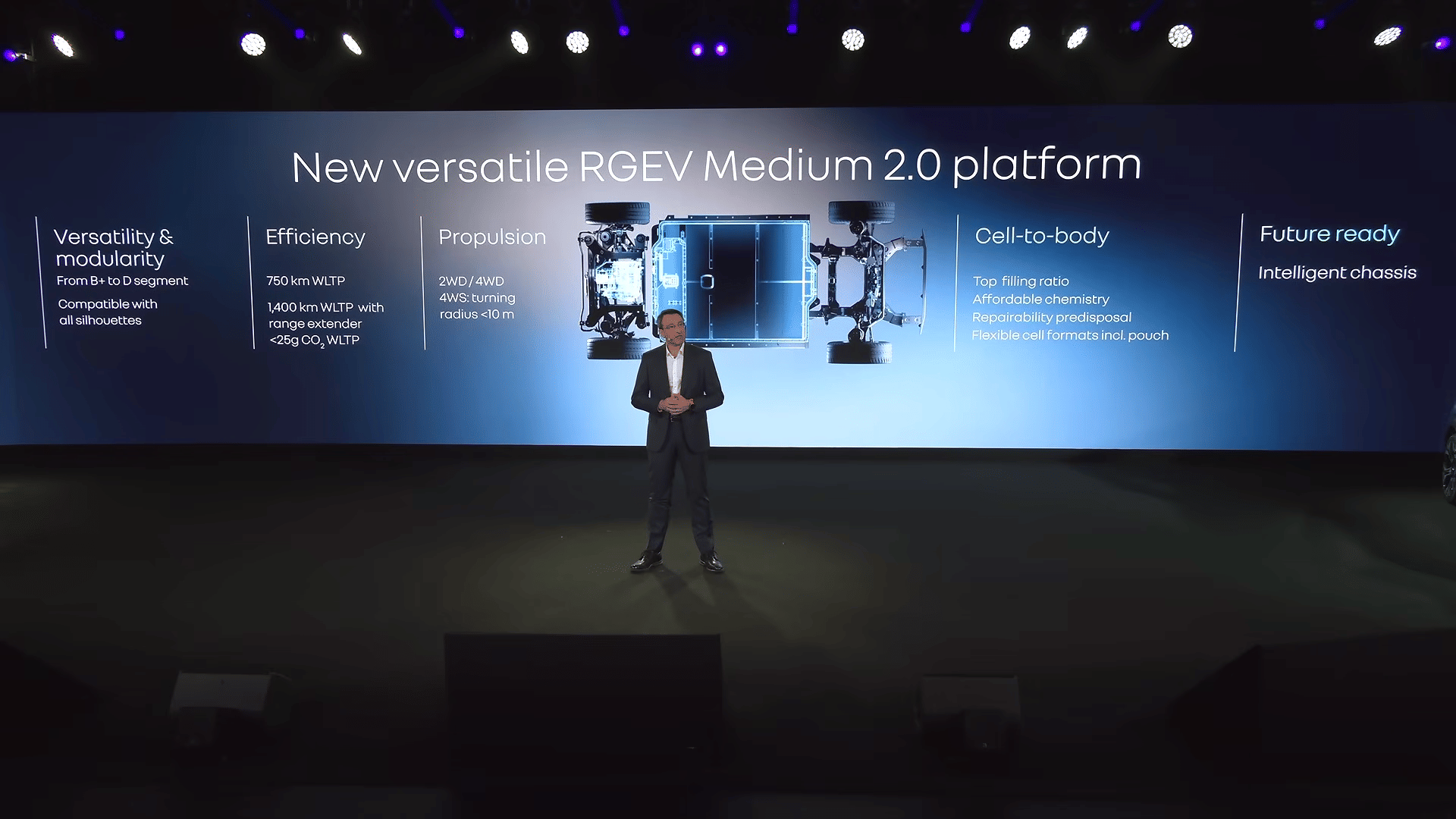

The technology centrepiece of futuREady is the RGEV Medium 2.0 electric platform, operational from 2028, covering the B-plus to D segments across saloon, SUV and MPV body styles. The group projects a 40% cost reduction against the current EV generation, a WLTP range of up to 750 km in standard form and up to 1,400 km with a range extender, and the platform will be developed primarily in France, with localisation planned in Palencia, Spain. It uses a cell-to-body battery design with a 70% fill rate (the proportion of pack volume occupied by active cells) and 20% fewer parts. French aggregate production output is expected to be 20% higher over the 2026 to 2030 period than over the preceding five years.

