Follow us

Follow us

EV sales in India surpass 2.45 million units in FY2026, all 4 segments register double-digit growth

With the electric 2W and 3W as well as the passenger and commercial vehicle segments each hitting their highest-ever retail sales, FY2026 saw India EV Inc continue the rich vein of growth it has displayed since FY2023. Here’s taking a close look at each of the 4 EV segments’ performance.

3369 Views

3369 Views

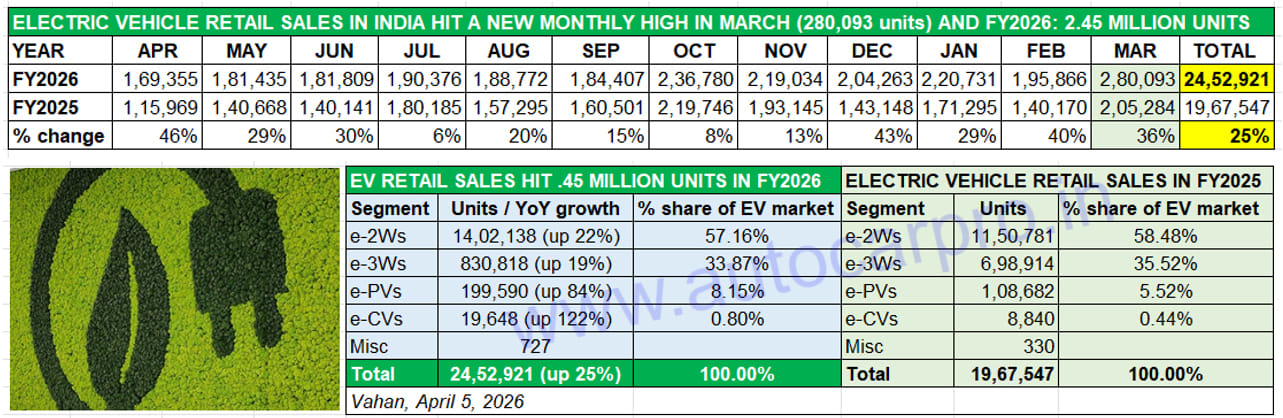

Even as the world battles a crude oil crisis, the Indian EV industry has wrapped up FY2026 on a very strong note. Combined sales of zero-emission 2- and 3-wheelers, passenger and commercial vehicles at 2.45 million (24,52,921 units) made for robust 25% YoY growth (FY2025: 19,67,547 units). That’s an additional 485,374 EVs sold YoY with growth democratised across all four vehicle sub-segments.

As the 12-month Vahan-derived retail sales split reveals, India EV Inc crossed the 200,000 monthly sales mark for the first time in festive October 2025 (236,780 units) and then achieved the same in November, December, January and March. In fact, the FY2026-ending month of March 2026 turned out to be record-breaking one with 280,093 units.

This is a creditable achievement, given that the GST 2.0 tax reform from end-September 2025 reduced ICE vehicle prices substantially and thereby increased the ICE-to-EV price differential.

Monthly retails surpassed 200,000 five times in FY2026 and hit a new high (280,093 units) in March 2026. All four vehicle sub-segments clocked highest-ever fiscal sales with e-PVs being an outlier.

In FY2026, the EV industry’s penetration level in overall automobile sales in India rose to 8.27% (of the 29.63 million vehicles) from 7.52% in FY2025 (of the 26.14 million vehicles). Each of the four vehicle sub-segments – two- and three-wheelers, passenger and commercial vehicles – achieved their best-ever annual sales. While electric 2Ws (1.40 million units, up 22%) had a 57% share of the India EV market, e-3Ws (830,818 units) had a 34% share. Surging demand for zero-emission passenger vehicles saw retail sales rise handsomely by 84% YoY to a record 199,590 units, giving the e-PV category an 8% share, up from the 5.5% it had a year ago. And, e-CVs (19,648 units, up 122%) increased their EV industry share to 0.80% from 0.44% a year ago. Let’s take a closer look at each of the four EV vehicle categories and their top performers.

e-2W SALES

FY2026: 14,02,138 units, up 22%. EV market share: 57%

FY2025: 11,50,781 units. EV market share: 58%

If India EV Inc scaled a new high of 2.45 million units in FY2026, much of the credit goes to the stellar performance of the most affordable sub-segment – electric two-wheelers. The 1.40 million e-2Ws delivered to customers made for strong 22% YoY growth on a large base (FY2025: 11,50,781 e-2Ws) and a 57% share of India EV Inc’s record EV sales. Importantly, this strong growth has come on a high year-ago base and in the face of the considerably reduced price-differential between IC engine two-wheelers and EVs as a result of the sharp reduction in GST from September 2025. In FY2026, the e-2W penetration level rose to 6.54% in the total 21.41 million 2Ws (ICE and EV) sold in India versus 6.09% in FY2025 (18.89 million ICE and EV 2Ws).

