Follow us

Follow us

India Used-Car Market To Hit $70 Bn By FY31: Redseer Report

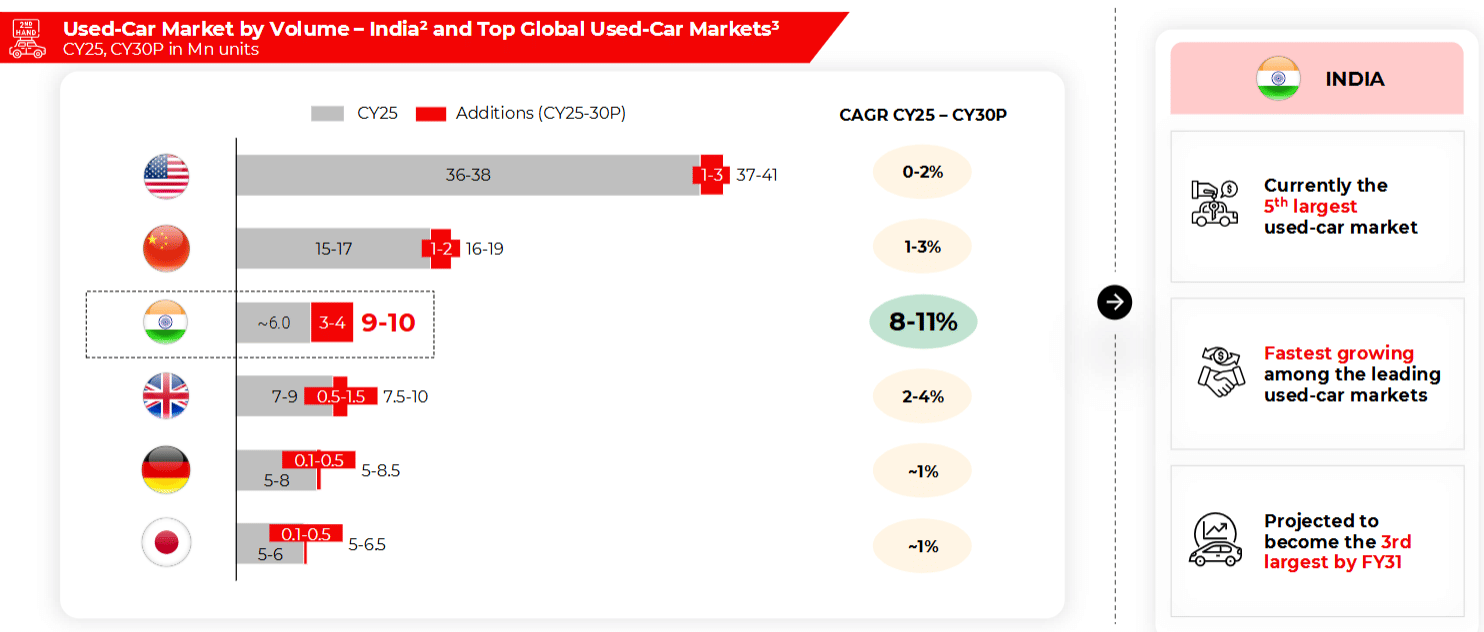

The report says India’s used-car market could reach 9-10 million units by FY31, expanding at 8-11% CAGR by volume, and making India third largest globally.

15 May 2026

15 May 2026

722 Views

Share -

722 Views

Share -

India’s used-car market is projected to nearly double to $68-78 billion by FY31, from around $35 billion in FY26, riding on rising household incomes, shorter vehicle replacement cycles, better financing access and growing digital adoption, according to a report by Redseer Strategy Consultants.