Thierry Charvet, Chief Industry, Quality and Supply Chain Officer

Alongside the platform, Renault is developing a third-generation electrically excited synchronous motor requiring no rare earths, costing 20% less and delivering 25% more output power than its predecessor. On software, the group has committed to launching the first Software Defined Vehicle by a European manufacturer in Europe in 2026, co-developed with Google, under which 90% of vehicle functions will be updatable over the air. Brunet framed the engineering ambition in direct competitive terms: "to bring together the skills to develop the technologies and the competitiveness that will allow us to compete with the best OEMs, such as the Chinese."

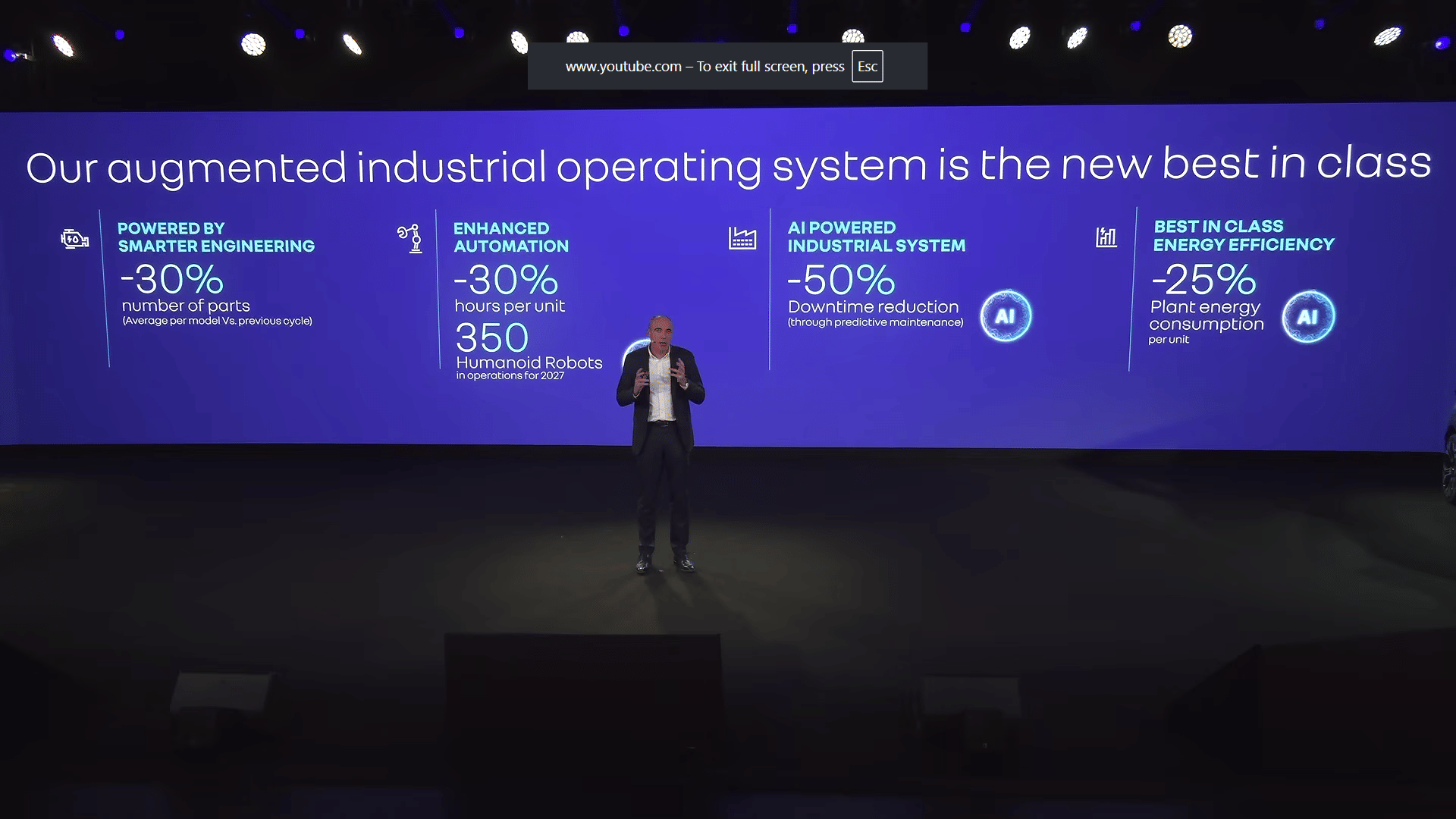

On the factory floor, Renault plans to deploy 350 humanoid robots across its plants within 18 months through a partnership with WonderCraft, a start-up. AI-based predictive maintenance is targeted to halve factory downtime. Plant energy consumption is planned to fall by 25%, bringing the cumulative reduction since 2020 to close to 50%. The projected outcome is a 20% reduction in production costs per unit and a 30% reduction in logistics costs.