The e-2W industry achieved six-figure sales in 10 of the past 12 months versus just four in FY2025 and scaled a new monthly sales high in the fiscal year-ending March 2026 with 190,941 units and handsome 45% growth. India e-2W Inc’s performance in FY2026 would have been even better if it wasn’t dragged down by the lacklustre performance of FY2925’s market leader – Ola Electric (164,294 units) – whose sales fell sharply by 52% YoY to less than 200,000 units and its position dropped by three ranks to No. 4, below market leader TVS Motor Co, Bajaj Auto and Ather Energy, and ahead of Hero MotoCorp.

For a comprehensive analysis of the e-2W segment’s performance in FY2026 and sales statistics of the Top 35 e-2W OEMs, CLICK HERE

e-3W SALES

FY2026: 830,818 units, up 19%. EV market share: 34%

FY2025: 698,914 units. EV market share: 35%

India’s e-3W industry, which had missed the 700,000 milestone by a whisker in FY2025, easily surpassed that and went on to register record retail sales of 830,818 units in FY2026, up 19% YoY. As is known, the e-3W segment continues to witness the fastest transition to electric mobility, mainly driven by legacy ICE OEMs which have diversified into zero-emission vehicles. In FY2026, the share of e-3Ws in overall 3W sales rose to 61% compared to 57% in FY2025. And the record 830,819 units gave the segment a 34% share of India EV Inc’s record 2.45 million units, the second highest after the e-2W segment’s 57% share.

Retail sales in FY2026 saw a sharp spike in November (83,663 units, up 32%) and December 2025 (88,276 units, up 49%) with the year-ending month turning out to be the highest monthly sales yet for the e-3W industry. India e-3W Inc’s robust performance was driven by three legacy OEMs – Mahindra & Mahindra, Bajaj Auto and TVS Motor Co – along with a few other companies from amongst the 680-player market. For a closer look at the top six best-selling e-3W OEMs who accounted for 36% (300,647 units) of the record retail sales in FY2026, CLICK HERE.

e-3W SALES

FY2026: 830,818 units, up 19%. EV market share: 34%

FY2025: 698,914 units. EV market share: 35%

India’s e-3W industry, which had missed the 700,000 milestone by a whisker in FY2025, easily surpassed that and went on to register record retail sales of 830,818 units in FY2026, up 19% YoY. As is known, the e-3W segment continues to witness the fastest transition to electric mobility, mainly driven by legacy ICE OEMs which have diversified into zero-emission vehicles. In FY2026, the share of e-3Ws in overall 3W sales rose to 61% compared to 57% in FY2025. And the record 830,819 units gave the segment a 34% share of India EV Inc’s record 2.45 million units, the second highest after the e-2W segment’s 57% share.

Retail sales in FY2026 saw a sharp spike in November (83,663 units, up 32%) and December 2025 (88,276 units, up 49%) with the year-ending month turning out to be the highest monthly sales yet for the e-3W industry. India e-3W Inc’s robust performance was driven by three legacy OEMs – Mahindra & Mahindra, Bajaj Auto and TVS Motor Co – along with a few other companies from amongst the 680-player market. For a closer look at the top six best-selling e-3W OEMs who accounted for 36% (300,647 units) of the record retail sales in FY2026, CLICK HERE.

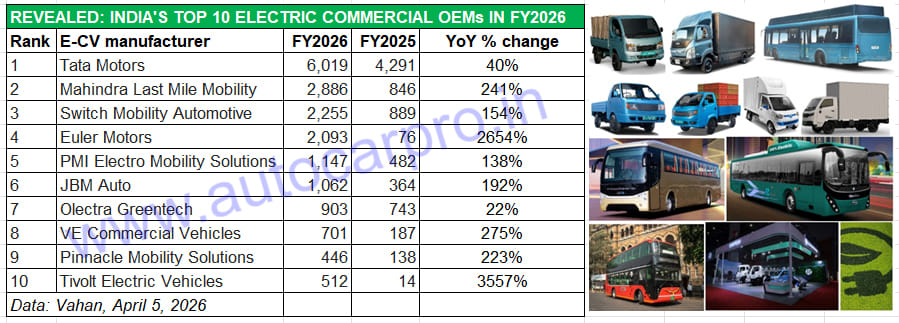

The Top 6 e-CV OEMs with 15,462 units accounted for 78% of the segment’s record sales in FY2026.

The Top 6 e-CV OEMs with 15,462 units accounted for 78% of the segment’s record sales in FY2026.

e-COMMERCIAL VEHICLE SALES

FY2026: 19,648 units, up 122%. EV market share: 0.80%

FY2025: 8,840 units. EV market share: 0.44%

Lowest in terms of volumes but the highest in sticker price, the electric commercial vehicle segment also hit a new annual sales high last fiscal. The 19,648 e-CVs sold in FY2026 are up 122% YoY (FY2025: 8,840 units), which sees the e-CV segment double its share of the all-India EV market to 0.80% from 0.44% in FY2025. All three vehicle categories (buses, light goods carriers and heavy goods carriers) have registered YoY growth.