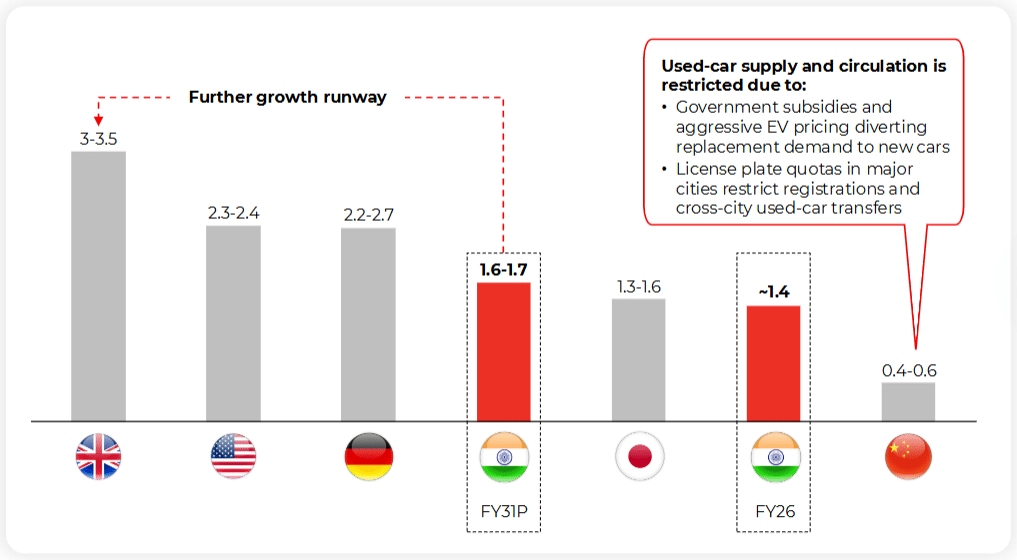

The market is expected to expand to 9-10 million units by FY31, from around 6 million units in FY26, growing at 14-18% CAGR by value and 8-11% CAGR by volume. This would make India the third-largest used-car market globally by the end of the decade, after the US and China, the report said.

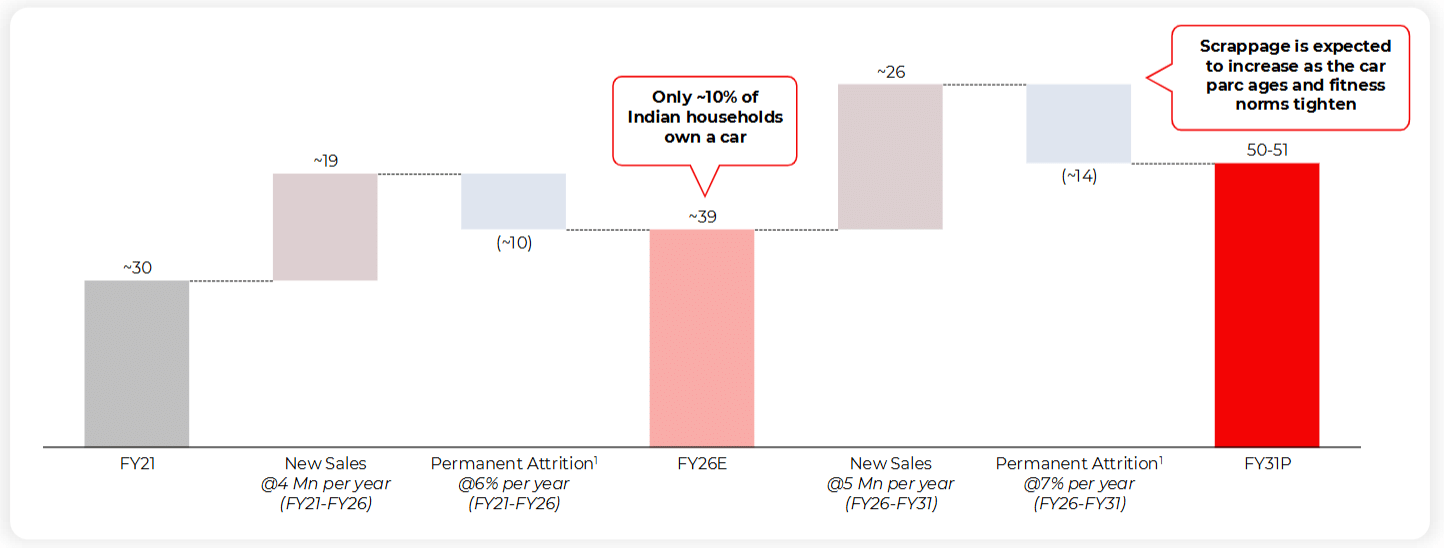

The scale-up will be driven by a larger car parc, faster upgrades, premiumisation, improved affordability, formal financing, regulatory digitisation and the resilience of used-car demand during economic cycles. Redseer expects India’s car parc to cross 50 million units by FY31, helped by steady growth in new car sales and low current levels of motorisation.