Where Renault Claims Its Durable Edge

Technology parity with Chinese manufacturers is a process Renault acknowledges will take time. The group's argument for sustaining margin during that transition rests substantially on the downstream value chain, an area its newer Chinese competitors have not yet had time to build in Europe.

That argument is underpinned by a quality commitment the group frames as foundational. Over the past three years, Renault cut the number of customer claims by half while launching 24 models with significant technological changes. The plan now targets a further 50% reduction in incidents over the next three years, with an overall goal of reducing incident rates by 70% within the first five years of vehicle use. AI-powered inspection systems will provide 100% coverage of quality-critical assembly operations on each production line, and over-the-air technology will enable remote diagnosis and software remediation without dealership intervention. "Our ambition is clear," said Thierry Charvet, the group's Chief Industry, Quality and Supply Chain Officer, Renault Group. "After five years, our customers can confidently say, my car is brand new."

Renault targets an 80% customer loyalty rate over a ten-year vehicle lifecycle by 2030. The commercial logic, as the group presents it, is to layer revenue on top of the initial sale. Renault calls this the second and third life of a vehicle, encompassing used car resale, leasing roll-overs, aftersales, remote software updates and energy services. "We underestimated a massive revenue pool on second and third life that we will now tap into," said Fabrice Cambolive, the group's Chief Growth Officer. The group projects a 50% increase in dealer revenue beyond the first ownership cycle. A software-defined retail programme, built on the digitalisation of commercial processes and a vehicle digital twin, is targeted to reduce total distribution costs by 20%. The dealer network's breakeven point is expected to fall by a minimum of 20%.

Chief Financial Officer Duncan Minto confirmed that EV cost reductions will be passed on to consumers as the market requires and that the plan's free cash flow is not generated from working capital. Medium-term financial targets include a group operating margin of between 5% and 7% of revenue. Automotive free cash flow is targeted at a minimum of €1.5 billion per year on average. R&D, capital expenditure and supplier entry tickets will collectively remain below 8% of group revenue. A negative price-mix assumption of a few hundred million euros per year has been built into the plan to account for continued European pricing pressure from Chinese competitors. Provost summarised the two-layer competitive argument plainly: "Upstream, yes, true, we somehow catch up, but we are in the base and we will be at the level of the best in terms of innovation, cost and speed. Downstream, I deeply think that we can bring higher value."

India and the Retreat From Volume Growth

Renault's geographic ambition, targeting 50% of sales outside Europe by 2030 against 38% today, is anchored most concretely in India, where the group now has full ownership of its Chennai manufacturing plant. Stéphane Deblaise, a dedicated CEO, was appointed to oversee the entire Indian value chain. More than 90% of vehicles sold in India will be locally produced. The first model developed under the plan, the Bridger SUV, will be manufactured in India before being supplied to global markets. "India is competitive," Provost said. "We have the chance to be full-fledged now there."

The international ambition is explicitly framed against Renault's 2019 strategic plan, which set aggressive volume targets and did not meet them. "We do not push volume. We work on value," Provost said. "Today, we do not decide the volume. We decide the car, the way to serve the customer." The four differences he identified from 2019 are a value-oriented strategy, clearer brand management, a quality improvement now visible to customers, and a selective geographic focus on markets with strong growth trajectories and viable paths to profitability.

futuREady calls for 36 models by 2030. Whether it delivers on its financial targets will depend on how quickly the two-year development standard that produced the Twingo becomes the rhythm of an entire company.

RELATED ARTICLES

Royal Enfield Mulls Setting Up CKD Assembly Plant in Indonesia

Kiran Murali

Kiran Murali

29 Jul 2026

29 Jul 2026

The company currently follows a distributor-led model in Indonesia.

Force Motors Reports Q1 FY27 Net Profit of Rs 217 Crore

Autocar Professional Bureau

29 Jul 2026

Autocar Professional Bureau

29 Jul 2026

Commercial vehicle manufacturer posts 6% revenue growth alongside share acquisition of Veera Tanneries.

Royal Enfield Targets 2.45 Million-Unit Capacity by FY30

Kiran Murali

29 Jul 2026

The combined brownfield and greenfield expansions will increase annual manufacturing capacity by over 60% from current l...