Zero-emission light goods carriers (13,767 units, up 167% YoY) accounted for the bulk of sales – 70 percent – up from the 58% share they had in FY2025. This is an increase of 8,613 units YoY and reflects the surge in demand coming from last-mile mobility providers, particularly from urban India.

Demand for electric buses, which are mainly bought by state transport undertakings for inter-city operations and local municipal corporations for city transport, saw sales grow 45% YoY to 5,039 units albeit their share of the e-CV market fell to 26% from 39% a year ago. And heavy goods carriers, typically used for infrastructure operations across the country, jumped 318% YoY to 840 units which gives them a 4% share of e-CV retail sales.

Of the total 19,648 e-CVs sold in India, market leader Tata Motors accounted for 6,018 units (up 20% 40% YoY) or a 31% share, much reduced from the 49% it commanded in FY2025. Mahindra Last Mile Mobility, with strong sales of 2,886 units (up 241% YoY) had a 15% share versus 10% a year ago. Switch Mobility, Ashok Leyland’s EV arm, sold 2,255 buses and light CVs to register 154% YoY growth and an 11% share of the e-CV industry’s sales last year. Meanwhile, fourth-ranked Euler Motors has a robust run of the market – the 2,093 units give it an 11 % market share in its first full fiscal year of retails. PMI Electro Mobility Solutions (1,147 units), JBM Auto (1,062 units), Olectra Greentech (903 units), VECV (701 units), Pinnacle Mobility (446 units)) and Murugappa Group company Tivoli Electric Vehicles (512 units) also registered strong YoY growth.

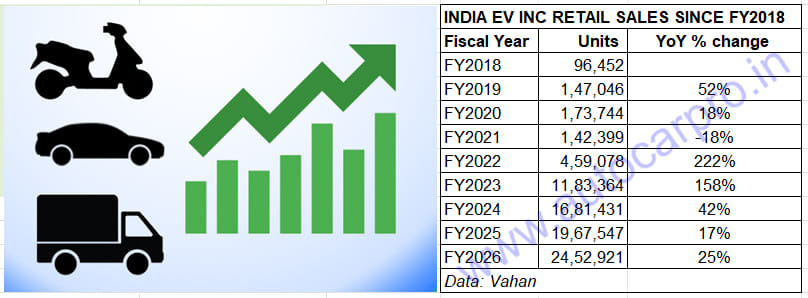

INDIA'S EV GROWTH STORY: 8.30 MILLION EVs SOLD SINCE FY2018

A deep dive into retail sales numbers since FY2018 reveals just how rapidly demand has grown for EVs in India, particularly in the past four years. Between FY2018 to FY2026, 8.30 million zero-emission vehicles have been bought in the country. Of this, 7.28 million EVs or 88 percent have been delivered to customers only in the past four discal years, reflecting the accelerated growth in the domestic EV industry.

The government has outlined a strategic shift to e-mobility, and has targeted EVs to account for 30% of its mobility requirements by 2030. Growing consumer awareness about the need to use eco-friendly transport and the wallet-friendly nature of EV cost of ownership over the long run is proving to be a big catalyst to adoption of electric mobility. What’s more, there’s fast-paced demand coming in from the e-commerce industry and logistics players for EVs on two and three wheels, and from taxi fleet operators for electric passenger vehicles.

Meanwhile, recognising the huge business potential, auto component manufacturers are also upping the ante on localising EV parts, either through full ground-up development or through technology licences. This is leading to enhanced optimisation of production costs and in turn EV affordability, which is the overriding growth mantra. The recent global crude oil crisis, as a result of the impasse at the critical Strait of Hormuz, has only served to accelerate the EV mantra as a measure to reduce expensive fossil fuel imports as well as more environment-friendly motoring.

RELATED ARTICLES

Bajaj Auto Races Past 800,000 EV Sales; Chetak on Track for 400,000 Units This Year

Ajit Dalvi

Ajit Dalvi

28 Jun 2026

28 Jun 2026

Bajaj Auto marks new retail milestone for its Chetak e-scooter, which has witnessed remarkable acceleration in recent mo...

IPO-bound Greaves E-Mobility Crosses 300,000 Sales, Registers 58% Growth This Year

Ajit Dalvi

18 Jun 2026

GEM’s new retail sales milestone for its Ampere e-scooters comes on the back of demand for the Nexus, Magnus Neo and G-M...

Hyundai Venue Joins Select Band of Compact SUVs With 800,000 Sales

Ajit Dalvi

09 Jun 2026

Hyundai Motor India’s first-ever compact SUV launched in May 2019 and followed by the second-gen model in November 2025 ...