Yet, the opportunity is not only about more cars entering the system. The bigger shift is behavioural. Used cars are no longer being bought only because new cars are unaffordable. Increasingly, they are becoming a financially prudent route to access better variants, higher segments and lower total cost of ownership.

Used Cars are No Longer a Compromise Buy

The Redseer report marks a clear change in how Indian buyers look at used cars.

It says used-car purchase in India is “no longer a compromise, but a prudent choice”. Buyers are using the used-car route to access higher segments, top variants, better features or a smoother ownership experience without committing the capital required for a new vehicle.

Redseer identified four broad buyer types: aspirational buyers, convenience seekers, assurance seekers and bare-minimum buyers. Aspirational buyers want access to higher segments or better variants. Convenience seekers are willing to pay for a smoother end-to-end process. Assurance seekers focus on vehicle history, condition and trust. Bare-minimum buyers remain led by the lowest cost of ownership.

The stakes are high because nearly 65% of used-car buyers are first-time car owners. For them, the decision is not casual. It is often a family milestone involving savings, EMIs, comparisons, vehicle checks and long-term ownership cost calculations.

This explains why trust, certification, warranty, financing and documentation are no longer optional. For many buyers, a used-car transaction now carries the emotional and financial weight of a new-car purchase.

Top Cities will Remain Important

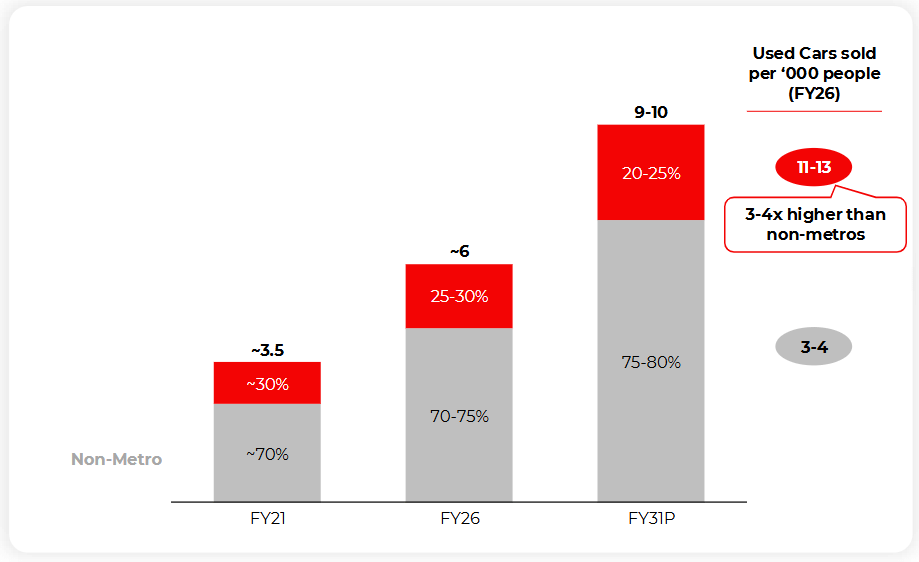

Even as non-metro India grows, used-car demand will remain concentrated in large cities.

Redseer expects the top eight cities to contribute around 20-25% of used-car volumes even by FY31. Delhi alone accounts for 25-35% of used-car demand within the top eight metros. Mumbai, Bengaluru and Hyderabad together account for another 30-40%, while Pune, Chennai, Ahmedabad and Kolkata make up the rest.

The report said used cars sold per 1,000 people in the top cities are 3-4 times higher than in non-metro markets. This concentration makes the top metros important for organised players because these cities offer higher transaction density, better financing access, stronger digital adoption and more frequent replacement cycles.

At the same time, non-metro growth will matter for scale. As incomes rise and financing improves, Tier 1 and Tier 2 markets are expected to generate more demand. The winners will likely be platforms that can combine metro-depth with controlled expansion into smaller markets.

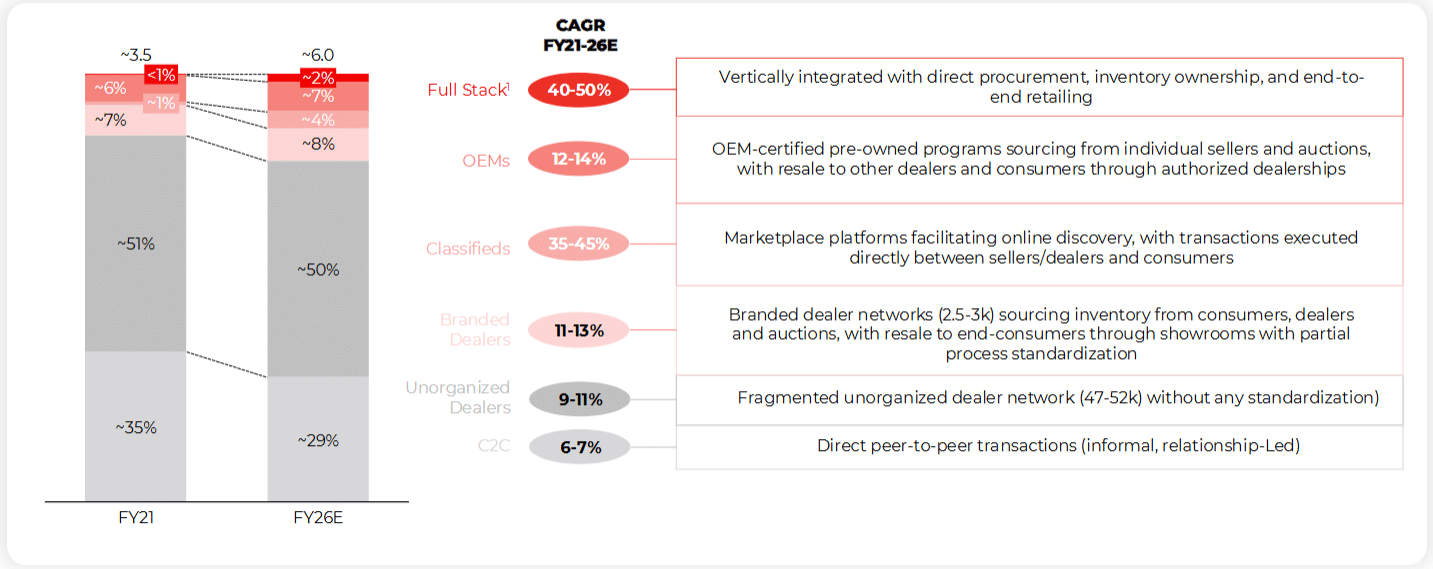

Full-Stack Platforms Could Unlock Next Growth Wave

The next phase of growth in India’s used-car market will depend on how quickly organised players can solve the sector’s biggest problem: trust.

According to Redseer, nearly 80% of used-car transactions remain unorganised. The segment continues to dominate because of reach, familiarity and local relationships, but it often falls short on standardised inspection, warranty support, price transparency, documentation and post-sale assurance.

The unorganised dealer network itself is estimated at 47,000-52,000 dealers, while branded dealer networks are much smaller at around 2,500-3,000 outlets. This makes the used-car market not just a retail business, but also a sourcing, pricing, inspection, refurbishment, financing and documentation business.

Classified platforms improve discovery, but do not control the full transaction. OEM-certified used-car programmes improve trust, but their reach is limited. Branded dealers bring more standardisation, but still operate with partial process control.

This is where full-stack used-car operators could gain ground. These platforms control the transaction end-to-end, from sourcing, inspection and refurbishment to inventory ownership, pricing, sales, financing, documentation and post-sale support.

According to Redseer, full-stack players are expected to increase their market penetration from about 2% currently to 5-6% by FY31, unlocking a roughly $4-billion opportunity and growing at 36-44% CAGR. In the top eight cities, their share could rise to around 15% of used-car sales by FY31.

The model is structurally stronger because it owns more parts of the customer journey. Redseer said full-stack platforms bridge the buyer trust gap with around 80% NPS, compared with less than 30% for unorganised channels. These players also offer trained sales teams, home test drives, branded hubs, digital documents, financing support and standardised processes.

But the model is difficult to build. It requires working capital, inventory ownership, refurbishment centres, logistics, technology, trained sales teams, financing partnerships and customer support. These factors increase complexity and capital needs, but also create entry barriers once scale is reached.

For organised players, the opportunity is clear. The challenge is execution. They have to solve trust, control quality, manage inventory risk and still keep the business profitable in a market where unorganised dealers continue to dominate volumes.

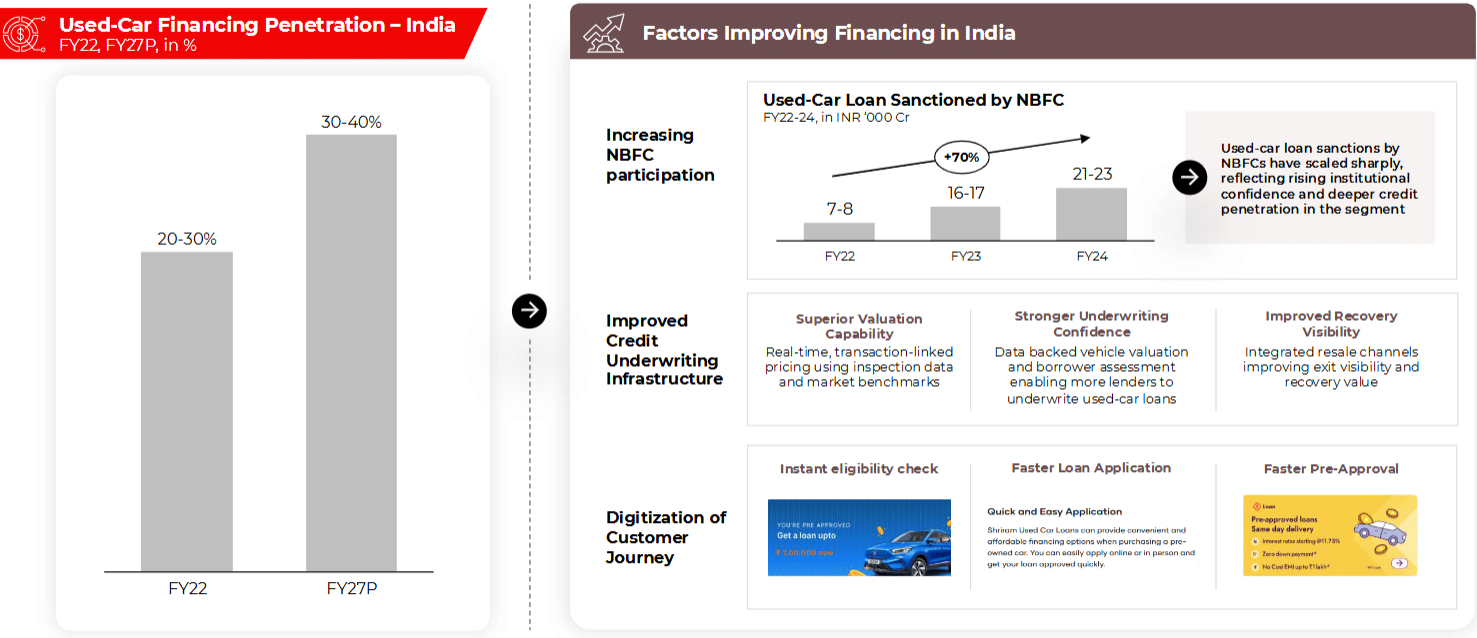

Financing Could Become The Next Big Lever

Financing is another critical growth driver. Used-car financing penetration in India is expected to rise from 20-30% in FY22 to 30-40% by FY27, according to Redseer. This is being supported by higher NBFC participation, better vehicle valuation tools, stronger underwriting models, digital KYC, faster loan approvals and embedded financing journeys.

The report said NBFC loan sanctions for used cars have scaled sharply, reflecting rising institutional confidence in the segment. Better financing reduces upfront payment pressure for buyers and expands the addressable market.

This is important because Redseer expects the addressable used-car buyer base to expand to around 280 million households by FY31. Rising incomes will also support demand, with more households moving into income brackets where used cars become more affordable relative to annual household income.

For organised players, financing is not only a conversion tool. It is also a trust lever. A buyer who gets vehicle valuation, inspection, loan approval and documentation in one journey is less likely to depend on informal dealers or fragmented networks.

Used Cars May Be More Resilient Than New Cars

The report also argues that the used-car market is less volatile than the new-car market during economic shocks.

During Covid and the semiconductor shortage, new-car sales saw sharper disruption because they were directly linked to OEM production, component availability and global supply chains. Used-car demand, by contrast, remained relatively more resilient.

This resilience comes from the nature of the market. Used cars offer lower acquisition cost, lower depreciation impact and wider price points. In a downturn, some buyers may delay new-car purchases but still consider used cars. Others may trade down from a new car to a better-value used car.

The EV transition is also unlikely to disrupt the core used-car market quickly. Redseer expects more than 90% of India’s car parc to remain non-EV even in 10 years. Used EVs are also expected to remain more expensive than average used cars, limiting direct substitution in the near term.

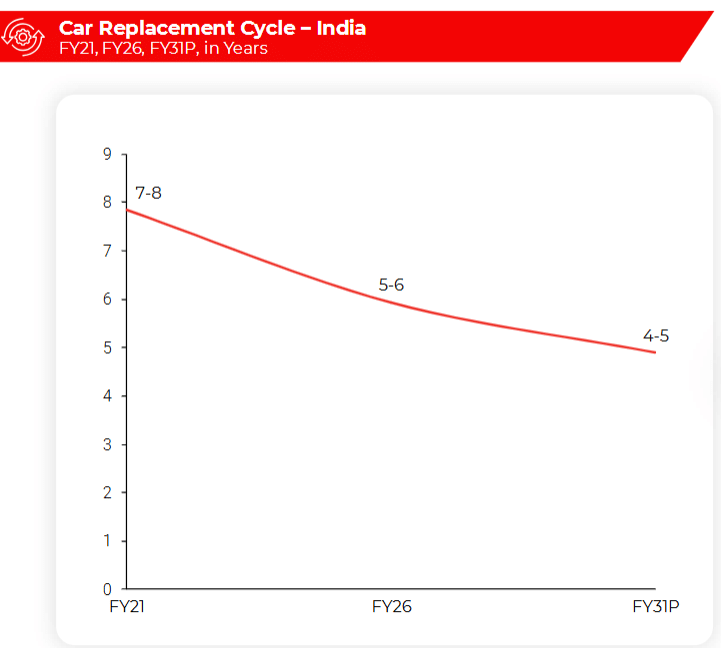

Faster Replacement Cycles to Improve Supply

On the supply side, shorter ownership cycles are expected to bring younger and better-quality used cars into the market.

Redseer expects India’s average car holding period to reduce from 7-8 years in FY21 to 5-6 years in FY26 and further to 4-5 years by FY31. In metros, the replacement cycle could shrink to 3-4 years by FY31.

This shift is being driven by faster model refreshes, new brands, more feature-rich cars, safety technologies, ADAS, infotainment upgrades, hybrid and electric variants, better fuel efficiency and tighter regulatory norms.

As consumers upgrade earlier, the used-car market gets access to younger inventory. This improves buyer confidence and allows organised platforms to build stronger propositions around inspected, certified and refurbished vehicles.

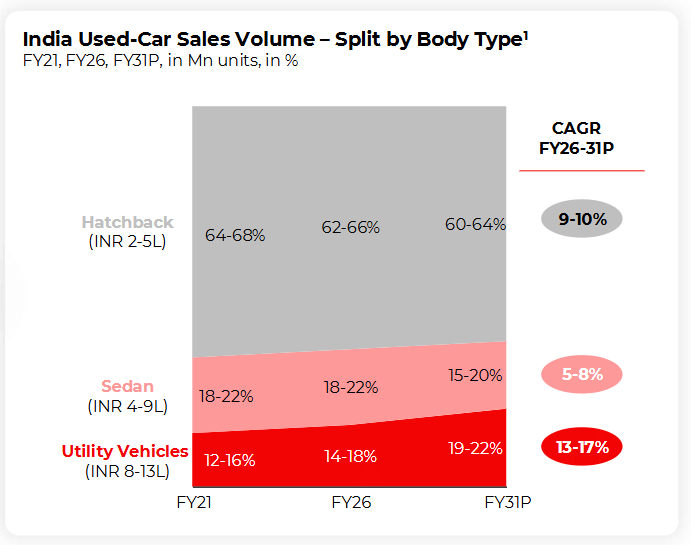

Used SUVs to Drive Premiumisation

The SUV boom in the new-car market is also spilling over into the used-car market.

Redseer expects the average selling price of used cars to rise from around ₹5 lakh in FY26 to ₹6.5-6.9 lakh by FY31, reflecting premiumisation and a richer inventory mix. The share of utility vehicles in used-car sales is projected to increase, while hatchbacks are expected to lose share.

This means the used-car market is not just becoming larger, but also more valuable. Buyers are increasingly looking for compact SUVs, mid-size SUVs and higher variants, mirroring the shift in new-car demand.

The premiumisation trend also benefits organised and full-stack players. Higher-ticket vehicles create room for inspection, warranty, refurbishment, financing and value-added services, which are harder to monetise in low-ticket transactions.

Trust Will Decide the Winner

India’s used-car market is entering a phase where growth is no longer the central question. The bigger issue is who captures that growth.

The market has strong tailwinds: more cars on the road, faster replacement cycles, younger inventory, SUV-led premiumisation, better financing, digital discovery and regulatory digitisation. But it also has a deep trust deficit.

For the market to reach its projected $70-billion size, buyers need confidence on vehicle quality, price fairness, ownership history, financing, warranty, documentation and post-sale support.

That is why full-stack platforms could become more important. They may not replace unorganised dealers overnight, but they can set new benchmarks for trust, transparency and process quality.

If organised players can solve for trust while managing capital intensity, India’s used-car market could move from being a fragmented resale bazaar to one of the country’s most important auto retail growth engines.

Watch Autocar Professional's interview with Kushal Bhatnagar, Associate Partner at Redseer Strategy Consultants, unpacking the findings of Redseer’s latest report on India’s used-car market:

RELATED ARTICLES

Attorney General's Office Says Its Submission Never Called the E20 Programme an 'Experiment'

Mukul Yudhveer Singh

30 Jun 2026

Mukul Yudhveer Singh

30 Jun 2026

AG’s Office says media reports claiming the Government described the E20 programme as an “experiment” before the Supreme...

Sierra.ev, Harrier.ev Put Tata Motors’ Premium EV Strategy to the Test

Darshan Nakhwa

30 Jun 2026

Darshan Nakhwa

30 Jun 2026

Overlapping prices and shared hardware raise cannibalisation risk, but the carmaker expects differences in size, styling...

Samvardhana Motherson Realigns Target Deadlines for Three Global Acquisitions

Dev Vadchhedia

30 Jun 2026

Dev Vadchhedia

30 Jun 2026

The automotive parts supplier updates compliance schedules for its pending buyouts in Yutaka Giken Co., Nexans autoelect...